There are no shortage of articles touting Research in Motion (RIMM) as the next Palm, which had to sell itself earlier this year as its current business model proved unsustainable. What all of these “analyses” seem to omit, however, is a comparison of the financial situation of the two companies. Instead, the comparisons appear to be made based on sentiment (which can change in a hurry – consider that RIMM stock traded about 70% higher just four months ago) and predictions several years out (which is almost impossible to do!), rather than on the financial data which could illustrate just how similar the two companies are. In this article, I attempt to make the financial comparison.

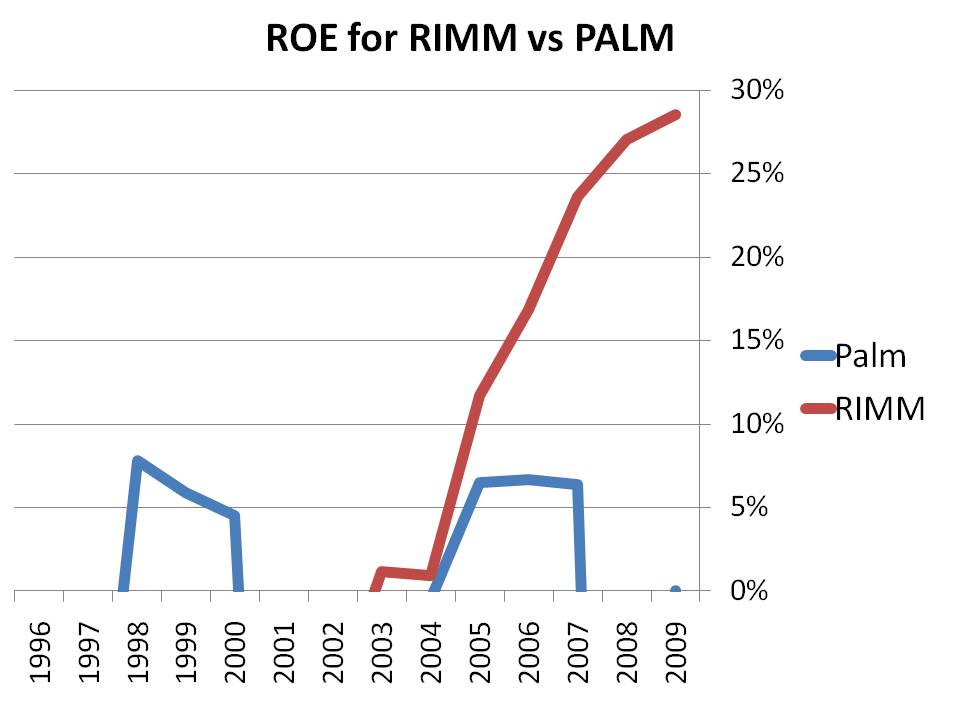

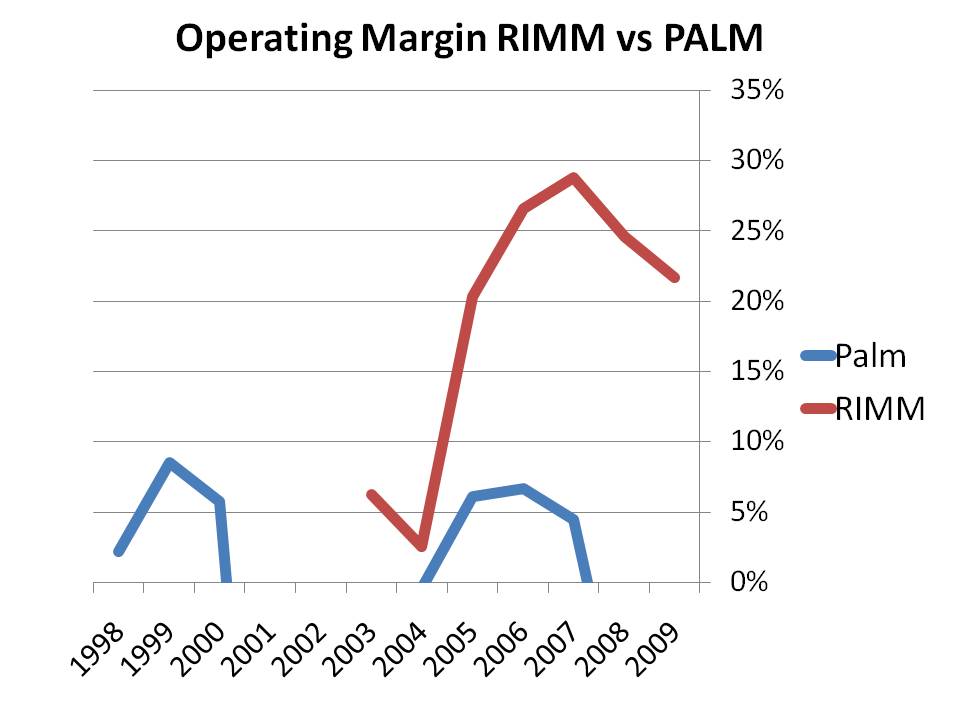

In the fifteen year record of Palm’s existence, it generated an operating income in just 6 of those years. The best operating margin it could ever manage was 8.5% (1999) at the height of the tech bubble. In no single year did Palm ever generate a return on equity of over 10% (the closest was 7.8% in 1998), even though it was considered the leader in its industry during that period.

RIM, on the other hand, operates at very high margins and generates returns on equity that are extremely high. The following charts illustrate how RIM has been more profitable in each of the last five years than Palm was even in its best year:

When an industry grows at a 25% rate despite a recession, there is room for success for many companies. The success of one or two companies (e.g. Apple, Google) does not preclude the success of other companies. Investors who predict the demise of companies generating ROE’s of 30% in growing industries are ignoring the most fundamental and basic aspect of whether a company is sustainable: its financials.

In a similar way, GameStop (GME) is often touted as the next Blockbuster. But an examination of the financials shows that these two companies are nothing alike, and never have been. While one barely snuck by, even in its “good years”, the other continues to deal from a position of financial strength that the former never had. That again appears to be the case here with RIM and Palm. But investor sentiment is so low, that RIM trades at a P/E below 10 once its cash balance is factored in.

Disclosure: Author has a long position in shares of RIMM