I’ve been asked this question over the years and I always explain it with a metaphor because that just allows you to picture it clearly in your head.

I generally like to say; it’s like buying Toyota at the price of a Mercedes or BMW.

Sometimes I go as far as to say, it’s like buying a Toyota but at a Ferrari price.

LinkedIn (LNKD) is such an example.

For the poor shareholders who have owned the stock for the past 12 months, I’m not exactly sure what they were holding for or more importantly why they even bought into LinkedIn in the first place?

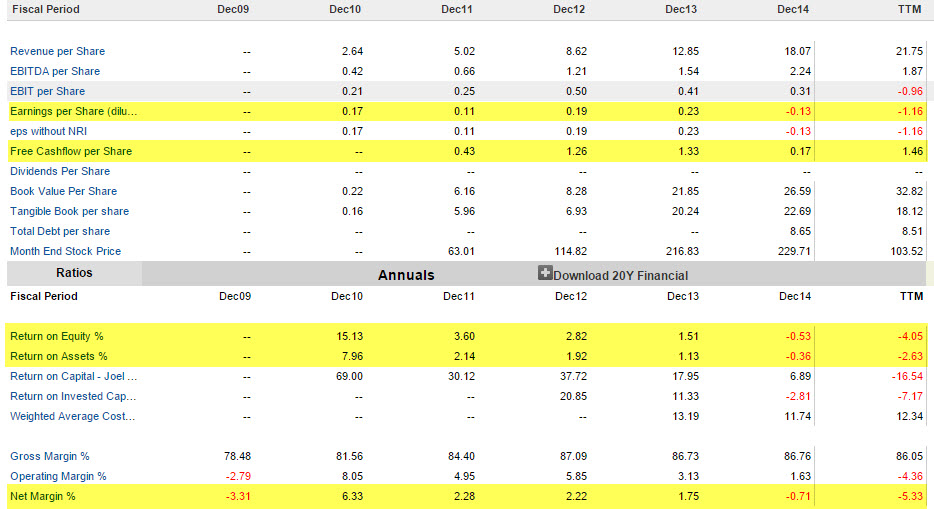

You just have to look at the numbers to clearly see there was a problem from day one when it floated and progressively got worse. The writing has been on the wall.

- Earnings per share currently at negative (Loss making)

- Free cashflow per share of just $1.46 which was over 185 times at its peak price above $270.00

- Return on Equity currently at negative but has been below 5 for a number of years

- Return on Assets also currently negative but below 5 for several years

- And Net Margin, which should be quite high for an online technology company, although negative, has been dismally low averaging a paltry 2% for the past few years. Google is over 20% consistently.

These five simple measures clearly shows LinkedIn (LNKD) would not even pass the most simplest of screening tests for further investigation. Or even valuation for that matter.

Be very careful on stocks like these, as they portray the events back in the late 1990’s tech boom where it was revenue and eyeballs and not actual profit which matters.

By simply avoiding these, your portfolio is already off to a good start.

See how you can easily protect yourself from stocks like LinkedIn, click here.