We have commented on occasion that almost all relationships that point to a bubble for asset prices have gold as the numerator. In other words… gold prices relative to most other asset classes are ‘high’.

Below we show a comparison between the ratio of gold prices to crude oil futures prices and the U.S. 30-year T-Bond futures.

The argument here is that the long end of the U.S. Treasury market swings with the ratio between gold and oil prices. When bond prices are resolving higher the gold/crude oil ratio will tend to rise and when bond prices are trending lower as interest rates rise the ratio will tend to decline. Fair enough.

In a sense the chart speaks to the ongoing debate regarding an inflationary or deflationary outcome. Many believe that stronger gold prices suggest rising inflation which- intuitively- should lead to tumbling bond prices. The chart suggests that the opposite is true. The chart suggests that ‘relative strength’ for gold prices reflects a trend towards falling long-term interest rates and rising bond prices. Put another way… in a weak economy with a substantial output gap and little in the way of the kind of rising price pressures that would lead to near-term inflation… gold prices have been behaving in an entirely rational manner. The problem isn’t gold prices per se but rather crude oil prices.

Our point is that with bond prices resolving slowly higher since mid-year one would expect to see the gold/crude oil ratio tilted upwards- which has been the case. To the extent that crude oil prices are not weak then gold prices necessarily must remain strong. Once again… fair enough.

Below is a shorter-term view of the same chart relationship. Our focus is on the divergence that has been created this month as the gold/crude oil ratio tracks higher even as bond prices have returned to the channel bottom marking the trend that developed since June.

Our thought is that if the TBonds hold the 118 level then chances are that bonds look higher once the FOMC meeting concludes tomorrow with a return to the 124- 125 level likely. If the TBond futures happen to close much below 118 then by extension the gold/crude oil ratio should decline with support around 13:1. If crude oil futures hold near 70 then a ratio back to 13:1 argues for gold prices in the low 900’s.

Equity/Bond Markets

Below is a comparison between the share price of Boston Scientific (BSX) and the product of crude oil futures multiplied by natural gas futures.

We are using ‘oil times gas’ to represent energy prices in general. We are using BSX to represent the kind of stock that has done well in the past when energy prices remain somewhat weaker.

The ‘oil times gas’ combination peaked at the end of 2000 and, with the exception of a brief gas-inspired flurry in early 2003, held below the highs through into 2004. In a sense the period of time when energy prices were not making new highs between late 2000 and 2004 could well represent the ‘output gap’. When the slack created by the collapse of the tech and telecom bubble was taken up energy prices moved to new highs which, in turn, pushed interest rates higher. As long as there was economic ‘slack’ there was no upward pressure on interest rates and within this time frame the share price of BSX was able to rise.

Let’s try that again. Following the peak for energy prices at the end of 2000 and right up until the time that energy prices made new highs in 2004… BSX’s share price rose.

Below we show BSX and the produce of crude oil times natural gas futures for the current time period. We pointed out in yesterday’s issue that once energy prices stopped rising in October a recovery of sorts began to form for BSX.

The bigger question has to be whether the cycle will repeat ‘exactly’. While BSX was a clear beneficiary of the output gap between 2001 and 2004 it could be- probably will be- that some other sector or theme will flourish over the next few years.

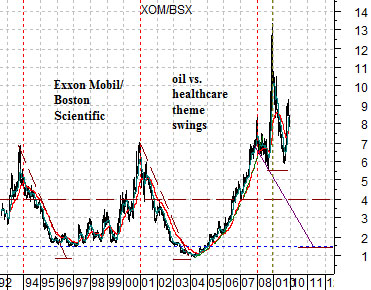

However… each time we consider the chart below of the ratio between Exxon Mobil (XOM) and BSX we find reason to believe that lightening may, in fact, strike in the same place twice. The chart shows that over time the XOM/BSX ratio has made long and very pronounced swings as money has moved from energy to health care and back again. Our recurring thought has been that if history were to be kind enough to repeat then the next trough for ratio- signifying a relative strength peak for BSX- would be set to occur some time around 2011 and 2012. No matter how many unconventional gas producers Exxon decides to buy along the way a ratio anywhere close to 2:1 will likely have to include some share price strength for BSX.