Agricultural stocks have sprouted nicely in 2010, is now the time to harvest the crops and head home? Persistent takeover chatter in Potash Corporation of Saskatchewan (POT), and more recently in CF Inudstries Holdings (CF), illustrate demand for potash makers and extreme bullishness in the agricultural sector. Adding fuel to the fire was Friday’s USDA Crop report. In general, a confluence of a factors are positioning the ‘ferts’ as a new frontier of investing.

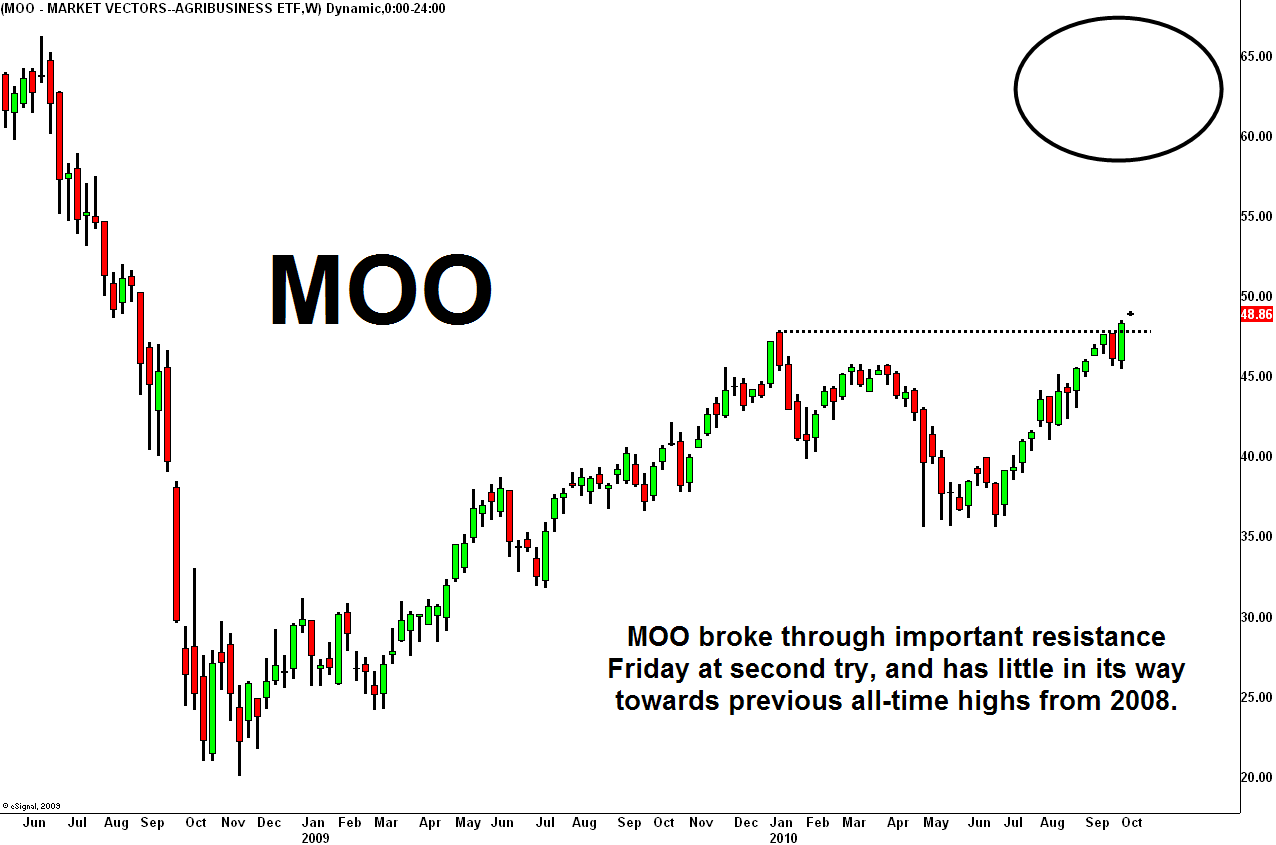

The Market Vectors Agribusiness ETF (MOO) hit 52-week highs Friday, and continued this morning above $49, representing almost a 40% gain from its 52 week lows back in July. Friday morning, a USDA report and another takeover rumor, this time in CF Industries Holdings (CF), provided further cause for optimism. The fertilizer names have been the group-du-jour, with global firms looking to snatch up leading names at perceived bargain basement prices. Investors are now left wondering: can we still buy into the sector given the recent run higher? The answer is: I don’t see any reason why not.

Friday’s USDA Crop Report showed a decrease in supply of corn, soybeans and wheat, a big boost for fertilizer makers. Adding to Friday’s momenetum was buyout speculation in CF Industries Holdings (CF) from Rio Tinto Group (RTP), which is interested in adding a potash maker to its holdings. CF finished up more than 12.5% Friday, leading the group higher. Other names in the sector boosted by the double dose of good news include Agrium Inc. (AGU), Mosaic Company (MOS), and Potash Corp. of Saskatchewan (POT).

