Courtesy of Ron Rutherford, Sabrient Systems and Gradient Analytics

The ISM reports showed mixed signals this time as the PMI (manufacturing) missed the consensus mark by 0.3% at 49.8%, and the NMI (non-manufacturing) beat the consensus by 0.6% at 52.6%. Although muted as usual, the Dow’s initial reactions were in the same direction as the consensus miss and later, the consensus beat. Both indexes were inside the consensus range provided by Econoday (Mfg and Non-Mfg).

The manufacturing sub-indexes showed positive signs in production, up 0.3% to 51.3%; new orders were up 0.2% but stayed below 50% at 48%; and prices were up 2.5% to a more acceptable 39.5%. Prices down might be good overall but sustained price level drops can lead to the dreaded deflation. The biggest negative in the manufacturing report was the drop in employment of 4.6% to 52%. It maintained above 50 but the trend is clearly downward from 57.3% in April 2012. If it continues to decline, a drop below 50% signifies contraction in employment.

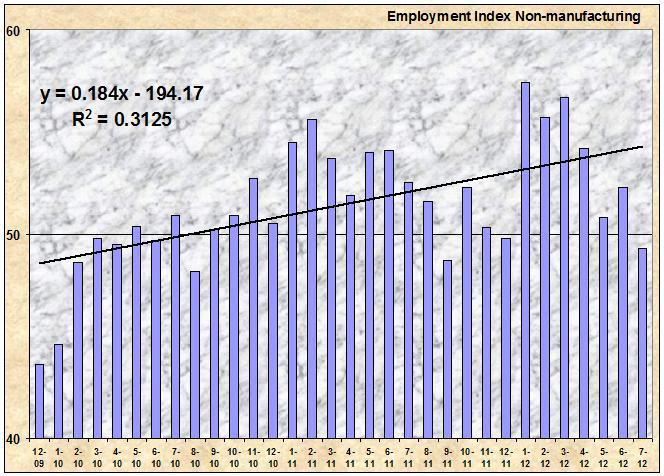

The non-manufacturing employment index also dropped significantly by 3% to 49.3%, breaking the 50% mark, meaning the hiring rate is contracting. But for the non-manufacturing sectors, there were extenuating facts that might indicate a potential snap back in this index in the near future. For example, new orders rose 1% to 54.3%; business activity jumped substantially by 5.5% to 57.2%; and new export orders was up 1.5% to 51%. Below is a graph of the non-manufacturing employment index since December 2009. Hopefully this time we bounce back above 50% just as we have done for the past couple of years.

(Click to enlarge)

Investors often have the mind set of Goldilocks. That is, they want good numbers, but not too good, or too low. The price index is one such index that is justified in the Goldilocks approach. Prices rising too fast or dropping too quickly spell trouble for the future of the economy. As noted above, the manufacturing price index increased last month but still was anemic at 39.5%. Non-manufacturing increased 6% to an acceptable mid-fifty value of 54.9% after two months of contraction below the 50% mark.

Besides the price indexes, the Macro View also is also concerned with commodities rising in price and those declining in price. Not only can it be a portent of potential problems in the

…