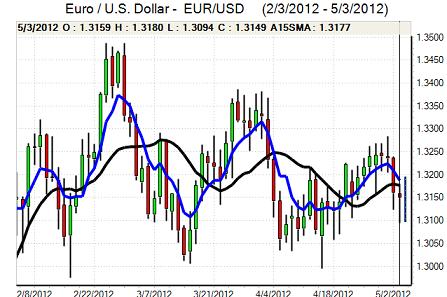

EUR/USD

The Euro hit resistance close to 1.3160 ahead of the ECB meeting on Thursday and tended to drift lower as caution prevailed. As expected, the ECB left interest rates on hold and the press conference was the main focus. Although President Draghi continued to reference downside growth risks he also stated that there were some signs of stabilisation during the first quarter. These remarks were somewhat surprising given the very weak surveys for April. Draghi also stated that there had been no discussion surrounding specific interest rate cuts with the overall monetary policy stance described as accommodative.

The net impact was to dampen expectations of a further near-term cut in interest rates which helped underpin the Euro, especially with a covering of short positions following the inability to bear 1.31 support. There will still be major concerns surrounding the economic outlook and the overall impression was that the ECB was looking to shift the focus back onto political action to boost the growth outlook and limit sovereign-debt risks rather than reflecting any real confidence in the outlook.

There were political uncertainties surrounding the French and Greece elections this weekend with fears that the pro-austerity Greek parties would not be able to secure a majority. There were also uncertainties over the French-German relationship if Hollande wins in France.

There was a decline in US jobless claims to 365,000 in the latest week from 392,000 the previous week which provided some relief to economic sentiment. In contrast, there was a decline in the latest ISM services-sector report to 53.5 from 56.0 previously. There was a decline in the export and employment components for the index, although they were still comfortably above the 50 level.

The data will maintain a high degree of uncertainty over the monthly payroll report and the US currency will tend to gain support on yield grounds if there is a stronger than expected report. The Euro consolidated around the 1.3150 region as narrow ranges prevailed.

Source: VantagePoint Intermarket Analysis Software

Call now and you will be provided with FREE recent forecasts

that are up to 86% accurate* 800-732-5407

If you would rather have the recent forecasts sent to you, please go here

Yen

The dollar found support in the 80.20 region against the yen on Thursday and pushed to challenge resistance near 80.50 following the better than expected jobless clams data. The US currency was unable to sustain momentum and there was renewed selling pressure following the ISM report as yields retreated again.

Japanese markets remained closed for the Golden Week holidays which continued to stifle activity. The dollar was unable to gain any fresh support in Asian trading on Friday with concerns surrounding the Asian economic outlook important in curbing selling pressure on the Japanese currency as risk conditions remained very cautious ahead of the US employment report.

Sterling

The latest UK PMI services-sector index was weaker than expected with a decline to 53.5 from 55.3 the previous month. Although this was significantly worse than expected and did push Sterling weaker, the impact was offset by a rise in the business expectations component to a 25-month high as hiring intentions also strengthened.

Although there was still a high degree of uncertainty, the net result from this week’s surveys was reduced, expectations surrounding further quantitative easing which helped underpin sentiment. In this context, selling pressure was limited with support on dips towards 1.6150 against the dollar with a move back towards the 1.62 region. Sterling also pushed to a fresh 22-month high close to 0.81 against the Euro before a partial retreat with evidence of further defensive inflows into the UK currency.

Swiss franc

The dollar pushed to highs near 0.9170 against the franc on Thursday immediately after the ECB interest rate decision, but was unable to sustain the gains and retreated back to below 0.9150 as momentum was again lacking.

The Euro was unable to make any significant headway against the Swiss currency even with the ECB taking a slightly less dovish stance than had been expected. There was still an important lack of confidence in the underlying Euro-zone fundamentals which maintained the potential for defensive capital inflows into the Swiss currency.

Source: VantagePoint Intermarket Analysis Software

Call now and you will be provided with FREE recent forecasts

that are up to 86% accurate* 800-732-5407

If you would rather have the recent forecasts sent to you, please go here

Australian dollar

The Australian dollar was unable to re-establish a position above 1.03 against the US currency on Thursday and retreated to lows below 1.0250 as it retested April lows. The currency remained generally on the defensive even though the US dollar failed to hold its best levels.

There were further doubts surrounding the Asian economy and downward pressure on commodity prices which stifled demand for the Australian dollar. The run of weak domestic data and more aggressive than expected Reserve Bank action, also continued to have a negative impact on the Australian currency and the currency was trapped close to 1.0250.