EUR/USD

The Euro found solid support on retreats during Friday and advanced to fresh 8-week highs later in the US session with a move above 1.36 against the dollar.

The German economic data remained favourable with a further increase in the IFO business-confidence index to 110.3 for January from a revised 109.8 the previous month and there will be optimism that Germany will be able to lead the Euro-zone as a whole.

The Spanish government’s decision to effectively nationalise the savings banks was also received favourably and there was a further decline in yield spreads between German and Spanish bonds which helped underpin Euro confidence. There will still be very important medium-term vulnerabilities which will deter Euro buying once the period of short covering has subsided.

There were no major US releases during the session, although markets remained cautiously optimistic over the near-term trends with fourth-quarter GDP due late this week. Before then, the Federal Reserve will announce its interest rate decision on Wednesday and there will need to be a shift in the Fed’s rhetoric to trigger a major shift in dollar sentiment. Without such a change, the US currency will not be in a strong position to gain renewed support.

The Euro will, therefore, be underpinned as long as there is greater optimism that the very important structural vulnerabilities can be kept under control and the currency was fluctuating around 1.36 in early Asia on Monday.

Source: VantagePoint Intermarket Analysis Software

Call now and you will be provided with FREE recent forecasts

that are up to 86% accurate * 800-732-5407

If you would rather have the recent forecasts sent to you, please go here

Yen

The dollar drifted weaker against the yen during Friday and retreated to test support near 82.50. The dollar did find support close to 82.50, although the main movements were on the crosses.

The improvement in confidence towards the Euro-zone and currency was illustrated by another Euro advance to an 8-week high against the Japanese currency. There will be expectations of further official Euro-zone bond buying which could also trigger wider capital outflows from Japan.

The commodity currencies have not been able to make fresh headway which will tend to curb yen selling to some extent. Finance Minister Noda repeated comments that yen strength and potential downside risks to the economy needed to be monitored closely.

Sterling

Sterling consolidated just above the 1.59 area against the dollar ahead of the UK data releases on Friday. The latest retail sales data was weaker than expected with a headline decline of 0.8% for the month. The data is likely to have been distorted by adverse weather conditions, but there will still be fears over an underlying slowdown in consumer spending.

The latest mortgage lending data also remained weak with new advances provisionally at the lowest level since March 2009. The weakness in lending will maintain fears over the housing sector and a wider lack of credit within the economy which will stifle growth. The advance fourth-quarter GDP data and the latest government borrowing data will be watched closely on Tuesday for further evidence on growth trends.

Inflation will also remain an extremely important focus in the near term with the latest Bank of England minutes due on Wednesday when a switch to a clear tightening bias is possible. There will also be increased media report surrounding the risks of stagflation with weak growth at the same time as higher inflation which will tend to undermine Sterling and MPC member Posen retained his dovish stance in comments on Friday.

The UK currency was able to re-challenge the 1.60 area on wider dollar weakness where selling pressure increased again and the UK currency was trading weaker than 0.85 against the Euro.

Source: VantagePoint Intermarket Analysis Software

Call now and you will be provided with FREE recent forecasts

that are up to 86% accurate * 800-732-5407

If you would rather have the recent forecasts sent to you, please go here

Swiss franc

The Euro dipped weaker against the Swiss franc during US trading on Friday, but it recovered quickly and generally traded above the 1.30 level. The dollar hit selling pressure close to 0.9680 and weakened to near 0.9550 before finding support.

The Euro-zone developments continue to have an important impact on the Swiss currency and a reduction in immediate fears surrounding the Euro area will continue to curb defensive demand for the franc. Further weakness would also ease pressure for National Bank intervention and volatility is liable to remain high.

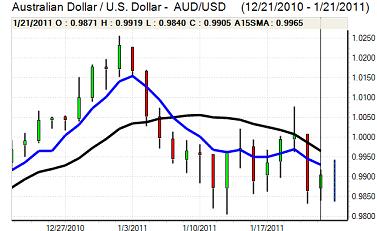

Australian dollar

The Australian dollar found support on dips to the 0.9850 area against the US dollar on Friday, but failed to break above 0.9920 and was generally on the defensive during Asian trading on Monday.

There has been further weakness in metals prices which is having a negative impact on the local currency, especially as there are still important uncertainties surrounding the impact of flood damage on key export sectors. There is still likely to be solid buying support on retreats given the underlying yield advantage.