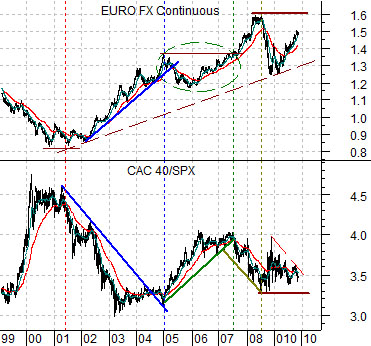

Below is a somewhat messy chart of the euro futures and the ratio between France’s CAC 40 Indice and the S&P 500 Index.

The premise is quite simple- when the euro is strong and rising the CAC 40/SPX ratio declines. Conversely when the euro is flat to lower the French stock market outperforms the U.S. stock market.

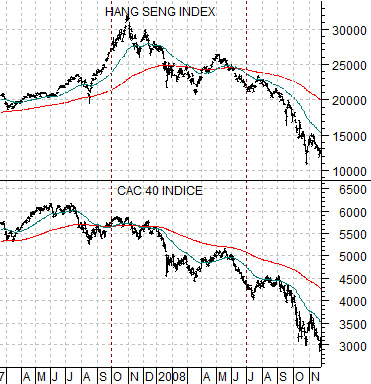

At bottom we show the Hang Seng Index and the CAC 40 Indice from 2007- 2008. The argument is that the CAC 40 was one of the first markets to buckle as it turned lower a quarter of so ahead of the Hong Kong stock market and a full year before the commodity markets reached a peak in the summer of 2008.

Our thought is that if stock and commodity prices keep rising on the weak dollar and stronger euro then the CAC 40 may once again lead to the down side. The problem with being negative on the equity markets today is that- as the chart comparison below attests- the French stock market has yet show much in the way of weakness. We would expect to see this index breaking below its 200-day moving average line (i.e. 3500) to signal the start of the leading edge of downward cyclical pressure.

Equity/Bond Markets

Below is a comparison between 10-year U.S. Treasury yields and the Baltic Freight (Dry) Index.

Nov. 11 (Bloomberg) — The dollar traded near a two-week low versus the euro before Chinese economic reports today that may support demand for higher-yielding assets.

The rising trend for ocean freight rates denotes or anticipates stronger growth in China. Stronger growth in China puts downward pressure on the dollar and bond market.

Below is a comparison between the ratio of copper futures to the CRB Index and the U.S. 10-year T-Note futures. The point is that the trend for bonds is ‘down’ even as copper prices- which tend to reflect Asian economic growth- rise relative to the CRB Index.

Below we show 10-year U.S. Treasury yields and the ratio between copper and gold futures prices. In general rising yields go with strong copper prices but over the past few weeks the strength in gold has pulled the ratio lower.

Our points are as follows: the trend for bond prices is ‘down’ as yields rise. The potential for the trend to reverse is quite high given the proximity of copper/CRB ratio to support. The trend is being stressed somewhat by copper’s inability- so far- to trade above the 3.00 level. At current gold prices copper should be closer to 3.30 if yields continue to rise. Either that or gold prices are better near 900 if copper continues to hold at or below 3.00.