Hey, Traders from around the world! I wrote a little number on bear put spreads last week. I figured I would just follow up with its sister, the bull call spread.

What: A bull call spread is a semi non-directional strategy involving two option legs: a call that you purchase and one that you sell. What I like about bull call spreads is it’s a limited return, limited risk strategy. It is cheaper than just straight up buying a call, even though there is some addition commission, due to the extra option leg. It also does not require any margin, like its cousin, the bull put spread.

How: If you are bullish to non-directional on a trade and perhaps it’s reaching a support and there’s no real confirmation, yet, that it will bounce. An example: Say you had just come up with a plan in advance to go bullish at a specific price. You could create a contingency order in a brokerage account if APC is at or near $60 (a strong support) you buy to open the $60 call and then simultaneously sell to open the $70 call, expiring in January. The $60 strike would cost approximately $4.00 per contract. The $70 strike would sell for approximately $0.74 cents. Therefore, the total debit on this trade would cost $3.26 per contract.

When: In my opinion, I get into bull call spreads on two occasions. If I already own a call and my analysis has determined the bullish trade could slow down for a few days or a few weeks, I’ll sell a call to bring in premium as the trade rests. The other situation is when a stock is approaching or at a very strong, confirmed support from prior price action. I’ll create a contingency order to simply buy the call and sell the call simultaneously, like in the above example of APC.

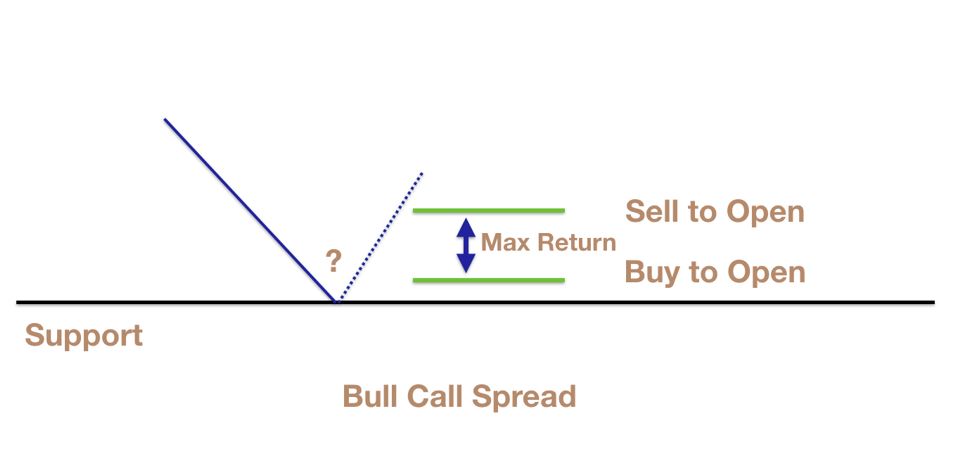

Where: At a support. The time frame of the trade is up to you. I like to keep the expiration dates the same, so there’s no calendar spread issues to worry about (like an in the money option being exercised at expiration prior to the other option).

Why: If you are bullish on a trade and expecting some buying at support. This strategy is often cheaper than buying a directional call. In the above example on APC, your risk is $3.26 your potential reward is $70 – $60 = $10. Therefore it’s a 1:3 Risk: Reward ratio in anticipation of APC bouncing. Below is an image of how I perceive this strategy.