EUR/USD

The Euro was confined to narrower ranges during Thursday with a phase of consolidation following sharp gains triggered by the central bank cut to swap rates the previous day.

There was a flurry of political rhetoric ahead of next week’s EU Summit as French President Sarkozy in particular warned over the efforts required to prevent a break-up of the Euro area with a call for Treaty changes. There was a clear warning from political and banking figures that the moves to boost liquidity will help ease immediate tensions, but that there are still severe structural difficulties.

The underlying plan still appears to be that major leaders will seek political concessions from the Euro-zone countries which would push them much closer to rapid fiscal integration. In return, there will be increased support for peripheral economies. The ECB also suggested that if there was a move to guarantee fiscal rules then the ECB would consider providing additional support. Tensions will inevitably increase ahead of next week’s summit given fears that failure or an inadequate response would trigger a terminal escalation of the crisis as capital outflows would intensify.

The US PMI manufacturing data was stronger than expected with an increase to 52.7 for November from 50.8 previously and there was a significant recovery in both the orders and prices components which continued to suggest that the economy is making some headway. This speculation will be confirmed if there a stronger than expected employment release on Friday. The dollar impact will again be mixed as potential yield support would be offset by reduced defensive demand for the US currency.

Regional Fed President Bullard hinted that there would be no major policy moves at the December FOMC meeting, although there was increased speculation that there would be a technical cut in the discount rate and the Euro drifted below the 1.35 area.

Source: VantagePoint Intermarket Analysis Software

Call now and you will be provided with FREE recent forecasts

that are up to 86% accurate* 800-732-5407

If you would rather have the recent forecasts sent to you, please go here

Yen

The dollar found support on dips to the 77.50 area against the yen on Thursday and pushed to the 77.80 area in Asian trading on Friday. A run of generally more favourable US data releases helped underpin the dollar against the Japanese currency.

The latest Japanese capital spending data was weaker than expected with a 9.8% decline for the third quarter after a 7.8% fall the previous three months which will maintain fears over a structural lack of demand within the economy.

There will be some reduction in defensive yen demand if global central banks can foster a mood of increased confidence, but funds will inevitably remain very cautious in the short term and there is little prospect of aggressive moves into overseas securities.

Sterling

Sterling found support on dips to the 1.5650 area against the dollar on Thursday and pushed to test resistance in the 1.5750 area, but was unable to break higher and dipped again late in the US session.

The PMI manufacturing index dipped to the lowest level since July 2009 at 47.6 from a revised 47.8 previously. There was a further downturn in orders and the rate of decline in employment was also the highest for over two years which maintained fears surrounding the economic outlook.

Following the latest Financial Stability Review, Bank of England Governor King again warned over the risk of a renewed credit crunch in the economy and also warned in uncompromising terms over the dangers posed by the Euro-zone crisis. There will be unease surrounding the UK banking sector and the impact on lending. It will also be dangerous to assume that defensive capital inflows will continue.

Swiss franc

The Euro found support on dips towards 1.2250 against the franc on Thursday and rallied back above the 1.23 level during US trading as the dollar also again found support below the 0.91 level.

GDP advanced 0.2% for the third quarter which was in line with expectations while the PMI index dipped further to 44.8 for November from 46.9 previously.

The government warned that it would consider supporting pushing interest rates into negative territory to help the National Bank combat any fresh strengthening of the Swiss currency, although it also stated that monetary policy remained in the central bank’s control. The talk of negative interest rates inevitably pushed the currency weaker and there was also reduced scope for defensive demand as risk appetite maintained a steadier tone.

Source: VantagePoint Intermarket Analysis Software

Call now and you will be provided with FREE recent forecasts

that are up to 86% accurate* 800-732-5407

If you would rather have the recent forecasts sent to you, please go here

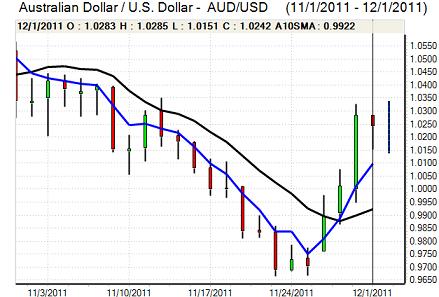

Australian dollar

The Australian dollar found support on dips to below 1.02 on Thursday and rallied to a high around 1.0260, but it was unable to sustain momentum and edged back towards 1.02 with some consolidation inevitable after the strong gains seen during Wednesday.

International risk considerations continued to dominate and, although the market tone remained more positive, there were still major doubts surrounding the regional outlook. There were also still important underlying unease surrounding the global banking sector which continued to curb Australian dollar demand.