The markets are by very nature their noisiest at their most important moments. The noise punishes the early birds, paralyzes the indecisive and talks the tardy into better late than never. Early birds may take their losses or not maximize their profit potential. The indecisive discuss their 20/20 hindsight by the water cooler and the late sweat every tick against them for fear of risking more than they should be in the first place. There are so many ways to struggle with a well-reasoned plan of action. While at times I miss the excitement of the trading floor or the professional interactions of a trading desk, there is something to be said for the small independent office environment. It allows me to focus on the data. In the markets’ noisiest moments, like this past week in the bond market, the key to sticking with a trading plan. I’ll explain in detail as, I believe, there is plenty of meat left on this bone.

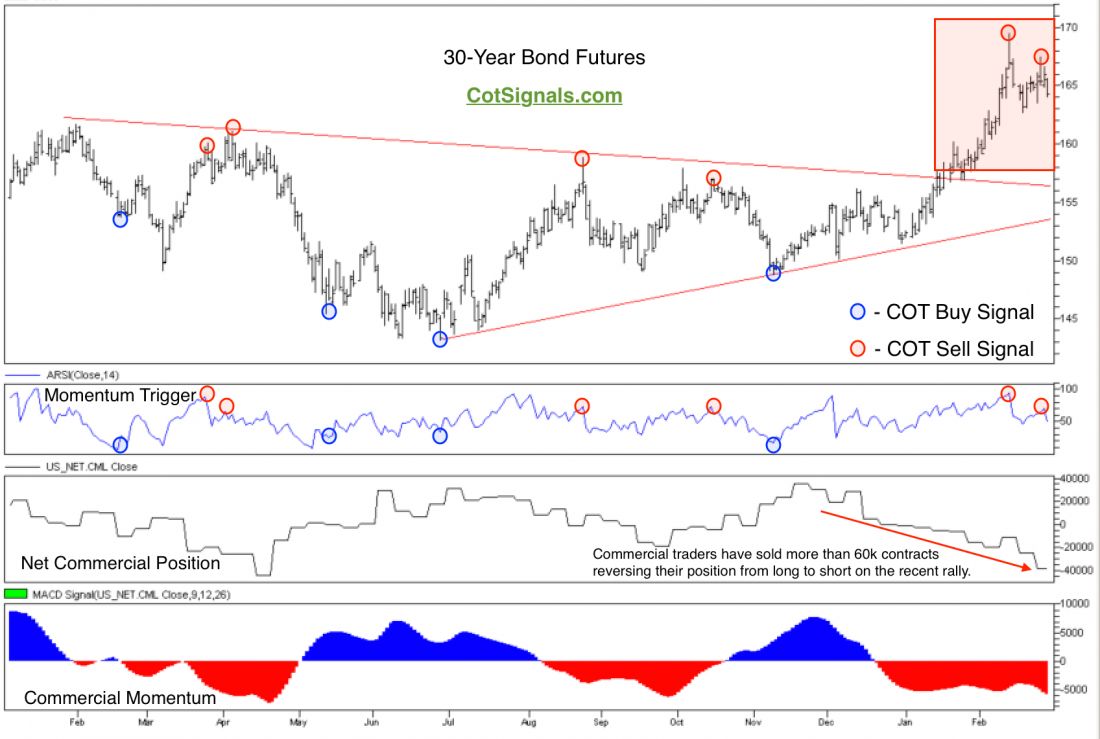

Many years ago as I began my foray into the Commitment of Traders report, I expected it to be useful in the agricultural commodities where the commercial trader category is made up of farmers and grain millers. As I expanded my research, I was surprised to see how good they were in the interest rate markets. Perhaps, even more successful than the ags, in general. You can see the Commitment of Traders signals generated over the last year on the chart below and this wasn’t an especially good year for their trading. Theoretically, it makes sense that the deepest futures markets in the world are made up of a connected group of traders through various networks employing the brainiest people they can find. This combination has served them well. Now, to the current action.

Commercial traders are typically the mirror image of the large speculator group. The most important distinction is that the large speculators don’t have to participate in any markets or market action. Their involvement is purely profit driven whereas the commercial population is bound to the market by the fundamental production or, consumption of a given commodity. In this case, the commercial traders are hedging their interest rate risk. Beginning in December, the commercial traders had positioned themselves on the long side of the market, expecting lower rates and higher prices. Meanwhile, the large speculator population had all ganged up on the short side based on the Federal Reserve Board’s first rate hike in years. The commercial traders, perhaps reading beyond the domestic news front, clearly saw global weakness on the horizon and knew that it would at least give pause to the Fed’s intended actions. The global weakness caused an about face that consisted primarily of a short covering rally by an ill-advised large speculator population.

As you can see on the chart, commercial traders have continued to aggressively sell the long end of the yield curve, selling more than 60,000 contracts since mid-December. Conversely, the large speculator population has not only covered their short positions (at a loss) but has now reversed and are now long more than 23,000 contracts. What we know is this: The large speculators have been consistently wrong at the most inopportune moments. The last time they were generally right was November of 2014. In the meantime, they accumulated their largest net long position within a week of the 2015 high and they had their largest short position in a year just as the market began a significant breakout and move higher. We expect the large speculators to get this one wrong as well. We’ll focus on the data and that puts us on the side of the big, interconnected money and sell the June 30-year Treasury Bonds accordingly. As always, we’ll keep a protective stop resting above last week’s high of 167^15. Finally, we’ll look for commercial buying support to come in near the trend line that defined the market’s breakout in December.

Please join us for a free 30-day trial of CotSignals.