On a daily basis we write about what we are thinking about. Whether we are thinking about important or even relevant things is open to debate. Today, for example, we have been pondering a quote that we have heard in relation to an unrelated topic because it seems somewhat appropriate.

“When one door closes another door opens; but we so often look so long and so regretfully upon the closed door, that we do not see the ones which open for us.” – Alexander Graham Bell

When one door closes another door opens. Is this true for the markets as well? We believe so and often refer to this using the term ‘offsets’.

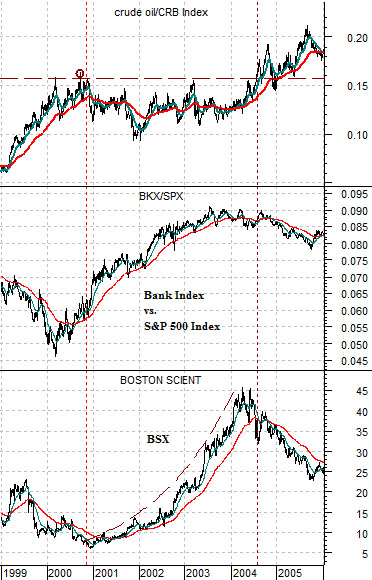

Belowis a chart comparison from 1999 through 2005. The chart shows, from top to bottom, the ratio between crude oil prices and the CRB Index, the ratio between the Bank Index (BKX) and the S&P 500 Index (SPX), and the share price of Boston Scientific (BSX).

The cyclical ‘door’ closed in 2000. This began with the peak for the Nasdaq in March which lined up with the low point for the banks and was followed later in the year with the top for energy and base metals prices which marked the lows for Boston Scientific.

The argument is that while many recall the equity bear market that ran from 2000 through 2002 few actually realize that it was less of a ‘bear’ than a ‘rotation’. Why? Because very few bear markets feature a near-doubling of the relative prices of the banks and an 8-fold price increase in a medical products company.

When the cyclical ‘door’ closed the markets rotated into other sectors. The weight of the cyclical decline created the impression of a negative trend as investors attempted to find the bottoms for the large cap tech and telecom stocks. As the quote states, ‘… we so often look so long and so regretfully upon the closed door, that we do not see the ones which open for us.’

The point? Yesterday it felt as if the energy ‘door’ closed but at the same time our sense was that the door opened for the energy ‘users’ and the financials. The temptation will be to spend the next few years trying to time the bottom for the commodity theme while ignoring the fact that new trends and new bull markets have begun.

Equity/Bond Markets

We may be confusing things with our door imagery but the point that we are attempting to make is still somewhat important. Trends run for a long time. When a trend finally ends an entire generation of investors has become so used to trading on the same theme that years can pass before many realize that something is different. We learned this lesson (hopefully) back in the 1980’s as we attempted to relive past glories in the commodities sector even as brighter lights made hay in the consumer and tech sectors.

So… let’s shift from vague meanderings about days gone by back to the here and now.

We are going to drag out a chart that we haven’t shown since some time back in 2009. The argument is based on the ratio between the share price of Goldman Sachs (GS) divided by the CBOE Volatility Index (VIX).

The GS/VIX is an interesting ratio. GS represents the financial sector while the VIX stands for volatility and uncertainty.

A rising ratio is bullish as a recovery should be led by the financials while including a reduction in concern. When GS is trending higher while risk is abating… the trend should be bullish.

The idea a few years back was that the trend started to improve in November of 2008 when the GS/VIX ratio made its final low. There was a lag, however, between the point of maximum stress in November and the eventual bottom for the laggard financials. For this we are going to use the share price of Bank of America (BAC).

The chart below shows that the GS/VIX ratio bottomed a few months before the markets gained enough confidence to pivot the share price of BAC upwards. From this we conclude that an upward trend for the GS/VIX ratio concurrent with downward pressure on BAC could be nothing more than the markets getting ready for something dramatic.

Below is the same chart from 2011 to the present day.

The argument is that the point of maximum stress was reached around the end of last year’s third quarter as the GS/VIX ratio made what appears to be its final low.

We are now roughly three months into the ‘lag’. We can see that the GS/VIX ratio has been on the rise and is gradually approaching its 200-day e.m.a. line. We can also see that the markets spent much of the final quarter of 2011 selling the laggard banks on the assumption that things were still going to get worse.

But… as time goes by a bearish outcome appears less and less likely.

Between 2000 and 2004 (chart on page 1) the crude oil/CRB Index ratio stopped making new highs. Through this time frame the markets shifted over to a variety of new themes. The trend moved back to the commodities sector in 2004 as crude oil and heating oil futures prices moved to new all-time highs.

The detail that we found interesting yesterday was the minor price strength for names such as GM. This theme should start to improve once the energy theme begins to roll over.