Back in August, a Financial Times front-page article cited a 35% rise in raw materials prices since early 2009 as evidence of a ‘commodities supercycle’ driven by the industrialization of emerging countries. Takeover speculation has been rife in the fertilizers all year, headlined by the ambitious August 16th BHP Billiton (BHP) bid for Potash Corp. of Saskatchewan (POT)—the Canadian company that owns around 20% of the world’s potash supply. The $130/share BHP bid, which at the time represented a nearly 20% premium for POT shares, was deemed very inadequate. Today, several sources are reporting there are other firms that may look to top BHP’s bid. Chinese firm Sinochem, in a possible joint bid with Indian firm National Mineral Development Corporation (NMDC), has been mooted. Britain’s Sunday Telegraph reported this morning that PotashCorp is even considering a break-up to avoid relinquishing control at what it perceives as depressed prices. They would sell nitrogen and phosphorous assets, pay a $70 per share dividend, and increase debt. Strong earnings last Monday from Mosaic Company (MOS), along with the CF buyout rumor, helped reinforce a bullish view in the sector. The Potash Corp. board cited the following reasons, among others, for rejecting the bid outright:

•The BHP Billiton offer fails to reflect PotashCorp’s prospects for continued growth and shareholder value creation

•PotashCorp’s financial advisors have each provided a written opinion to the Board that the consideration being offered pursuant to the BHP Billiton offer was, as of the date of such opinions, inadequate, from a financial point of view, to shareholders (other than BHP Billiton and any of its affiliates).

•Superior offers or other alternatives are expected to emerge.

The fundamental demand driver for potash is that there is limited arable land around the world on which to grow crops. Countries like India, which has no arable land, and China, which has been dealing with severe droughts, need nutrient-rich potash in order to create soil suitable for growing crops. In addition, last year farmers in the US, uncertain about future demand for crops due to the economic recession, held off on stockpiling potash reserves. This year, it is forecasted that farmers will more aggressively buy up fertilizer in anticipation of higher demand. High initial start-up costs for starting potash production are also driving the demand for takeovers within the sector.

From a technical perspective, the agricultural stocks also look like they have room to run. While it is important to avoid chasing extended stocks, it is also crucial to recognize when strength is simply a sign of better things to come. It would be nice to get a pull-back, but I can’t object to paying up at this point for a longer-term hold. POT’s resistance toward potential takeovers, and further rumors regarding Rio Tinto and CF, confirms what the chart is telling us: the future is bright for the ‘ferts’. It is also important to consider companies who will feel the residual effects of higher crop prices after the USDA. Farm equipment makers Deere & Co. (DE), Agco Corp. (AGCO) and CNH Global NV (CNH) benefited from the Friday’s news, while meat processors like Tyson Foods Inc. (TSN), Sanderson Farms Inc. (SAFM) and Smithfield Foods Inc. (SFD) closed sharply lower Friday.

Look to play the Market Vectors Agribusiness ETF (MOO), which is heavily weighted towards fertilizers, to gain exposure to the entire agricultural sector while avoiding the potential for headline risk.

|

Top 10 Fund Holdings for MOO (as of 10/08/2010)

|

|||||

|

Number

|

Holding

|

Ticker

|

Shares

|

Market Value

|

% of net

|

|

1

|

Deere & Co

|

DE

|

2,220,999

|

$168,039,763.65

|

8.53%

|

|

2

|

Mosaic Co

|

MOS

|

2,390,085

|

$156,813,476.85

|

7.96%

|

|

3

|

Potash Corp of Saskatchewan Inc

|

POT

|

1,000,582

|

$145,884,855.60

|

7.41%

|

|

4

|

Wilmar International Ltd

|

WIL (SP)

|

31,580,751

|

$145,552,196.58

|

7.39%

|

|

5

|

Monsanto Co

|

MON

|

2,640,781

|

$135,077,758.63

|

6.86%

|

|

6

|

Syngenta AG

|

SYNN (VX)

|

343,967

|

$91,593,570.55

|

4.65%

|

|

7

|

Archer-Daniels-Midland Co

|

ADM

|

2,641,636

|

$86,804,158.96

|

4.41%

|

|

8

|

Yara International ASA

|

YAR (NO)

|

1,677,901

|

$80,874,052.73

|

4.11%

|

|

9

|

BRF – Brasil Foods SA

|

BRFS

|

5,020,448

|

$75,658,151.36

|

3.84%

|

|

10

|

Sociedad Quimica y Minera de Chile SA

|

SQM

|

1,514,489

|

$74,285,685.45

|

3.77%

|

While the agricultural stocks have enjoyed a huge run this year, the end of the road isn’t anywhere in sight. The PotashCorp takeover battle looks set to rage on as many companies around the world right for the prize. The future for the ‘ferts’ is bright, and they should in some form be part of your balanced asset portfolio moving forward.