Dec. 19 (Bloomberg) — The dollar touched a three-month high against the currencies of major U.S. trading partners as the Federal Reserve said the economy improved while reiterating it will keep borrowing costs low for an “extended period.”

The U.S. dollar ended the week stronger so we thought that this might be an opportune time to review what a ‘strong dollar’ can or should mean with regard to a few of the other markets.

Below is a comparison between the sum of copper futures (in cents) and crude oil futures (in dollars times three) and the sum of the U.S. 30-year T-Bond futures and U.S. Dollar Index (DXY) futures.

The basic point is that copper and crude oil prices trend in the opposite direction of the long end of the Treasury market and the dollar. We will bank this perspective for a moment and move on to the chart below right.

The next chart compares gold futures with the spread or difference between the TBond futures and the U.S. Dollar Index. The chart argues that gold prices tend to rise when the TBond is strong relative to the dollar.

The argument would be that when the dollar swings higher it puts downward pressure on commodity prices. If the dollar AND the bond market move upwards together then the sum of the two will be stronger which tends to go with weaker base metals and energy prices. A rising dollar is a negative for commodity prices in general while a strong bond market usually represents the kind of economic or cyclical weakness that goes with a negative trend for base metals and energy prices.

If, on the other hand, the dollar moves higher and the bond market declines then the spread between the TBond and DXY will fall. In other words this outcome could result in a fairly flat ‘sum’ which helps to support energy and base metals prices even as the ‘spread or difference’ is forced lower putting downward pressure on gold prices.

The point is that while a rising dollar will tend to be a negative for commodity prices the key to exactly where the pressures show up lies with the bond market. If bond prices rise then look for lower energy and base metals prices but if bond prices decline then much of the burden will fall on the precious metals.

Equity/Bond Markets

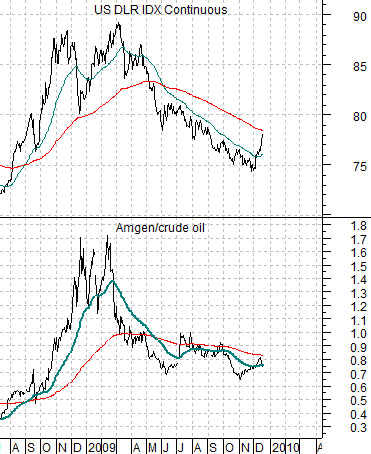

Below is a comparison between the U.S. Dollar Index (DXY) futures and the ratio between biotech giant Amgen (AMGN) and crude oil futures.

The AMGN/crude oil ratio tends to trend with the dollar. When the dollar is stronger AMGN- representing the biotech sector- will tend to rise relative to crude oil future prices.

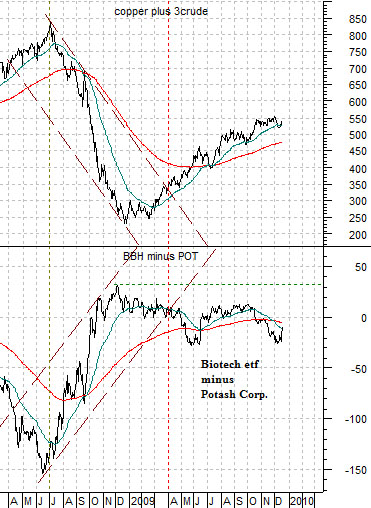

Below is a comparison between the sum of copper and crude oil futures (which, we showed on page 1, tends to trend inversely to the dollar and bond market) and the spread or difference between the share price of the Biotech etf (BBH) and fertilizer producer Potash Corp. (POT).

We have adjusted the BBH for the recent takeover of Genentech by Roche. The adjustment may not be perfect but we believe that it is close enough for today’s purposes.

Any outcome that leads to either a flat or negative trend for base metals and energy prices should go with a flat or positive trend for the biotechs relative to the ‘ag’ stocks. In other words one way to know that the markets are shifting trends- away from the weak dollar/strong commodity theme- is through relative strength in the biotech sector. The better the BBH does in relation to names such as Potash and Agrium the greater our conviction that the dollar’s strength is ‘real’.

Below is yet another relationship based on the share price of Amgen. The chart compares AMGN with the ratio between aluminum producer Alcoa (AA) and gold miner Newmont (NEM).

In essence the markets have been under pressure since early July. We have noted on a few occasions in the past that a positive stock market trend tends to go with a rising AA/NEM ratio. In other words if money is flowing towards gold and away from the economically sensitive aluminum producers the underlying trend is usually somewhat bearish. From the start of the current month through the end of last week the markets have begun the process of returning to more positive themes lending a positive bias to the equity markets.