Thoughts from the Frontline Weekly Newsletter

July 10, 2009

In this issue:

The End of the Recession?

The New Normal Is Still In Our Future

The Hidden Problem Within Unemployment Data

Was Income Really Up?

Tulsa, London, and The Baltics

There is no doubt that the US is in financial trouble. Those talking of a strong recovery are just not dealing with reality. But the US is in better shape than a lot of countries. This week, we begin by looking at Japan. I have written for years about how large their debt-to-GDP ratio is, yet they keep on issuing more debt and seemingly getting away with it. But now, several factors are conspiring to create real problems for the Land of the Rising Sun. They may soon run into a very serious-sized wall. And it is not just Japan. Where will the world find $5 trillion to finance government debt? We look at some very worrisome graphs. Those in the US who think that what happens in the rest of the world doesn’t matter just don’t get it. There is a lot to cover in what will be a very interesting letter. I suggest removing sharp objects or pouring yourself a nice adult beverage.

This Is Outrageous

But first, I want to direct the attention of those in the US finance industry to a white paper written by Themis Trading, called “Toxic Equity Trading Order Flow on Wall Street.” Basically, they outline why volume and volatility have jumped so much since 2007; and it’s not due to the credit crisis. They estimate that 70% of the volume in today’s markets is from high-frequency program trading. They outline how large brokers and funds can buy and sell a stock for the same price and still make 0.5 cents. Do that a million times a day and the money adds up. Or maybe do it 8 billion times. It requires powerful computers, complicity of the exchanges (because the exchanges get paid a lot), and highly proximate computer connections. Literally, the need for speed is so important that to play this game you have to have your servers physically at the exchange. Across the river in New Jersey is too slow. Forget Texas or California. This is a game played out in microseconds.

The retail world doesn’t get to play. This is a game only for big boys who can afford to pay for the “arms” needed to fight this war. But the rest of us pay for the game, as that half cent is like a tax on transactions, not to mention the increased daily volatility, which skews pricing. Think it doesn’t affect you? That “tax” is paid by mutual funds, your pension fund, and every large institution.

Frankly, this is outrageous. The more I read the madder I got. And it is going to get worse as computers get faster and software more intelligent. We need rules to level the playing field. Themis suggests one simple one: just make it a rule that all bids have to be good for at least one second. That would cure a lot of problems. One lousy second! In a world of microseconds, that is an eternity.

Goldman Sachs went after an employee who stole some of their latest and greatest software this last week. The US assistant attorney general said in the courtroom that the software had the potential to manipulate the market. Imagine that. I am shocked. There is gambling going on in the back room? Gee, commissioner, I had no idea.

All this “algo” (algorithmic) trading also gives a very false impression of volume. If you are a fund and see 10 million shares a day traded, you might feel comfortable that you could hold one million shares and exit your trade easily. But if 80% of the volume is false “algo” trading, that volume isn’t really there. You may have a position that will be a problem if you want to exit, and not know it.

“High-frequency trading strategies have become a stealth tax on retail and institutional investors. While stock prices will probably go where they would have gone anyway, toxic trading takes money from real investors and gives it to the high frequency trader who has the best computer. The exchanges, ECNs and high frequency traders are slowly bleeding investors, causing their transaction costs to rise, and the investors don’t even know it.” (Themis Trading)

We are literally talking billions of dollars here. The SEC needs to step in and stop this, and soon. This is a lot more important than the salaries of investment professionals, for which the Obama administration today suggested new rules, which would allow the SEC to oversee salaries at member firms. Seriously? They don’t have enough to do already?

The link to the white paper is http://www.themistrading.com/article_files/0000/0348/Toxic_Equity_Trading_on_Wall_Street_12-17-08.pdf. Themis Trading is at http://www.themistrading.com/.

Read the paper. Then, if you like, drop the very nice folks at the SEC your thoughts at tradingandmarkets@sec.gov. And now, let’s start off with Japan.

The Land of the Setting Sun

One of the real benefits of writing this letter is that I get to see a lot of really interesting information from readers and meet with very savvy investment professionals. This week I had the privilege of sitting with a team of analysts from Hayman Capital here in Dallas. Hayman runs a global macro hedge fund, so they spend a lot of time thinking about how all the different aspects of the global markets fit together.

A one-hour meeting stretched to three hours, as the discussion was quite lively. I learned a lot more than I contributed (which is not unusual). After I made my presentation, they showed me a presentation they had been using. Some of the graphs were quite eye-opening. While I had seen some of the data in different places, there were a lot of new ideas, and having it all in one place was extremely helpful. There was a lot of work (as in months) done here; and Kyle Bass, the founder of the firm, graciously allowed me to share some of it with you (and kudos to Wes Swank, who pulled this together). The graphs are theirs, and my discussion about them is certainly informed by our meeting; but I am using the material as a launching point, so they are not responsible for my conclusions and interpretations.

