This is going to be an interesting week. And not in a good way.

Four times a year the market produces what is called a “triple witching week” when stock index futures, options on the indices (including the VIX) and the futures, and options on individual stocks all expire more-or-less simultaneously. The need to rebalance portfolios and the confusion caused by price changes makes the market a little crazy. Prices swing all over the place.

This week is the triple witch. But it going to be much worse than normal.

This time the open interest in the expiring options – in effect the volume of option contracts outstanding – is much higher than normal. And the options are unbalanced, with more market participants holding Puts, which pay off if the market falls, than Calls, which pay off if the market rises.

There are an estimated $1.1 trillion in notional value of S&P500 options expiring on Friday morning, and about $6.7 billion – roughly two-thirds—are Puts. About $215 billion notional are Puts that pay off relatively close to or just below the current market price.

The amount the Put sellers have to pay increases at the same rate as the index falls. The bigger the drop, the more the institutions who sold Puts have to pay out. If the drop is big enough, some institutions will be bankrupted; others will be so badly damaged they may not recover. Think Lehman Brothers here.

That horrid prospect can be avoided if the market goes up – not too far, perhaps just enough to cover the 2050 strike price, say – instead of down.

Options are an all-or-nothing proposition. If you sold a Put that pays off at 2050, and the market at expiration is 2051, you pay nothing, and the guy you sold it to gets nothing. If the settlement price is 2025, you lose 25 points per contract and the guy you sold it to orders Krug by the case. There will be some large players trying to make sure the market goes up this week. And there will be equally large, well-funded players trying to make sure it goes down.

On Wednesday the Federal Reserve steps tentatively into this titanic struggle. The last Federal Open Market Committee meeting for the year starts on Tuesday, and on Wednesday the interest rate policy will be announced. The Fed has been loudly signalling that this time by Golly they really mean it! Interest rates will be increased. This is the last chance!

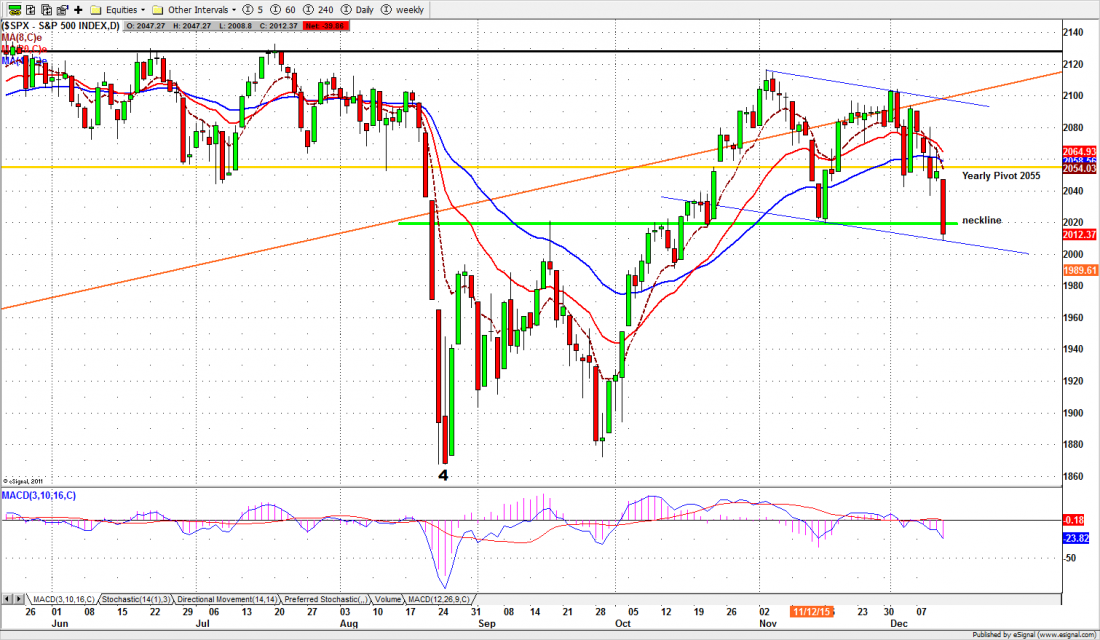

But the market is faltering – last week the SPX closed at 2012, about 80 points below the previous week – and a rate increase now might be enough to knock out all of the support, all the way down to 1830, the August low.

Oil has crashed, and taken the energy sector down with it. Two big junk bond funds have halted redemptions and as the price of junk has tanked the yields have become astronomical – above 17% by one measure, the highest since 2009. And the soaring US Dollar means a lot of the world can’t afford the stuff America wants to sell, so world trade is stagnant. No help from overseas, for the foreseeable future.

It will require a lot of courage – or stark insensibility – to raise rates for the first time in 84 months under these circumstances. There are already some straws in the wind to show the Fed is rethinking the whole nasty business, including what looks like a trial balloon floated via the Wall Street Journal Sunday evening.

Will the Fed tank the market the week before Christmas? We’ll find out Wednesday. But watch for some hairy price action before then.

Today

We are now trading the March contract in the S&P500 e-mini futures, symbol ESH6. Today a move below 1990 will be bearish, and if we break that level, expect a further decline to the 1965-75 zone. 2050-55 will be a key resistance and the 2035-40 zone will help defend it. We will likely see sellers coming in on any bounce up to these resistance levels.

Major support levels: 1990.50-92.25, 1975-72, 1962-58, 1950-45

Major resistance levels: 2025-28, 2045-50, 2075-72, 2088-93

Get free detailed market analysis from Naturus.com here: Naturus market analysis