The question today is whether the long end of the Treasury market is actually leading the short end- and hence the Fed- by close to a year.

Below we compare the U.S. 30-year T-Bond futures and 3-month eurodollar futures with the charts shifted or offset by one year. The argument is that the peak for the TBonds in 2003 led the top for short-term debt prices in 2004. The lows for the 30-year T-Bonds in 2006 preceded the cycle trough for 3-month eurodollar prices in 2007 by roughly the same length of time.

The point, we suppose, is that the TBonds reached a peak at the end of 2008 and have not risen back to those lofty levels over the past 15 months. If the start of rising long-term interest rates in December of 2008 was pointing towards rising short-term interest rates in December of 2009… then the chart at right makes sense. The chart shows that the U.S. dollar and 3-month TBill yields began to push upwards through December of last year as the combination of crude oil futures and the Australian dollar reached a peak. If history were to be kind enough to repeat the trend for short-term yields would remain positive until a year after the TBonds reached the next price bottom. As things stand that would be 2011 at the earliest.

Equity/Bond Markets

We tend to believe that unless we hammer away at a point on multiple occasions it is just another of the many topics and arguments that we regularly toss against the wall. When we come back to an issue time and time again it usually means one of two things. Either we believe that it is important and relevant or, as is often the case, we are perplexed by the fact that it is not working.

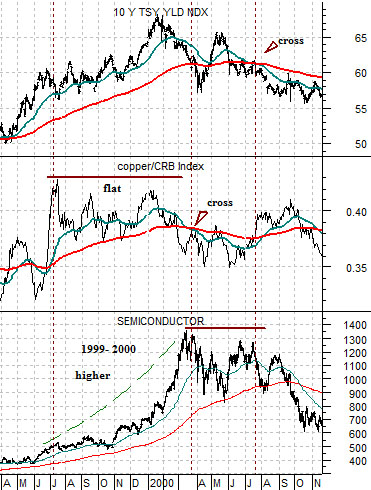

Below we compare the Semiconductor Index (SOX), the ratio between copper and the CRB Index, and 10-year Treasury yields (TNX) from 1999- 2000.

The argument is that WHEN the copper/CRB Index ratio peaks the markets tend to rotate out to a new trend. IF the dollar is weaker then the focus shifts over to the grains. IF the dollar is stronger then the tech theme (i.e. semiconductors) tends to benefit.

From the peak in the copper/CRB Index ratio to the point in time when the 50-day e.m.a. line crosses down through the 200-day e.m.a. the chip stocks have tended to rise in price. The two ‘stops’ that we use are based on the moving average ‘cross’ by the copper/CRB Index ratio and a ‘cross’ by 10-year Treasury yields. Between 1999 and 2000 the window for concentrated ‘tech’ strength stretched from mid-1999 into the end of the first quarter of 2000.

At present (see chart below) the copper/CRB Index ratio is holding near the highs and is well above the moving average lines. The same is true for 10-year Treasury yields. This suggests that the cyclical trend is still strong enough to support a rotation into the semiconductors. For this to happen we are going to have to see some big names break out of the current trading ranges. Notice on the chart below that Cisco managed to push above 25 this week although Intel is still holding below resistance around 21.50.