Leading up to Noodle’s (NDLS) IPO on June 28, there was some decent buzz surrounding the deal. Certainly, expectations skewed to the bullish side with the general feeling that its 5.4 million share IPO would price well and find solid demand. But, few could’ve anticipated just how strong that demand would be.

The fast-casual restaurant IPO harkened back to the dot-com boom days in the late 90s as the deal priced at $18, well above the $13-$15 expected price range, and opened for trading a whopping 83% above its IPO price. But, it wasn’t done just yet. Over the next few sessions, it continued to charge higher, making highs at $52/share on July 7 – a staggering 189% higher than its IPO price.

The incredible opening performance begs the question: “What is it about NDLS that is so enticing to investors?” There are a few items. First, as we discuss below, its growth has been strong and its financials are healthy, overall. Also, two of NDLS’ closest competitors – Chipotle (CMG) and Panera Bread (PNRA) – had much higher P/S multiples (and stock prices) than NDLS when its IPO hit. Specifically, prior to its opening, NDLS had a 1-year trailing P/S of 1.3x compared to 4x for CMG and 2.5x for PNRA.

And lastly, speaking of CMG, the company’s CEO and CFO both came over from CMG in 2005. Given their track record of success, growing CMG into a power in the fast-casual market, investors are anticipating they will repeat their performance with NDLS.

CLOSER LOOK AT NDLS

NDLS is a fast casual restaurant concept offering lunch and dinner. Restaurants offer a variety of cooked-to-order dishes, including noodles and pasta, soups, salads and sandwiches. NDLS’ mantra is to deliver fresh ingredients and flavors from around the world under one roof—from Pad Thai to Mac & Cheese. There are 343 restaurants, comprised of 291 company-owned and 52 franchised locations, across 26 states and the District of Columbia, as of May 28, 2013. On average, patrons spend $8 per visit.

The company has been through a couple notable changes since opening its first location in 1995. The first big event occurred in 2005 when the company appointed Kevin Reddy as CEO and Keith Kinsey as CFO. The two came over from Chipotle (CMG), where Reddy was the COO, Chief Operations Officer and restaurant support officer and Kinsley was in an operations leadership role.

The next significant event for NLDS occurred in late 2010. This is when a private equity consortium led by Catterton Partners acquired a controlling interesting in Noodles and Company. At the time, the two parties settled on a fair value of $8.67/share.

FINANCIAL REVIEW

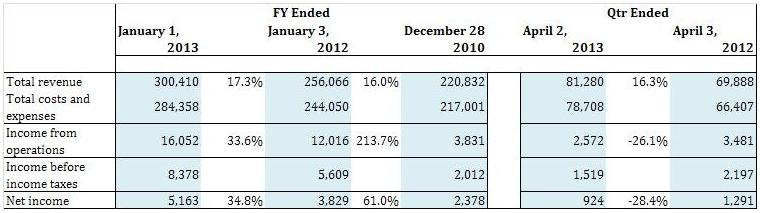

NDLS has very clean financials highlighted by consistent growth and profitability. Revenue and income from operations have grown from $170 million and $2 million in 2008 to $300 million and $16 million in 2012. In addition, the company has been cash flow positive for at least the past three years.

Turning to locations, from 2004 to 2012, NDLS increased the number of total restaurants from 100 to 327, representing a CAGR of 16.0%. Importantly, NDLS can fund new restaurant growth through operational cash flow.

Another strong metric, NDLS has posted consistent same store sales growth at its restaurants. In fact, in 28 of the past 29 quarters NDLS has achieved positive comps due primarily to increased traffic. NDLS’ balance sheet is relatively clean with only $34 million in debt following the IPO. Funding is a little short, however, with only $1 million in cash on hand.

IN CONCLUSION

NDLS’ start has been nothing short of stunning. With its current return of about 160%, there is only one IPO so far this year that can top that: 3D printing company ExOne (XONE), up an astounding 265%.

There is certainly much to like with the story. Revenue growth has consistently been in double digit territory; comparable restaurant sales have be steady, higher in 28 of the past 29 quarters (+5.2% last year); earnings are expanding; it has a lot of room to expand, its management team has a track record of success, most notably with CMG; and its valuation was attractive at the time of its IPO.

The question now is, with the stock shooting straight higher, is it too late for new investors to become involved? Its valuation is no longer that attractive with a trailing P/S of 3.5x, putting in between CMG’s 4x and PNRA’s 2.5x. Also, given the huge gains, some investors and traders will be looking to flip out of the stock soon, looking to lock in those gains. We’d also point out the very small float of – only 5.4 mln shares involved – so the stock is prone to rapid moves, in either direction.

With this in mind, it may be prudent for new investors to wait for it to cool off before taking a position. The fundamentals are there, but, chasing it may not be a recipe for success at this point.