One of our recurring themes over the past while has been that in between the peak of a commodity cycle and the start of what we believe will be a consumer-oriented cyclical trend (i.e. autos instead of steel, Japan in place of Brazil) there should be a fairly lengthy stretch of time when U.S. large cap consumer defensive names outperform the broad U.S. market. In other words after the peak for Rio Tinto, Potash, and FreePort McMoran and before the start of the kind of price strength that will drive us into the next asset price bubble there should be a period when long-term interest rates resolve to their ultimate bottom while stable consumer growth names return to favor.

One can argue with our thesis on any number of points but the one that tends to give us pause has to do with the nature of ‘large cap consumer growth’. Our view is that the markets will replay the first half of the 1980’s and our assumption is that the relative strength leaders through that time period should do well over the next few years but the caveat is that we are associating ‘large cap consumer growth’ with U.S. and European companies when, as we all know, all of the growth is occurring in China, India, Russia, and Brazil. Wouldn’t it make sense to argue in favor of Chinese or Indian consumer products and health care names? Perhaps. Which is why we are mentioning it here today.

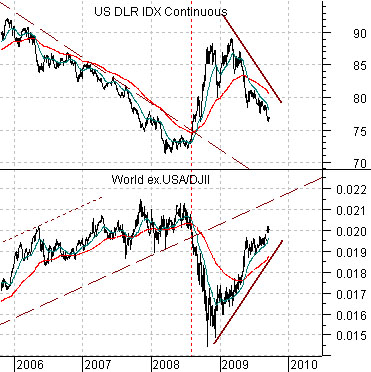

Aside from that the charts below describe the Big Picture view that we are working with. The chart at top right compares the U.S. Dollar Index futures with the ratio between the Morgan Stanley World ex-USA Index and the Dow Jones Industrial Index. In a sense we are suggesting that when the dollar is falling ‘everything but U.S. large cap’ does better than U.S. large cap and when the dollar is stronger U.S. large cap tends to do better than virtually everything else. Fair enough.

Below is comparison between the cross rate of the Japanese yen to the euro and the ratio between the S&P 500 Index (SPX) and the NYSE Composite Index. The SPX/NYSE Comp. ratio is supposed to represent ‘large cap relative to small cap’ and quite clearly when the yen is stronger than the euro- which tends to go with a better U.S. dollar (we show this on page 3 today)- large cap does better.

The point? If, as, or when the dollar rises the appropriate themes to be long are U.S. large cap versus virtually all of the emerging, developing, or commodity sensitive markets and U.S. large cap compared to U.S. small cap. For good or for bad… these are the pictures that we are using the support our thesis.

Equity/Bond Markets

We have been showing the ratio of Ford (F) to heating oil futures for the past year or so but have recently begun to combine it with the ratio between Japan’s Mitsubishi UFJ (MTU) and the gold etf (GLD). We thought we would attempt to explain our reasoning.

The Ford/heating oil ratio represents two economically sensitive or cyclical themes- autos and energy prices. Our view is that at an economic cycle begins with falling interest rates and strength in the autos and ends with tight capacity, rising interest rates, and higher energy prices. The cycle should begin with a rising Ford/heating oil ratio as bond prices rise and eventually end with a falling ratio as bond prices decline.

The Ford/heating oil ratio bottomed in November of 1981 even as the S&P 500 Index continued to decline into August of 1982. We argued last year that when the ratio turns higher- as it did late last year- it should mark the start of a rising equity markets trend. Fair enough.

We have also argued that there are two kinds of cyclical weakness- the good kind and the bad kind. The bad kind- in our view- goes with energy price weakness AND even greater weakness from Ford. In other words if crude oil and heating oil prices decline by, say, 30% as Ford’s share price falls by 60%… that is the ‘bad kind’.

The ‘good kind’ involves weakness in energy prices and strength in the share prices of the energy users. Absolute strength would be nice but at minimum we are looking for relative price strength. A decline of 30% for energy prices offset by, say, a rise of 30% for the share price of Ford would represent positive cyclical weakness.

Last year’s debacle represented the bad kind of cyclical weakness as virtually everything other than the dollar, yen, and Treasuries declined in price. Our view is that we are working into a similar situation to last year as commodity prices, Asian growth, and the commodity currencies start to weaken in response to dollar and bond market strength but our hope- and ‘hope’ is probably an accurate word- is that this time will be different. Instead of ‘bad’ cyclical weakness we are looking for ‘good’ cyclical weakness and one of the keys is the Ford/heating oil ratio. So far… so good.

At bottom is a comparison between the ratio of the Bank Index (BKX) to the S&P 500 Index (SPX) and the ratio between gold prices and the CRB Index.

The blazingly obvious point here is that… banks bad then gold good. In other words the reason gold prices began to rise back in 2006 only to spike to a relative strength peak into early 2009 was… the banks were in the process of leading the markets and the global economy into the kind of future that favors ammunition, canned goods, and bars of gold. Fair enough.

Our view is that the MTU/GLD ratio will trend with the Ford/heating oil ratio. Our view is that commodity price weakness in 2008 presaged the end of the financial system while commodity price weakness in late 2009 or, perhaps, 2010 will lead to lower long-term interest rates, better share prices for the banks of commodity ‘user’ countries (U.S., Japan, Europe) and ultimately lower gold prices as the gold/CRB Index ratio declines back to a more healthy level below 2:1. Given that the CRB Index is currently close to 250 we might argue in favor of support for gold in the 700’s but our conviction is that 500 or so is a better price target.