Over the years, I have written about Japan often. Its economy is very important to the world, and its banks have funded and loaned a great deal to companies outside of Japan. Global growth would have been a lot slower without the Japanese. Up until recently, their population has saved a great deal of its disposable income, and those savings have allowed the Japanese government to run massive deficits.

And we are talking truly massive. Over the last ten years, the government has seen the level of debt-to-GDP rise from 99% to over 170%, not including local governments. They ran those deficits to try and pull themselves out of the doldrums of their Lost Decade of the ’90s, following the crash of their real estate and stock markets, starting in 1989. They built bridges and roads to nowhere, all sorts of programs, quantitative easing, etc. Sound familiar?

Of course, they were coming out of two really large bubbles, far larger than those recently in the US. I think I remember reading that at one point the land on which the Imperial Palace in Tokyo is built was valued at more than all of the real estate in California. Why not buy Pebble Beach or a few iconic buildings in New York, when they were so cheap? Today, Japanese real estate is still massively down (on the order of 50-80%, depending on location). And the Nikkei is still down roughly 75%, 20 years later. Do you think the Dow will be at 3,500 in 12 years?

As late as 1999, personal savings plus pensions were running at 12% and had been as high as 16%. And much of those savings went into government debt. The government kept borrowing, and rates stayed in the area of 1%. Today, a ten-year bond yields 1.3% in Japan, so they could run up a very large debt and the interest-rate cost was not a big factor in the budget.

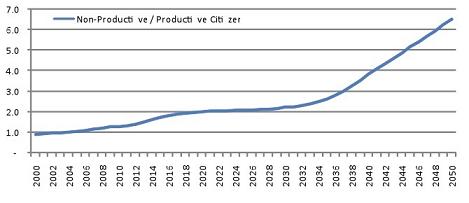

But now things are changing. Demography is starting to change the landscape. Japan is a rapidly aging nation. The population is shrinking, and the birth rate is among the lowest in the world. And the dependency ratio is starting to rise. There are currently 1.2 nonproductive citizens (under 15 years old and over 64) for every productive Japanese; the ratio will reach 2.0 by 2020 and will continue to grow thereafter. (See chart below.)

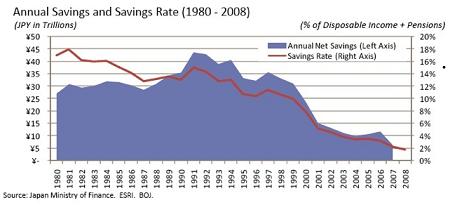

This also means that the ability to save is dropping, since so many retirees now need to dip into savings to live. Notice in the chart below that savings have dropped from 18% to 1.8%. Also notice that annual net savings is now down to 5 trillion yen.

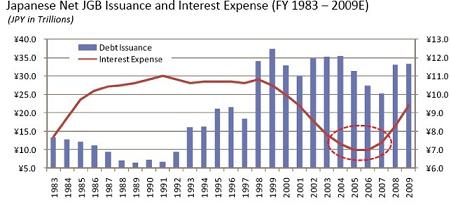

But this year, the Japanese will want to issue roughly 33 trillion yen in debt! Also note that the national pension fund has informed the government that this year they will for the first time be net sellers of debt. Look at the chart below. Notice that as debt was increasing through 2006, actual interest-rate expense for government debt was decreasing, because rates were dropping, getting to 0.1% in 2001. Yet with no more room to cut rates, interest-rate expenses have started to rise. Total government debt is now close to 900 trillion yen.

Interest-rate expense is now about 18% of the Japanese government budget. What if rates went to a lofty 2%? That would over time double the interest-rate expense. And the Japanese are borrowing between 30-40% of their annual budget. The total debt is rising rapidly.

Ok, let’s go over these points:

Japan’s population is shrinking, and the number of workers per retiree is rising. Japan has the highest ratio of debt to GDP in the developed world. And that debt is growing by 7-8% a year, and does not include local debt. Interest rates cannot go lower. Savings are falling rapidly and will not be able to cover the need for new debt issuance, by a long shot. Within a few years, because of the aging of the population, savings will go negative. Social security payments are rising. GDP is shrinking, and export trade is off about 30-40%, depending on the industry. Machine tools are down 80%!

