With the end of the quarter approaching along with the prospect of a potential trend change we thought we would take another swing at the topic that we introduced in yesterday’s issue.

The basic argument runs something like this. When economic growth expands to the point where the supply of critical resources becomes tight interest rates tend to rise. The resources in question might be labor, energy, capital, raw materials, etc.

Interest rates rise until the yield curve flattens or inverts and eventually this leads into an economic slow down and/or recession which reduces pressure as the demand for critical resources declines.

The longer the economy operates below potential the greater the output gap but eventually positive growth will work through the excesses of supply until prices and interest rates begin to rise. Rinse and repeat.

We are attempting to combine two different arguments today. The first is that economic growth tends to lag behind changes in interest rates by about two years. The second is that there are sectors that rise in price during the output gap and when these sectors turn lower it indicates that the yield curve should be ready to flatten.

Below we show a chart of the sum or combination of U.S. 3-month TBill yields and 10-year Treasury yields from 2001 into 2003. Below right we feature a comparison between the share price of Boston Scientific (BSX) and lumber futures from 2003 into 2005.

The charts have been offset by two years. The idea is that changes in yields in 2002 were ultimately impacting economic growth in 2004.

BSX and lumber futures represent the kind of markets that rose in price in between the start of economic weakness at the end of 2000 and the first hike in the Fed funds rate in 2004. The charts have been set up to suggest that the second wave of falling interest rates that began in the spring of 2002 and moved to new lows later that summer helped to create sufficient economic growth- two years later- to mark the cycle peak for the themes represented by BSX and lumber futures.

We will continue with this argument below.

Equity/Bond Markets

It doesn’t make sense to watch lumber and medical products makers such as BSX during the current cycle because the pressures are coming from a different direction. In other words when capital spending collapsed post-2000 the economy was forced to find growth from consumer spending which in the recent instance it was consumer spending that was placed under pressure as real estate prices declined.

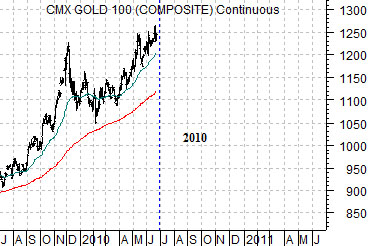

Below we show the sum of 3-month and 10-year U.S. Treasury yields from 2007 into 2009 and a chart of gold futures from 2009 to the present day. Similar to page 1 these two markets have been offset by two years.

The argument for a peak in gold prices around the end of the quarter rests in part with the way yields turned lower through the second half of 2008.

Above we showed that the peak for BSX lined up with the peak for yields two years previous while the final highs for lumber lined up with the break to new lows for yields in 2002.

If the comparison applies to the current case then it is possible that gold prices could be at a peak as we move into July. It is also possible that gold prices will remain stronger until two years AFTER the break to new lows for yields which took place in the fourth quarter of 2008.

Further below we show once again the yield spread between 30-year and 3-month Treasury yields. The argument is that the yield spread began to rise at the start of 2001 and after holding near the highs through 2003 and into 2004 turned lower as lumber futures prices and the share price of BSX started to decline.

Most economists seem to believe that the Fed will not start to raise interest rates until 2011 or, perhaps, even 2012. With TBill yields close to 0% the yield spread could still decline if longer-term interest rates are gradually squeezed lower.