We grant that the left side of the chart always makes more sense than the right side but as we worked through past trends and cycles we couldn’t help but notice that there was a kind of cyclical disconnect in the Asian growth theme at key points in time. We call this disconnect the ‘9-month lag’.

It would be nice if the markets would simply repeat the same trends in the same sequences but, alas, life is not quite so kind. Our view is that the markets repeat trends over and over again but always with a few key differences that make it difficult to see the actual repetition.

Just below is a chart comparison through 1997. The chart features the sum or combination of copper and crude oil futures along with Hong Kong’s Hang Seng Index.

The trend for the Asian equity markets tends to be quite similar to the trends for energy and base metals prices. The chart shows that at the start of 1997 copper and crude oil futures prices began to decline but after a few months of downward pressure the Hang Seng Index punched up to new highs.

The point is that the negative trends for copper, crude oil, and the Hang Seng Index began at the same point in time even though the Hang Seng Index pushed well above the negative trend into the autumn of that year. Between the start of the negative trend and the snap lower back to the trend for the Hang Seng Index nine month elapsed.

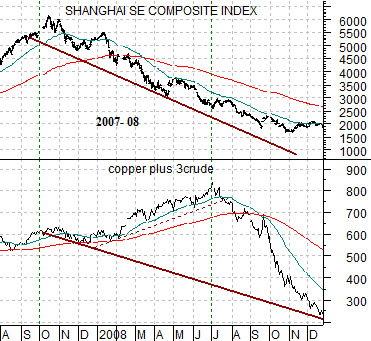

Next is a comparison between China’s Shanghai Composite Index and the sum of copper and crude oil from August of 2007 through 2008.

The argument is that ‘Asian growth’ turned negative in the autumn of 2007. Notice that as the Shanghai Comp. trended lower the commodity markets bubbled upwards for nine months until finally collapsing in mid-2008.

In both cases shown a declining trend was set and an associated market diverged from this trend and headed higher for 9 months before succumbing to the pressures of markets gravity. With this in mind we push on to the current situation on the next page.

Equity/Bond Markets

Below is a chart comparison between the U.S. Dollar Index (DXY) futures and the Hang Seng Index.

We are expanding on today’s first page point using a different perspective. Instead of focusing on the trend for copper and crude oil prices we are using the dollar. Given that a rising dollar tends to act as a negative for commodity prices the argument is that when the dollar begins to trend higher the corresponding trend for Asian growth turns lower.

In any event… as constructed the chart suggests that the trend for Asian growth turned negative during the fourth quarter of last year. The peak for the Hang Seng Index in November lines up with the bottom for the dollar.

If the Hang Seng Index is trending inversely to the dollar and the dollar swung higher late last year then an intuitive leap suggests that the Asian growth has been negative for anywhere between 5 and 7 months.

Why 5 and 7 months? If we take the argument literally then the trend changed around the end of November. If we mark the trend in terms of calendar quarters- which is usually the way trends work- then the shift took place at the end of last year’s third quarter.

If the Asian growth theme is negative then the 9-month lag shown on page 1 becomes more than a little relevant. Our view is that this could lead to an apparent acceleration of the cyclical recovery through the end of this quarter in a manner similar to the Hang Seng Index in 1997 and the commodity markets in 2008 followed by weakness and falling long-term yields through the back half of the year.

Below are charts of lumber futures and the ratio between Japanese bank Mitsubishi UFJ (MTU) and the gold etf (GLD).

Earlier this year we argued on more than a few occasions that the MTU/GLD ratio might be set to swing higher around the end of the second quarter. The idea was based on the way that Citicorp lagged the recovery in the markets between 1990 and 1991.

The markets worked through a sequence of sorts through the previous decade. The collapse of capital spending that marked the Nasdaq’s decline from 2000 into early 2003 pulled interest rates lower and as yields declined lumber prices- sensitive to the housing market- rose. By the spring of 2004 energy prices strengthened to the point where interest rates were pushed higher and this marked the peak for lumber futures prices.

Once lumber prices turned lower the markets turned one sector after another lower. We have shown on many occasions how lumber began to decline followed by the forest products stocks, the home builders, and eventually the major financials.

The point is that if we compare the way lumber futures peaked in mid-2004 with the highs for the MTU/GLD ratio at the start of 2006 we end up with an 18-month lag between the two trends. Given that lumber prices turned higher in early 2009 the argument suggests that we could either see a positive trend for the laggard banks (MTU) or some kind of negative trend for gold prices starting some time this summer.