If rates were to go up by 1%, let alone 2%, over time Japan’s percentage of tax revenue dedicated to interest payments would double to 18% and then to 40% and then just keep going up. It is conceivable that it will take 100% of tax revenues in less than ten years, at the current trajectory. Why? Because Japan is going to have to start to compete with the rest of the world to sell its bonds. Who but the Japanese would buy a Japanese bond at 1.3%? From a country that is rapidly going to 200% of debt-to-GDP? Doesn’t really seem like a smart trade to me. And as the data shows, the ability of the Japanese consumer to buy more debt is rapidly waning.

The Japanese government is coming to a crossroads with no good exits. Cut the budget drastically in the face of a deflationary recession? Monetize the debt and let the yen go the way of all fiat currencies? Can someone say Zimbabwe? Increase already high taxes in a very weak economy?

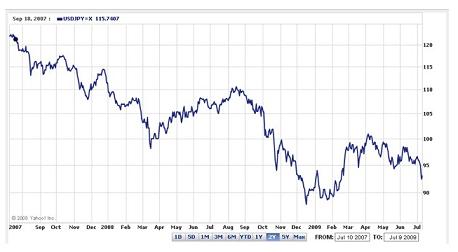

And yet the yen has been getting stronger over the last month. It is now at 92 to the dollar, up from 120 just two years ago. Why would a country with such bad fundamentals have such a strong currency? Shouldn’t the yen be a screaming short?

Let me offer two speculations that are mine alone. First, it is well-known that the Japanese are very involved in the reverse carry trade. That is, since they can’t find yield in Japan, they convert to another higher-yielding currency for income. So, maybe the retirees actually need to spend some of that money they have outside of Japan to live, so they have to convert to yen.

Second, Japanese corporations are getting hammered. Could it be that they are bringing yen home to pay for current transactions like rent and payroll? Japanese corporations dependent on exports desperately need the yen to fall, yet the central bank can’t seem to engineer a falling yen. I wrote about five years ago that the Japanese Central Bank has to rank as one of the most incompetent of all central banks, because they can’t even destroy their own currency.

But I think the central bank is going to figure it out. If they do not monetize the debt, rates will have to rise over time (say the next 2-3 years), and that is most definitely a problem. Monetizing the debt would mean the yen would fall in value, which is something they actually want to happen. How much monetization? When? I don’t know, and I doubt they do. If I were the head of the central bank or the government, I would not sleep easy.

Japan is the second largest economy in the world. There is a rule in economics: “If something can’t continue, then it won’t.” Japan can’t continue down this path. All the trends are going against them. Sadly, Japan is going to hit the wall, maybe some time in the next few years. This will be very bad for the world, as they have financed much of Asian growth. They do in fact buy a lot of world goods, and their buying power is going to fall. This is going to mean fewer US and European jobs. Not to mention fewer jobs in the countries that are Japan’s neighbors.

And unless we change things in the US, this will be us in less than ten years. As in hit the wall, serious depression, etc. I am hopeful that we can actually get our act together. But then I am an eternal optimist.

Buddy, Can You Spare $5 Trillion?

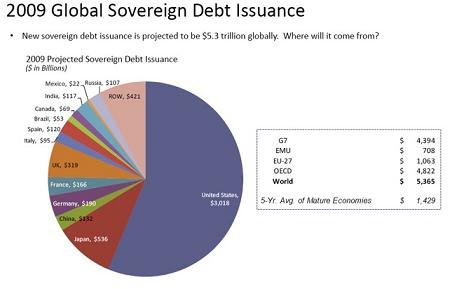

I have been writing for months that I don’t think the US can find $2 trillion dollars this year and then come back to the well for another $1.5 trillion next year without serious disruption in the markets. Where do you find that much money when all the rest of the world also wants to borrow massive amounts? How much are we talking about? The friendly folks at Hayman actually spent the time to add it all up. This is not a comforting graph.

The graph shows the US will need to issue $3 trillion in debt. “Wait,” I asked, “I thought it was only 1.85” The answer is that the number has grown to almost $2 trillion (as I wrote it would). Then you need to add in off-budget items like TARP, state and municipal debt, etc. Pretty soon it adds up to another trillion. All told, Hayman estimates that the world will need to find $5.3 trillion in NEW government financing. Never mind the needs of corporations or individuals or commercial mortgages, etc.

I am still trying to get my head around this. Let’s hopefully assume that they made a mistake and it is “only” $4 trillion. Where do you find that kind of money in a global deleveraging recession?

The World Bank says that total world GDP in 2008 was $60 trillion (http://siteresources.worldbank.org/DATASTATISTICS/Resources/GDP.pdf).

That means we need to find almost 9% of world GDP to fund the new government debt. Gentle reader, this is a serious problem. And now the next chart. Remove sharp objects or take another drink.

