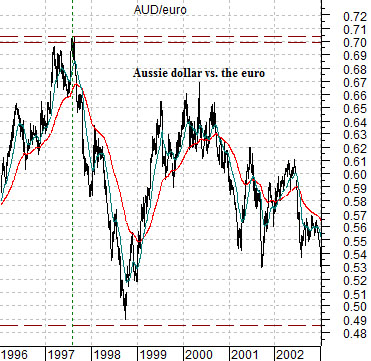

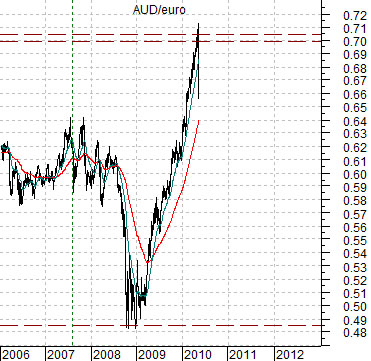

After a week away from the markets we are going to start off today using a rather bizarre perspective. We have actually set up and removed a number of chart-based arguments as we searched for something that might help to explain the current situation. Eventually we decided to show the cross rate between the Australian dollar (AUD) and euro within the context of one our recurring arguments- the Decade Theme.

The Decade Theme is based on the idea that during each of the past several decades the trends have been broadly similar. Asset price peaks in ‘0’ years (1980, 1990, 2000), cyclical bottoms into the ‘2’ years, recoveries through the ‘3’ years, corrections in the ‘4’ years, crashes and crisis in the ‘7’ and ‘8’ years, leading into asset price recoveries through the ‘9’ years.

From this perspective the subprime crisis in late 2008 was similar to 1998’s Asian crisis with the rally during 2009 in some ways similar to the Nasdaq’s drive to a bubble peak during 1999.

The problem is that even as the decades repeat they do so in different ways. Commodity prices peaked in 1980, the Japanese and Taiwan stock markets into 1990, the Nasdaq and large cap U.S. stocks into 2000, and an asset class yet to be determined into 2010.

At first blush the prospect of an asset price peak in 2010 leading into a correction through 2012 would seem somewhat ominous but when we consider that the two most obvious sectors for bubble-dom are gold and the commodity-related currencies… a bullish outcome may, in fact, be possible.

The Aussie dollar reached a peak against the euro in 1997, crashed into late 1998, and then rebounded into the middle of 2000. In the current cycle the cross rate topped out in 2007, collapsed into the end of 2008, and then surged to a second top into 2010.

The trends are similar even though the position of the cycle peaks are different. The previous decade focused on U.S. growth and tech so the AUD/euro reached an extreme in 1997 while the current situation was more Asian growth and commodities which created a cycle peak into 2010. Our view is that the AUD/euro should spend the next two years resolving lower as money rolls out of the commodity theme, commodity currencies, and gold and back towards the dollar and euro.

Equity/Bond Markets

The Asian crisis in 1998 marked the end of a trend that began in early 1997. As Asian growth improved in 1999 the markets sent the Nasdaq screaming into a bubble peak.

The key is that the markets that went into crisis (Asia, Brazil, Russia, etc.) were not the same markets (large cap U.S.) that led the collapse two years later in 2000.

The banks peaked in 2007 and went into crisis late in 2008. As the banks recovered one or more markets were pushed into price bubbles. The idea is that it shouldn’t be the banks that lead the decline into 2012 but instead should be those sectors that benefited the most from the actual crisis. Try as we might we can’t get away from the idea that the most likely culprit for a price peak this year will be gold.

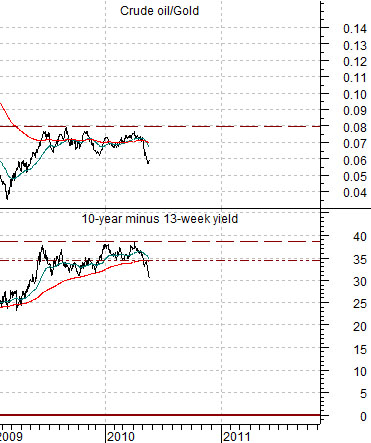

Below we show the ratio between crude oil and gold along with the spread between 10-year and 3-month Treasury yields.

In 2000 the yield curve was inverted with crude oil at a peak relative to gold. The situation this year is almost exactly the opposite of 2000. The chart below right shows that the yield curve is at a peak while the crude oil/gold ratio is well below .08. In other words… one would expect to find oil prices at a bottom relative to gold with the yield spread at the highs similar to early 2002 which is another way of writing that if the yield curve was inverted- as it was in 2000- we could justify strong gold and weak crude oil but with the yield curve at an upper extreme the markets should be pulling gold prices down relative to energy prices.

Quick change of direction. The equity markets bottomed in October of 1990. Just over a year later in November of 1991 the stock price of Carnival (CCL) snapped back to its 200-day e.m.a. line before settling out and pushing to new highs. Below we show CCL in 1991 as well as the current situation (just over one year from the March 2009 lows). The point? This still looks more like a knee-buckling correction than an actual end to the broad recovery.