As one who has spent many years studying financial markets, I have focused on market breadth analysis. I have wondered why in this area little progress has been made in the past 60 or 70 years. We continue to use the classic data of advances, declines, unchanged, and the traditional Advance-Decline Line. We have not advanced much beyond the work of the Masters. We use multiple variations of the same indicator, but most all these indicators are based on price change from yesterday.

UNDERSTAND THE LIMITATIONS

Any intent to develop new oscillators or indicators using market breath data is limited, in the majority of cases, by the available historical data. It is necessary to know what can be the influence or impact of survivorship bias on the outcomes of those creative pursuits. It is clear that our current breadth indicators and data do not have information about those stocks that have ceased trading due to acquisition, merger, bankruptcy, or delisting. Hence, when we study the past without taking into account those missing stocks, our results are incomplete, and moreover, we cannot determine at what point in time our market breadth analysis began to lose robustness.

CRITICAL FACTOR

My review of trading system literature shows that failure to account for survivorship bias overestimates results over those obtained when stocks that have ceased trading have been taken into account. This is due to the observation that theoretically stocks that have ceased trading had a negative performance record, and hence, by eliminating them, the result is superior. I have some concerns about this observation, but without more space to explain, it is deemed valid.

KEY QUESTION

What is the effect on our market breadth indicators and their statistics without accounting for survivorship bias? In the past two years, while developing new oscillators and calculations, I have asked myself that question.

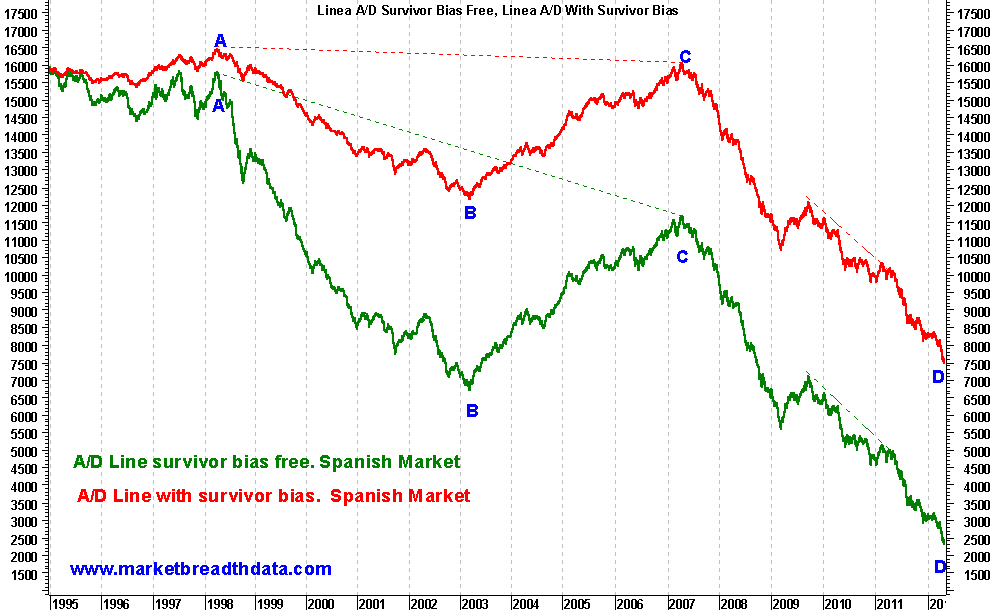

This past year, I worked with derivations of market breadth data from the Madrid Stock Exchange (SIBE). The Green line in Figure 1 shows an A/D Line without survivorship bias (I have calculated this A/D Line for many years), while the Red line shows the A/D Line calculated with all issues then trading without considering those that had ceased trading.

For a better comparison of their movements, I equalized the starting values of both A/D Lines at the start of 1995.

It is obvious that the behavior of both A/D Lines is quite different, although their directional movement is similar for most of the time shown in Figures 1 and 2.

It is evident that as we look back in time, the behavior of both A/D Lines becomes more different – a logical result because the number of issues used to calculate the A/D Lines began to change. As certain stocks ceased trading, the difference in the number of stocks used to calculate each A/D Line changed (less in the A/D Line that accounts for survivorship bias). This difference explains the amplitude in Figure 1 between Points A and B which is greater in the Green A/D Line than in the Red A/D Line.

A noteworthy detail is the difference in the trend lines between Points A and C in both A/D Lines. In Figure 1, on February 27, 2007, the slope of the Red trend line (-0.194) was 89% less than the Green trend line’s slope (-1.803). But on the trend lines drawn in Figure 2, the difference was considerably reduced. On October 22, 2010, the difference between the slope of the Red trend line (-5.14) and Green trend line (-5.57) was 43%.

USE CAUTION

We must note that the Madrid Stock Exchange (SIBE) is small. Currently, some 130 companies are listed. Even with this small number of listings, we can see the influence of survivorship bias on market breadth indicators. Thus, we must be cautious with any market breadth studies that do not take into account survivorship bias, especially in larger exchanges where a greater number of issues is traded.

MORE TO COME

In future articles, we will continue to describe the behavior of survivorship bias and its effect on technical indicators. We will show similar behavior seen in the USA market. These studies, including how to construct an A/D Line with reduced noise without a significant reduction in performance, will be presented in a forthcoming book this Spring.

Thanks to: George A. Schade, Jr., CMT who translated this article.