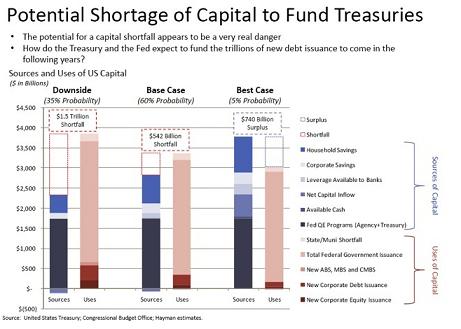

This one is titled “The Potential Shortage of Capital to Fund Treasuries.” They take into account the need for corporate borrowing, new corporate equity issuance, real estate debt, capital inflows and outflows, household savings, etc.

Bottom line? There is simply not enough available capital under current conditions to do it all. Something has to give. More household savings? More foreign investment (flight to safety, as the rest of the world looks even worse)? Reduced corporate borrowing and thus less GDP growth? Higher rates to attract more foreign and US investment?

The combinations are infinite, but none of them bode well. Increased household savings means less consumer spending. To attract more foreign investment (in the amounts that will be needed) will mean higher rates. And this is 2009. What happens in 2010? And 2011?

One trillion dollars is 7% of US GDP. And we will be running trillion-dollar deficits for a very long time.

Just a thought: Do you want to be a senator or congressman running for office next year with unemployment nearing 11% (my estimate), with all of the problems mentioned above, and with a record of having voted for the largest unfunded deficits in history? It is going to be a very interesting election cycle.

I will close here, as going into the next slides will make the letter way too long, but we will get to them next week. As a teaser, they asked me what my number-one concern was. I said Europe and European banking. Interestingly, that was also their number-one concern for “exogenous” risk. It will make a great launch for next week’s letter.

New York and Maine

My travel plans keep changing. Looks like I will not get to London and the Baltics this summer. So my next trip is a quick evening in New York with Art Cashin and Ron Insana for dinner, a few business meetings, and then off to Maine with my youngest son Trey for the Shadow Fed fishing weekend hosted by David Kotok at Grand Lake Streams. Talking with friends who are lucky enough to get an invite, we all say it is the highlight of our year. Just thinking about it gives me a smile. It looks like Steve Liesman of CNBC (who, by the way, is a very accomplished guitar player) will be doing a documentary of the weekend.

All in all, it is a pretty high-powered group, economics -wise, and I am looking forward to the debates, with several Fed economists and the likes of Paul McCulley, Martin Barnes, Barry Ritholtz, John Silvia (and congrats to him on his new post as chief economist for Wells Fargo), Chris Whalen, George Friedman of Stratfor, and too many others to mention. Way too much wine and great food, and the fishing is always good. It doesn’t get much better.

And then I come back and get ready for daughter Amanda’s wedding in Tulsa and Trey going back to school. And I turn 60 the first week of October. Oddly, my fall travel schedule is rather light, which is good, as I am so far behind on so many projects. But I do need to get to Europe and also go to Uruguay to meet with new Latin American partner Enrique Fynn (more on that in a few weeks). And two more grandkids will appear this year. Life is good and more interesting than ever.

Have a great weekend. I know mine will be fun.

Your still believing we will all get through this mess analyst,

John Mauldin

John@FrontLineThoughts.com

Copyright 2009 John Mauldin. All Rights Reserved

Note: The generic Accredited Investor E-letters are not an offering for any investment. It represents only the opinions of John Mauldin and Millennium Wave Investments. It is intended solely for accredited investors who have registered with Millennium Wave Investments and Altegris Investments at www.accreditedinvestor.ws or directly related websites and have been so registered for no less than 30 days. The Accredited Investor E-Letter is provided on a confidential basis, and subscribers to the Accredited Investor E-Letter are not to send this letter to anyone other than their professional investment counselors. Investors should discuss any investment with their personal investment counsel. John Mauldin is the President of Millennium Wave Advisors, LLC (MWA), which is an investment advisory firm registered with multiple states. John Mauldin is a registered representative of Millennium Wave Securities, LLC, (MWS), an FINRA registered broker-dealer. MWS is also a Commodity Pool Operator (CPO) and a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB). Millennium Wave Investments is a dba of MWA LLC and MWS LLC. Millennium Wave Investments cooperates in the consulting on and marketing of private investment offerings with other independent firms such as Altegris Investments; Absolute Return Partners, LLP; and Plexus Asset Management. Funds recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MWS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor’s services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauldin receive fees from the funds they recommend/market, they only recommend/market products with which they have been able to negotiate fee arrangements.

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore