So far, 2015 has been fairly light on high-buzz, high-growth tech-related IPOs, but that figures to change this week with Fitbit’s (FIT) 29.9 million share IPO. As of this writing, the deal is expected to price within a range of $14-$16, but, given the buzz — and it’s very impressive growth rates — it wouldn’t be a surprise if the price range was lifted before it launches on Thursday, June 18.

With the company offering nearly 30 million shares, the float is on the larger side, especially relative to most IPOs this year. However, demand should be healthy enough to comfortably soak up the higher supply of shares, considering the enthusiasm for the deal. The IPO also boasts of a tier one lead underwriting team of Morgan Stanley, Deutsche Bank, and BofA Merrill Lynch.

Closer Look at FIT

Fitbit is the maker of six wearable, connected health and fitness trackers. Some of the devices are wrist-based, similar to a watch, and some are “clippable” onto a person’s clothes. All of its devices are capable of tracking users’ daily steps, calories burned, distance traveled, and floors climbed. The MSRPs for its products range from $59.95-$249.95.

Most of its devices also measure sleep duration and quality, while its more advanced products track heart rate and GPS-based information such as speed, distance, and exercise routes. Further, some of its more advanced devices feature higher integration with smartphones, including the ability to receive call and text notifications, and play music.

FIT is more than a solely a device maker, however. It generates additional revenue through premium subscription offerings, such as Fitbit Premium, a virtual trainer, and FitStar, which provides interactive video.

FIT Growing Rapidly, But…

There are a couple broader trends worth highlighting that should provide a tailwind for the company. For instance, people have become more health conscious, paying more attention to diets and fitness. To put this trend into some context, FIT estimates that in 2014, consumers spent over $200 billion on health and fitness services like health club memberships, weight management services, dietary supplements, etc.

Of course, the wearable device market is also growing very rapidly. According to IDC, in 2014, shipments of wearable devices more than tripled year/year, reaching a total of 19.6 million units shipped. By 2019, IDC expects the market for wearable devices to reach 126.1 million units shipped in 2019, representing a $27.9 billion worldwide revenue opportunity.

FIT also has a few company-specific catalysts lined-up that it should capitalize on. Specifically, it plans to continue investing heavily in research and development to further bolster its product line and platform through both internally-developed and acquired technologies.

Additionally, up to this point, most of FIT’s growth has come from the consumer sector. But, going forward, it intends to increase its focus on building relationships with employers and wellness providers, growing revenue through employee wellness programs.

Its’ Success is Drawing in Competition

So, the good news is, FIT is growing rapidly with plenty of opportunity ahead of it. The flip side of that coin is that its’ success is attracting a lot of attention from competitors. Apple’s (AAPL) new iWatch, for instance, has many of the same health tracking capabilities as FIT’s devices.

Also, Android-based smartwatches will compete in this space, along with Jawbone, which just recently filed two lawsuits against FIT: one for patent infringement and one alleging FIT recruited its’ employees, who took trade secrets with them to FIT.

Whether these lawsuits have merit remains to be seen, and the timing certainly raises some eyebrows as FIT is about to become flush with new cash, making it an easy target.

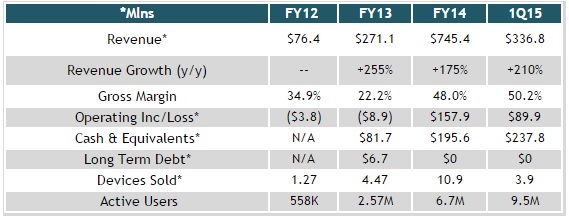

Financials

Taking a closer look at its 1Q15 results, revenue surged 210% to $336.8 million with a substantial majority of the increase due to the number of devices sold increasing to 3.9 million from 1.6 million in the year ago period. On a geographic basis, U.S. revenue grew $175.5 million, or 195%, and international revenue soared 276% to $52.4 million.

FIT’s expenses also saw sharp increases. Most notably, Sales & Marketing expense spiked 289% to $43.9 million and Research & Development was up 147% to $22.4 million.

Still, its’ astounding revenue growth and much improved gross margin more than offset the higher expenses, allowing it to generate $89.9 million in operating profit, up 469% year/year.

Lastly, we would expect the valuation to reflect a company with top-flight growth rates and compelling growth prospects ahead. But, based on the midpoint of the price range, its trailing P/S comes in at a very reasonable 4.1x FY14 revenue, and 2.3x annualized FY15 revenue.

Conclusion

Overall, its fundamentals are about as solid as we have seen from any IPO this year. The triple digit revenue growth is the most obvious attribute in its favor. But, there are several others as well, including its swing to profitability last year, its rock solid balance sheet, and a very reasonable valuation.

There are a couple blemishes and concerns to be aware of, though. Most importantly, heightened competition is a given. Apple’s (AAPL) iWatch and some Samsung devices have similar capabilities. And then there’s its main rival, Jawbone, which just filed two lawsuits against FIT, as mentioned earlier.

All in all, we expect FIT to have a very successful IPO this week, with a likely big pop when it opens for trading. Depending on the degree of that pop, FIT may still have some room to run due to its rather conservative price range.