When the price of a market, security, or asset breaks to all-time highs a subsequent period of consolidation is to be expected. There will be times, of course, when prices will simply continue to rise but, in general, the momentum and buying power necessary to take out a major resistance point will lead to a bit of backing and filling.

We start off today with a few thoughts on copper futures. Below is a chart comparison between the ratio of gold to the CRB Index, the share price of McDonald’s (MCD), copper futures, and the ratio between Japanese bank Mitsubishi UFJ (MTU) and the gold etf (GLD).

We argued some time back that the key for an upswing in the laggard banks was a down side break in the ratio between gold and the CRB Index below the 200-day e.m.a. line. This took place in early December of last year.

Concurrent with this the chart shows that copper futures pushed above the previous peak around 4.05. New highs for copper suggested a strong cyclical trend that pulled gold down on a relative basis, created selling pressure for MCD, and sent the ratio between MTU and the GLD upwards. So far, so good.

The problem of late has been that after pushing upwards into February the price of copper has recently weakened. This has helped move long-term Treasury yields lower while shifting the focus of the markets back to gold and crude oil.

The argument here, we suppose, is that the charts of MCD and the gold/CRB Index are virtually identical and both are the mirror images of the chart for copper futures. If copper is simply consolidating the break out with a slow pull back to the rising 200-day e.m.a. line then in due course the trend will shift from falling yields and ‘defensive’ back to rising yields and ‘economically aggressive’.

In a sense this is a classic example of the kind of uncertainty that prevails when the dominant theme (i.e. copper) starts to weaken. If copper continues to decline then large cap consumer names should do better along with gold but if copper swings back to the upside then a return to better prices for the laggard banks and cyclical sectors seems appropriate. As is usually the case the eventual answer will come from the direction of long-term Treasury yields which have fallen from almost 3.75% in February back to close to 3.3% at present.

Equity/Bond Markets

April 29 (Bloomberg) — The Bank of Japan raised its growth forecast for next year on optimism the economy will bounce back on reconstruction work and restored power supplies after factory output dropped by a record in March.

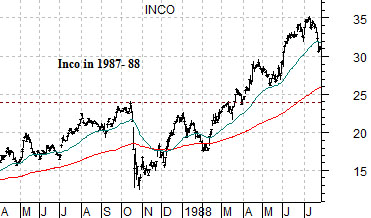

We are going to have to run through this very quickly… starting with the two charts below of the Nikkei 225 Index from the current time period and nickel producer Inco from 1987.

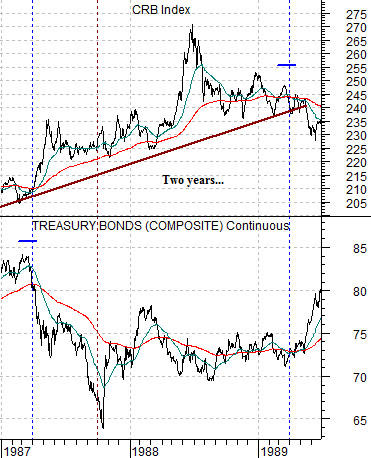

The argument is based on the charts just below. In the spring of 1987 long-term U.S. bond prices began to decline and five or six months later the stock market ‘crashed’. Inco was one of the first stocks back up to new highs because… the 2-year lag argued that the cyclical peak would not occur until two years AFTER long-term bond prices started to decline. The chart at top right shows that the CRB Index remained positive into the spring of 1989.

This is mostly ‘a wishin’ and a hopin’’ but the thought is that IF the Nikkei rebounds to new highs within the next few months THEN the trend may be an extension of the 2-year lag. In other words- from the chart at bottom – the Japanese bond market turned lower in the autumn of 2010 which argues for a continuation of the stronger cyclical trend into the autumn of 2012.

The point? From this rather imaginative perspective the recent decline in the Nikkei is strangely similar to the 1987 stock market crash in that it took place five or six months after the cycle peak for bond prices. A case can be made for the Japanese stock market IF it climbs right back up above its 200-day e.m.a. line and then moves on to new highs over the next quarter of two.