Anti-Claud is coming to town!

Anti-Claud is coming to town!

You’d better not print, you’d better not ease you’d better not contract or your wages will freeze – a real Central Banker is coming to town… Jean Claude Trichet has a lunch meeting at the NY Economic Club and there is no one who knows better when Bernanke’s sleeping and when the recovery is fake, so we’d better pay attention, for the country’s sake! THIS is the most powerful banker in the World, not the hollow bank puppet we have setting US policy and Trichet has fought easy money tooth and nail, even as the US embraced it this year.

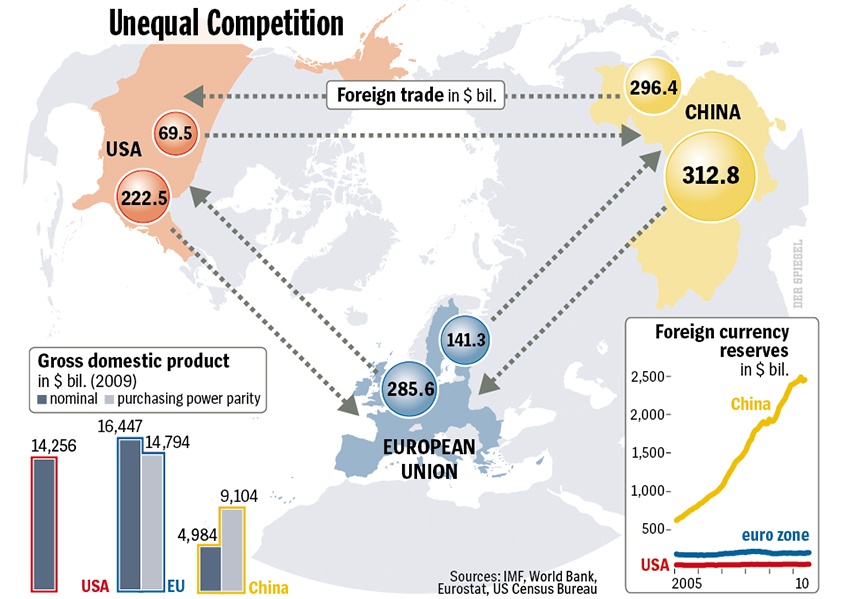

As you can see from the Chart on the right, Europe is a bigger (slightly) trading partner of China than the US and a MUCH bigger buyer of US goods than China by a factor of 3. The strong Euro lowers Europe’s trade imbalance as they have to send less Euros to both the US and our peg-partners in China for the same amount of goods they bought last year while the same goods they sold last year ship out in exchange for larger amounts of foreign notes.

With the Bank of Japan this week boosting its asset- purchase plan and the U.S. Federal Reserve mulling a similar shift, Trichet said last week that ECB policy makers are in the “same mood” as a month ago and for now remain committed to phasing out their unlimited lending program. That boosted the Euro back to $1.40 for the first time since February. The ECB and Fed compose “two different schools of thought,” said Jacques Cailloux, chief European economist at Royal Bank of Scotland Group Plc in London. “The ECB is looking at their own economy and seeing some signs of a revival. They’re very concerned about going down the line of the Fed.” Now Mr. Trichet will attempt to school us this afternoon – not coincidentally, on the same afternoon that the Fed Minutes will be released and QE2 mania is likely to peak out.

As noted yesterday by Zero Hedge, “While risk assets may hit all time highs courtesy of free liquidity, the economy, also known as the middle class, will be stuck exactly where it was before QE2… and QE1.” The article does a great job of outlining my long-standing premise that money simply cannot be printed fast enough to overcome a drop in velocity and,…