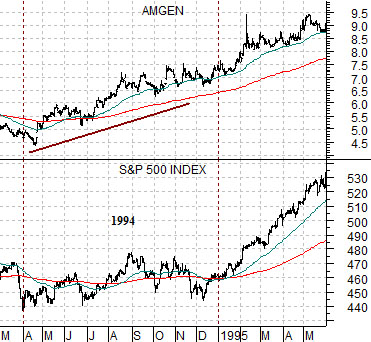

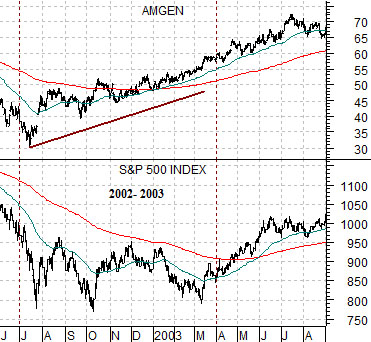

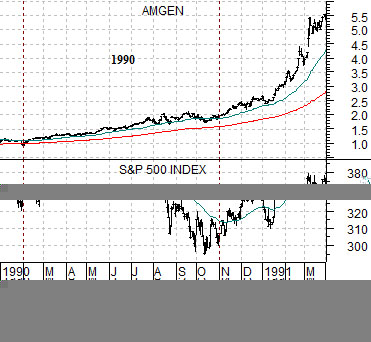

We are going to return to an argument that we have not shown in these pages for at least a couple of quarters. The idea is based on the stock price action of biotech giant Amgen during equity markets corrections.

At right we feature a chart of Amgen (AMGN) along with the S&P 500 Index (SPX) from 1990- 91. Below right we show the same comparison through the 1994- 95 time frame while directly below we have included the view from 2002- 2003.

The argument was that AMGN has tended to turn higher around nine months before the broad stock market pivoted back to the upside. The stock price of AMGN began to swing upwards in February of 1990 nine months before the stock market turned positive in November, in April of 1994 close to nine months ahead of the end of year upswing that carried through 1995, and again in July of 2002 close to three quarters ahead of the stocks market’s return to a rising trend in the spring of 2003.

If AMGN tends to lead the stock market’s recovery then what does this say about the current situation? We will show the muddled picture on the following page.

Equity/Bond Markets

Given that we have argued in the past that AMGN tends to lead the stock market to the upside by close to nine months… one would think that it would be reasonably easy to forecast a rising equity markets trend. After all… one only has to see exactly where AMGN has turned back to the upside and add another nine months.

The situation would be fairly straight forwards if AMGN had simply swung back to the upside but the chart at right shows that it has made two separate bottoms over the past year or so.

If we mark the start of a rising trend for AMGN as July of 2008 then the process would select a March 2009 bottom for the SPX. With the benefit of hind sight we can see that this is exactly when the stock market turned positive. However, as mind-bending as this may appear the problem is that AMGN followed the steep price rise into the autumn of last year with a second bout of weakness into the first quarter of 2009.

The point is that if we use this one comparison as a means of timing the stock market it would have argued that a low was due in March of this year (which was exactly what we were calling for at the time) while also suggesting the possibility for a second bottom into the fourth quarter.

The equity markets are pushing nicely higher at present and we do not want to spend too much time arguing with such a strong trend so the point that we are attempting to make today is that a case can be made for lower equity prices into the end of this year. The good news would be that this would give us a second chance at the kind of recovery trend that the markets have exhibited over the past five months.

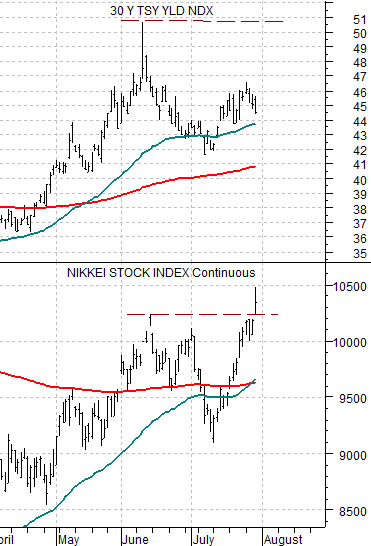

Our thought is that the beginning and end of any argument that includes lower equity markets prices is based on the action in the bond market. The stock market has been rising on the kind of cyclical strength that goes with higher long-term interest rates and lower long-term bond prices so if we can make a case for falling yields… we can also make a case for weaker asset prices.

At right we show the yield index for 30-year U.S. Treasuries and Japan’s Nikkei 225 Index futures.

July 31 (Bloomberg) — Japan’s unemployment rate rose to a six-year high in June, undermining the outlook for consumer spending just as exports start to improve.

The jobless rate advanced to 5.4 percent from 5.2 percent in May, the statistics bureau said today in Tokyo, higher than the 5.3 percent median forecast of economists surveyed. Consumer prices excluding fresh food, the central bank’s preferred gauge, fell a record 1.7 percent in June, a separate report showed.

rom March into July global stock markets have been pushing upwards along with long-term yields. The problem as we approach the end of the month is that stock prices are still pushing higher- the Nikkei futures broke to new highs during trading yesterday- but yields are not following. The arguments that we have been making on pages 3 and 5 (which we will run through once again today) this week have been that the equity markets have started to diverge from the bond market in rather disconcerting fashion of late.