Gold prices weakened in trading yesterday but found support once again at the rising 150-day exponential moving average line. We have included two charts for this on page 4.

With gold bouncing up off of support it is certainly not a given that the decline will continue. This is, after all, a support level that has held for years with each test resolving into a price acceleration to new highs.

For the sake of argument, however, let’s assume that ‘this time is different’. Let’s assume that this time gold prices fail to hold at the 150-day e.m.a. and in due course break to the down side.

In terms of the intermarkets the trend for gold is almost identical to the trend for the ratio between the price of the U.S. 30-year T-Bond futures divided by the U.S. Dollar Index (DXY) futures. Gold tends to rise with a stronger bond market as well as a weaker dollar.

To bust the bullish trend for gold we would need either a very weak bond market (rising long-term interest rates) or a very strong dollar. Most likely we would need both but let’s look at a potential path for the dollar that would help to apply some kind of downward pressure on the price of gold.

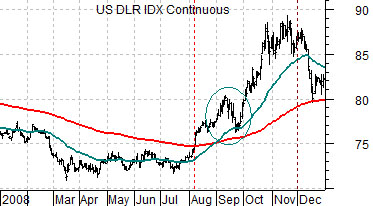

To get from ‘here’ (gold in a rising trend above its moving average line) to ‘there’ (bearish trend) a rising dollar would be required so we have included two charts of the U.S. Dollar Index futures at bottom .

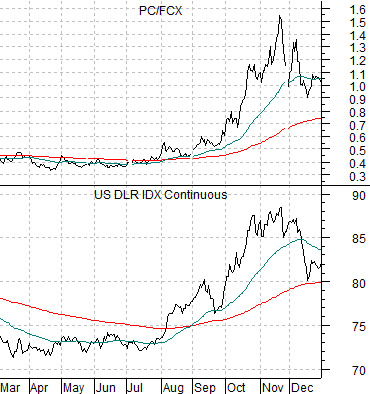

The top chart is from 2008. The lower chart is from 2011. We have lined up the charts up based on the point in time when the DXY rose up through its 200-day e.m.a. In 2008 this event happened in early August while in 2011 it took place in early September. This means that the 2008 chart runs from January through December while the 2011 chart starts a month later in February.

In 2008 the dollar broke up through its 200-day e.m.a. in August and then pulled back to its rising 50-day e.m.a. in September. From there the trend accelerated to the upside. In 2011 the dollar moved above its 200-day e.m.a. line in September and recent declined back to its rising 50-day e.m.a. line. The point is that if the current trend follows that of 2008 we could see an upward surge for the dollar into year end that would go quite some ways- especially if it occurred at the same time as weaker bond prices- to pulling gold prices appreciably lower.

Equity/Bond Markets

We will cover the two charts below first today.

The above argument was a lower gold price would require the dollar to follow a similar path to the second half of 2008. If we were to get a support break for gold and an upswing for the dollar… how would this impact the equity markets

In recent years the broad U.S. stock market (and virtually all other equity markets) has tended to be weaker on dollar strength. Our argument is that a stronger dollar does not necessarily mean that stock prices are going to tumble but will definitely lead to a shift within the markets.

The charts below compare the U.S. Dollar Index futures with the ratio between consumer cyclical Panasonic (PC) and commodity cyclical FreePort McMoRan (FCX). The chart below right is from 2008 while the chart directly below is from 2011.

If the dollar were to extend to the upside the PC/FCX ratio should rise. Panasonic should do better than FreePort. Whether this results in a tumbling or rising stock market rests in large part on whether the ratio rises on PC strength or on FCX weakness. We thought it interesting (and bullishly hopeful) yesterday that FCX actually closed higher in response to a 5% decline in copper prices.

At right we return to the chart comparison that we featured on the first page of yesterday’s issue.

The argument is that lower Japanese bond prices would be a positive. A weaker ratio between gold and the CRB Index would be a positive. A rising equity/bond ratio would be a positive. A close up through 40 by the Bank Index would also be a positive. While we might suggest that the markets have passed the point of maximum stress- for now- the reality is that a better trend has yet to truly begin.