Slowing Asian growth appears to be putting downward pressure on interest rates even as stronger U.S. growth is pushing rates higher.

To explain… earlier this month Goldman Sachs research reiterated its view that the current semiconductor equipment cycle- expected to run will into 2011- would be the biggest ever. Given that semiconductor stock prices tend to peak at or close to the highs for semi equipment orders… they maintain a positive view on the tech sector. Fair enough.

Below is a chart comparison between 10-year U.S. Treasury yields and the ratio between the Philadelphia Semiconductor Index (SOX) and the S&P 500 Index (SPX).

The argument is that the SOX/SPX ratio goes with yields yet it just made a new recovery high yesterday. The relative strength exhibited by the chip stocks suggests that U.S. capital spending is strong enough to move interest rates higher even as they decline based on slowing Asian growth and the Eurozone crisis. Typically, by the way, divergences of this nature tend to accelerate or accentuate a strong cyclical theme.

Below is a chart comparison between the U.S. Dollar Index (DXY) futures and the ratios between the S&P 500 Index and two individual stocks- Intel (INTC) and copper producer FreePort McMoRan (FCX).

This is probably an upside down way of making a point but the idea is that when the dollar trends lower- as was the case into November of last year- the focus of cyclical strength will tend to be in the basic materials sector. In other words the SPX/FCX ratio will tend to decline as FreePort strengthens relative to the broad market.

When the dollar turns higher, however, the game changes. Instead of the basic materials stocks outperforming the tendency is for the tech sectors to do better which causes an upward tilt in the SPX/FCX ratio and a downward slope for the SPX/INTC ratio.

Our point? The markets are worried about a consumer spending slow down during the second half of the year but, to a certain extent, that misses the point. It is not U.S. consumer spending that is going to power the recovery but instead U.S. capital spending. If Goldman Sachs is correct in its view that this will be the biggest semi equipment cycle ever… then it makes sense to hold a bullish equity markets view with a strong lean towards ‘tech’.

Equity/Bond Markets

We are going to return to the two charts of 10-year U.S. Treasury yields that we included in yesterday’s issue. Below we show 10-year yields from 1998 into 2001 and from 2008 to the present day.

The argument is that the recent decline from around 4% to 3.1% for 10-year yields is one of two things. It is either a crisis-related decline similar to the lows set in 1998 and again at the end of 2008 or it is a harbinger of a growth slow down similar to the first quarter of 2000.

The charts have been set up to make a fairly specific point. If history were to repeat 10-year yields will make a bottom this quarter (hopefully one has already been put in) and then hold that bottom for some time. As long as the lows around 3.1% are not broken then there is at least a chance that economic growth is not slowing.

In the final quarter of 2000 yields moved down through the lows set in April and that was the market’s way of ‘saying’ that the theme (capital spending, tech, large cap, U.S. dollar) that had powered the Nasdaq and S&P 500 Index to new all time highs into the spring of 2000 was now turning negative.

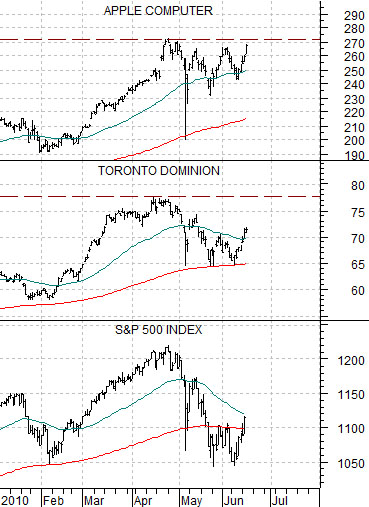

In any event… we can think of a number of very good explanations for why the S&P 500 Index went into the tank last month and none of them relate to the end of the world or Europe heading into an economic abyss. Our thought is that a return to a stronger trend will require the leaders to lead with enough momentum to swing the laggards upwards. A monster stock like Apple, for example, would help the trend considerably by breaking above the April highs while Canadian banks (which have been leading the recovery in the financial sector) would look better if Toronto Dominion (TD) managed to push to new all time highs above U.S.$78.