We thought that we would start off today by going back over a topic that we have covered in these pages on more than a few occasions. Sort of a ‘how did we get here’ idea.

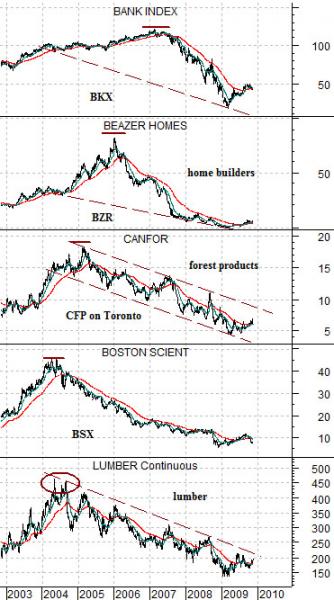

Below is a chart comparison anchored at the bottom by lumber futures. From lumber we move to the chart of Boston Scientific (BSX), Canadian forest products company Canfor (CFP), U.S. home builder Beazer (BZR), and the Bank Index (BKX).

The tale starts back in 2000 following the peak for the Nasdaq. As capital spending began to falter long-term U.S. interest rates began to decline. By January of 2001 the Fed- late to the party as always- began to cut short-term interest rates in an effort to offset the collapse of cyclical growth.

As interest rates declined lumber futures moved higher representing the leading edge of the positive real estate cycle. During periods of weaker cyclical growth the markets tend to turn to non-cyclical stories sending BSX upwards. As one might expect the forest products stocks had a good run along with the home builders. The banks discovered the joys of packaging, distributing, and leveraging mortgage-related securities and a good time was had by all.

In the spring of 2004 energy prices- specifically heating oil futures- broke to new all time highs. This created a significant change in trend as interest rates once again began to rise. The swing from falling to rising yields marked the peak for lumber futures so in 2004 lumber prices began to decline. By 2005 the forest products stocks had entered a bear market and by the end of that year the home builders had reached a bull market top. The banks pushed higher into 2007 but, as the chart comparison attests, all roads led back to 2004. The beginning of the end for the housing bubble dated back to 2004 when energy prices in particular and commodity prices in general gathered enough upward momentum to turn interest rates higher.

Our point? We really do not want to see a continuation of commodity price strength. We really do not want to see energy prices coming anywhere near last year’s cycle highs? Why? Because the sectors that led to the down side and ultimately cratered the entire financial system have yet to turn higher. Ideally it will be a year or two before the Federal Reserve sees fit to start aggressively tightening monetary policy once again.

Equity/Bond Markets

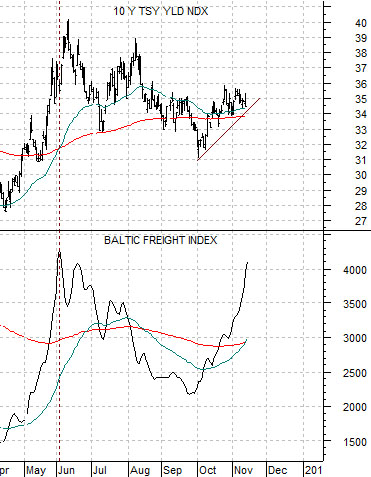

Below we compare 10-year U.S. Treasury yields (TNX) and the Baltic Freight (Dry) Index.

One of the problems facing the markets at present is upward pressure on interest rates and one of chief culprits is ocean freight rates. We may argue that the U.S. is more likely to tip into deflation than swing towards hyper-inflation but for the moment cyclical strength- predominantly in China- is causing upward pressure on yields. Typically the Baltic Dry Index leads 10-year yields at the turns by a week or two so our expectation is that we will not see a test of the lows near 3.1% until some time after parabolic recovery trend for dry bulk cargo freight rates turns lower.

Below we compare 10-year Treasury yields with the ratio between the share price of Coca Cola (KO) and copper futures.

Our expectation this year was for a peak in 10-year yields around the end of the second quarter. So far that has proven to be correct although the markets continue to trade as if yields are still on the rise. The Coke/copper ratio should have bottomed at the highs for yields suggesting that at best a lower trend for yields may have begun in early August.

So… on the one hand 10-year yields reached an absolute high in June at the first peak for ocean freight rates. On the other hand a case can be made that the actual top was reached in August at the low point for the Coke/copper ratio. The chart below right shows 10-year yields and the ratio between crude oil futures and gold futures. The ratio is range bound suggesting that the trend for yields is neither higher nor lower. Instead the trend is simply ‘flat’. If the ratio breaks above the August highs then yields are back in a rising trend but if the ratio takes out the July lows then we would expect to see 10-year yields resolving back down towards the 2.0% to 2.5% range.