For a change- perhaps a welcome one- we are going to do our best to start off with a very simple and straightforward argument.

From the perspective of those long the equity markets in general and the U.S. equity markets in particular the best case would be a continuation of the strong trend that began in March of last year. On the other hand the worst case would be that the entire rally turns out to be nothing more than a bear market bounce.

Feb. 19 (Bloomberg) — Stocks are poised to tumble as gauges of the economic outlook in the U.S. and China have peaked, according to Societe Generale SA’s Albert Edwards… He says stocks are “overpriced” and headed for a long-term drop he terms “the ice age.”

We have lived through our fair share of markets cycles and know full well how emotions can come into play. One day you read that the markets are going to collapse and the next day prices rally creating the impression that new highs are just around the corner. If you jump in and out each time the S&P 500 Index moves a couple of percentage points in either direction… there is a reasonable chance that you will end up both frustrated and poorer.

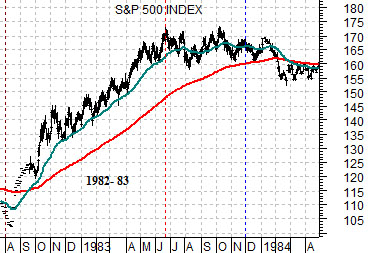

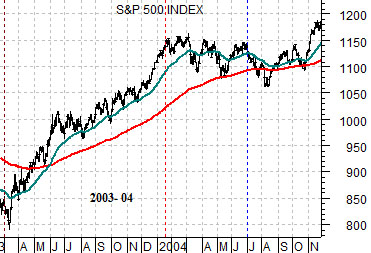

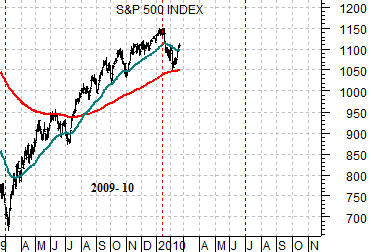

Below are three charts of the S&P 500 Index (SPX). The top chart shows the time period following the bear market bottom in August of 1982. The middle chart features the time frame after the start of the new bull market in March of 2003. The lower chart lines up the lows set in March of 2009 with the two previous bottoms.

So… what is our simple and straightforward point? If the stock market truly turned higher in March of 2009 then the comparisons shown suggest that absolutely nothing that is happening today should be that surprising. We wrote a month or two back that the SPX would likely lose momentum as we moved into February. After about 10 months of accelerating higher with corrections holding at the 50-day moving average line the S&P 500 Index has now moved into a time period similar to the second half of 1983 and the first half of 2004. At this juncture- assuming, of course, that we are truly not heading into an investment ‘ice age’- corrections would be expected to find support around the 200-day exponential moving average line (red line on chart) with rallies finding resistance in the vicinity of the January peak around 1150. The comparison argues that a choppy but generally flat trend through the end of the second quarter would fit nicely with previous cycles.

Equity/Bond Markets

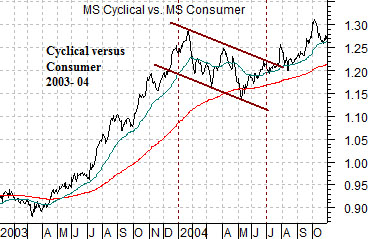

Below we have included two charts based on the ratio between the Morgan Stanley Cyclical Index (Alcoa, Ford, Deere, Caterpillar, Hewlett Packard, etc.) and the Morgan Stanley Consumer Index (Abbott Labs, Carnival, Colgate, Coke, Johnson and Johnson, Merck, etc.). The top chart shows the time frame from the start of 2003 into October of 2004 while the lower chart begins at the start of 2009.

Above, our argument was, essentially, that as long as the equity markets are not collapsing down below the 200-day moving average lines then this looks very much like the start of past bull markets. In other words… more of a fledgling ‘bull’ than a somnambulant ‘bear’.

The chart at top right shows that after a period of rather marked relative strength for the cyclical sectors through the final nine months of 2003 the markets spent the first half of 2004 favoring the consumer stocks. If history were to repeat… within the context of a generally flat trend for the S&P 500 Index the first half of this year would favor the stable growth or defensive sectors.

Below we feature a comparison between copper futures and the price spread between the 30-year T-Bond futures and the 10-year T-Note futures.

This is a rather complicated picture even though the argument that it makes is fairly simple. We hope.

To explain… the price spread between the 30-year and 10-year Treasury futures moves ‘with’ bond prices. The spread rises when bond prices are rising and declines when bond prices are trending lower. We use it at times to get a sense of what the overall trend is for the bond market and it comes in handy when absolute prices are behaving somewhat erratically.

From an intermarket perspective rising copper prices go with falling bond prices. In other words as long as copper prices are pushing higher there will be continued upward pressure on yields. Fair enough.

So… let’s try to follow the bouncing ball. Notice that the price spread between the 30-year and 10-year Treasury futures declined back to around -1 last week. A level of -1 (the TBonds priced around 1 point below the price of the 10-years) marked the lows for the spread at the start of this year when copper prices pushed up to around 3.50 and the high point for yields back in June of 2009. A spread of close to -1 was reached in early March of 2008 when copper prices made their first run at 4.00.

The point is that over the past few years a price spread of -1 has been associated with some kind of peak for copper prices. While the 2008 example shows that copper futures can make repeated forays back to the highs the argument is that for our argument to work… copper prices have to hold at or below 3.50.

If copper prices do not make new highs then two things happen. First, the pressure on the bond market eases somewhat. Second, the perceived attractiveness of the base metals and commodity cyclicals fades which then supports our contention that in a fairly calm and reasoned manner the equity markets swing back to favoring the consumer and health care sectors through the first half of this year.