One of our more regrettable tendencies is to argue and argue a point until it starts to work and then move on to tilt at the next windmill. We had actually set up the first two pages today to cover another topic and then decided that it would probably make sense to go back over the dance between the Japanese yen, bond prices, and the laggard cyclicals.

First we start with the basic relationship. The argument is that the Japanese yen and the long ends of most major bond markets (we have shown comparisons between Canadian, U.S., Japanese, and German bond futures and the trends are virtually identical) have served as destinations for risk-averse capital. The greater the risk associated with what has seemed like a never ending series of crises… the higher bond prices and the Japanese yen move.

So… the chart shows that over the past 8 or so months there is little to distinguish the path of the yen versus that of the U.S. 30-year T-Bond futures. From this we take the logical leap that a much weaker yen could lead to some amount of downward pressure on bond prices.

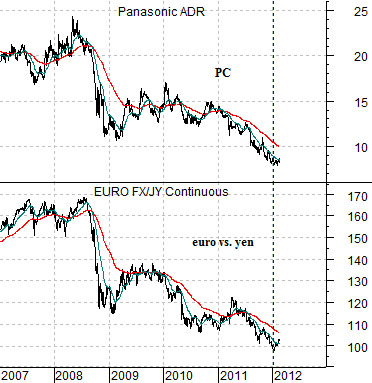

Next is a comparison between Panasonic (PC) and the cross rate between the euro and the yen.

The markets work through offsets, unintended consequences, and self fulfilling prophecies. Strength in one sector creates weakness in another sector or, at times, weakness in one sector leads to strength in another. An example of the latter might be the collapse in developed country capital spending post-Nasdaq bubble that pulled interest rates lower and inflated housing prices. Weakness in capital spending led to lower interest rates and stronger real estate prices.

As the yen rose against the dollar it also strengthened against the euro. The euro/yen cross rate shows that the euro has been driving lower relative to Japan’s currency since 2007- 08. Yen strength against both the dollar and euro was based on a myriad of concerns unrelated- we would argue- to Japan but the end result was the virtual annihilation of the profit margins of Japan’s major exporters. In other words as money moved into the yen in search of safety the unintended consequence was sharp bearish pressure on many of Japan’s major corporations which, in turn, helped support the conclusion that it made sense to focus on risk averse investment options.

Equity/Bond Markets

The ‘laggard cyclical’ sectors that we have focused on include a number of major banks as well as Japanese exporters like Panasonic and Sony. We use specific stocks to represent broader themes.

Just below is a comparative view of 10-year U.S. Treasury yields and the ratio between Japanese bank Mitsubishi UFJ (MTU) and the S&P 500 Index (SPX).

The argument is that yields should turn higher once MTU begins to strengthen relative to the broad U.S. stock market. In other words… a sustained pivot to the upside by the MTU/SPX ratio should lead to a rising trend for long-term U.S. interest rates.

Next is a comparison between Japanese 10-year (JGB) bond futures and the ratio between Panasonic and the S&P 500 Index (PC/SPX).

One might argue that the MTU/SPX ratio turned higher around the final days of trading in 2011. The PC/SPX ratio, on the other hand, has done little more than ‘not make a new low’ for a whopping 10 straight trading session. The point is that IF this is the turn THEN it is ‘so fresh’ that it is almost impossible to see it on a long-term chart.

In any event the idea is that the stronger the PC/SPX ratio the greater the downward pressure on Japanese bond prices.

Then we have a chart of Bank of America (BAC) and the combination of the Japanese 10-year bond futures times the Japanese yen futures. The JGB times yen has been rising relentlessly since the middle of 2007 as an offset to the bearish trend for U.S. home prices and banking shares.

The suggestion here is that a weak yen should relate to weak bond prices. Strength in the laggard banks and Japanese exporters should follow a weaker yen and go with rising yields and falling bond prices. The offset to a declining yen and bond prices should be a rising trend for the ‘laggard cyclicals’.