(Just Be Sure You Get a Credit)

Today I want to talk about the one by two ratio vertical spread, both long and short. Both are excellent trading strategies, although the one with the most risk works more often than the one with unlimited profit potential.

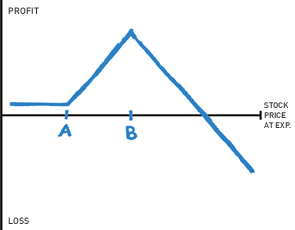

Let’s examine the long-ratio vertical where you own one option and are short two further out-of-the money (OTM) options. And you want to do this for a net credit. Using Calls, the P&L graph looks like this:

Long one call, strike A and short 2 calls, strike B. If both strikes expire worthless, the profit is the credit received. Maximum profit occurs with expiration exactly at the short strike, strike B. You start losing money when the stock moves higher than the interval between strikes A and B plus the credit received.

Let’s take a hypothetical example. XYZ is trading at 50. I buy 1 52.50 call paying 1.25 and I sell 2 55 calls at .75 for a .25 credit. Below 52.50, I make the .25 credit. At 55, the 52.50 call is worth 2.50, so I make 1.25 and the 55 calls expire worthless, giving me a total profit of 2.75, or $275 for every spread.

Where do I start to lose money? The difference between strikes A and B in this case is 2.50. So, at 57.50 plus the .25 credit, 57.75 is my breakeven. Above that, I lose money.

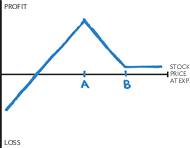

Now let’s take an example of the 1:2 ratio vertical spread using puts.

The P&L graph is the reverse image of the call example.

We are long one put strike B, short 2 puts, strike A. Our maximum profit is expiration at the short strike. Above strike B, we make the credit received, and we start losing if the stock is lower than the distance between strikes A and B minus the credit received.

Now I will use a real life example from March 17 at 10:05 CDT using Google (GOOG). With the stock at 550, I am looking at the 530-510 1:2 vertical put spread.

I can buy the 530 put 1 X at 11.50 and sell the 510 put 2 X at 6.50 for a nice 1.50 point credit. Let’s breakdown possible results at expiration: GOOG above 510 makes the credit, 1.50. At 510, my maximum profit is achieved, 21.50, or $2150 for every time I do the spread. I lose money at a price below the distance between strikes minus the credit received, making my breakeven point 508.50.

Because I am net short options, the clock is on my side. However, my risk is potentially unlimited. It would not be wise, for instance, to do a 1:2 call spread if the stock is a potential takeover candidate.

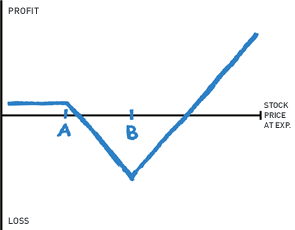

The flip side of the 1:2 spread is the 2:1 where I am long 2 options and short one option. This trade has potentially unlimited profits, but the clock is your enemy as the long options decay. The P&L graph using calls looks like this:

I am short 1 X strike A and long 2 X strike B. If strike A is at the money, I can probably do this for a credit. Any expiration below strike A makes the credit received. My point of maximum loss is on my long strike, strike B. This makes my breakeven higher than the interval between strikes A and B plus the credit.

Here is a real life example using Apple (AAPL) with AAPL at 126.40, I can sell one May 130 call at 4.30 and buy 2 May 140 calls at 1.60, giving me a 1.10 credit. Below 130, I make 1.10. At 140 exactly, I lose 8.90 or $890 every time I do the trade. My breakeven is 131.10, that being the distance between strikes plus the credit. And above 140, I make potentially unlimited money.

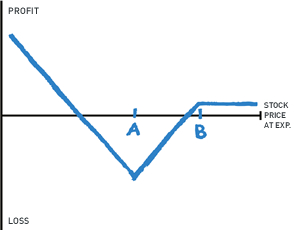

The 2:1 spread using puts looks like this when done for a credit:

I would do this if I thought a stock were going to crash and have a resultant explosion in implied volatility. Long 2 X strike A, short 1 X strike B. My worst case scenario is expiration at strike A, and my best case scenario is the stock going to zero, admittedly something that doesn’t happen very often.

Let’s use Tesla (TSLA) as an example. With TSLA at 194.20 I can buy 2 May 155 puts at 4.50 and sell one May 175 put at 9.35, giving me a .35 credit, which I make on any expiration above 175. My maximum loss is expiration on the long strike (have you noticed that best case scenarios are expiration on the short strike and worst case expiration on the long strike? This is true of all option spreads) 155 is where I lose 10.65. My breakeven is 174.65 and below that I make money.

So, which do you choose, 1:2 or 2:1? You choose 1:2, if you expect either no move or a slow and steady move to the short strike coupled with a decline in implied volatility and the 2:1 if you expect a pop in volatility coupled with a big move.

I am neither advising nor recommending any of the above trades. I am an options educator and not a financial advisor. I am simply illustrating examples of the many and varied possible options strategies.

#####

If you would like to get more from Randall Liss and The Liss Report, please click here.