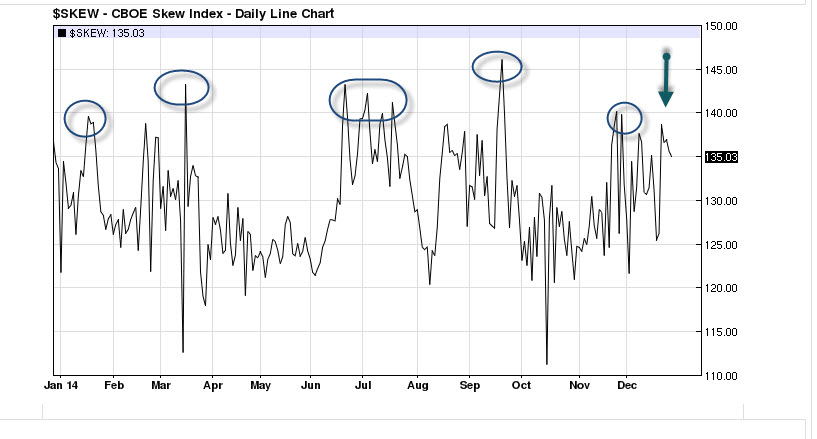

I wrote about the CBOE Skew Index here a couple of months ago and talked about how it had become a fantastic predictor of correction market moves in 2014. To review, the skew index is a compilation of bets placed on out of the money options, mostly puts. These bets are ‘looking’ for a big move south very quickly, perhaps the result of some sort of ‘black swan’ event. For the most part, these tail risk bets rarely pay 0ff – mostly 5% of the time or less.

But when they do, the gains are sharp and quick. Many option players buy these options as protection or a hedge against an overbought market condition. We are bumping up against an overbought condition that may produce another sharp correction – soon. See the skew index below.

What I have found interesting in 2014 is when the skew index spikes (more bets on these increase the price of the index) there has been a good-sized correction every time. The major high in skew was in mid September, and what unfolded afterwards was a 9.4% correction. All others this year were swift but mild, about 4-6% in size and no more than two weeks in duration. More recently the skew hit near 138 and a 5% correction ensued.

However, correction calls with a high skew generally are coupled with a low volatility index, or VIX. In just about every case in 2014 the VIX was 13% or lower when skew was high, in one case it was close to 10%. That is a reading of high complacency and buyers have likely finished. When the buying is done there is nothing left to do but sell. The smart money will reach for protection when it’s cheap (as it is when VIX is low) to guard against losses on their long stock/option plays.

It is hard to understand this counter play being successful. Buying a 5% probability expecting a payoff is a very poor bet, but the point is buying insurance BEFORE something disastrous occurs. Further, the ‘hope’ is that this protection does not pay off, but it’s good to have just in case. If you do not have fire insurance on your house and all the sudden your neighbor’s roof is in flames, you’re not on the phone with your insurance agent looking for coverage, right?

In addition, the MC oscillators have clocked in now over 100 on both the NYSE and Nasdaq, as breadth has been strong over the last several days (Dow Industrials up 7 days straight). That is not yet to an extreme overbought but it is headed there.

So, we are currently at 135 on the skew index, not the highest level of the year and a VIX at 14.5% – also not the lowest reading. But this is something we need to be aware of as the holiday trading continues we should see volatility drop even more, and as that happens we’ll see the smart money reaching for cheap protection. Not a bad idea for us to do, too. I’ll be watching both of these closely.