Thursday closed the day on the highs, leaving the Nas Composite and Nas 100 on new highs for the year. The S&P 500 and Dow are not far below the years highs, Thursday’s move came on heavier volume for an accumulation day across the broader markets. The TRIN closed at 1.26, still too high like Wednesday reflected for the rise. The VIX closed at 16.47 on the 10dma. Gold fell $8.80 to $1140 an ounce and oil down 2 cents to $83.70 a barrel.

The market opened very weak and under Wednesday’s low, most of it was off the fears in Greece sending the dollar up and the market down. The market shrugged most of it off in the first hour and then moved higher throughout the day. The Nas indexes are very near the upper Bollinger, a RSI at 74 is rising quickly we’ll watch for 80 for that severe overbought territory. The SPX and Dow aren’t as high at 67 and not into the upper BB yet. On each index on the daily chart the CCI diverged today, it closed lower while price closed higher. With the expansion today pushing up with a TRIN still over 1, although it did drop throughout the day I am still thinking we are seeing some profit taking up here and the advance is not all buying.

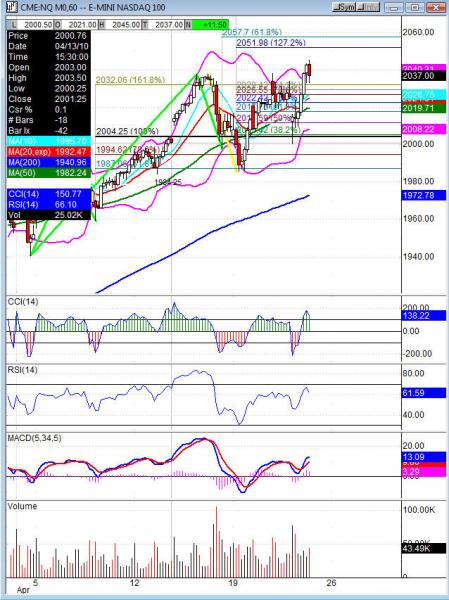

The ES once again rejected a close over 1204. Through 1204 and onto 1211 and 1214.75 would be where the bulls head. Under 1185.5 and we look for 1179.5 and onto 1171 for support on the ES. The NQ under 2008.25 look for 1998.50 and 1985.75 is likely. 2046.25 resistance on the NQ and then we could see a move as high as 2057.75 without a lot of struggle. The SOX was on watch for the Nasdaq to find a lift and it was strong on Thursday, enough of a lift to bring the sector just under 401.77 swing high from April 15th.

After the bell Microsoft (MSFT), Amazon (AMZN), PMCS, CRBC all tumbled off earnings while Capital One (COF) Rambus (RMBS) and American Express (AXP) all saw a nice lift in after hours trading. The mixed action didn’t have a lot of reaction on futures, although they traded down slightly. The market is likely to focus on any more Greece news, the economic data due out and start looking to next week the final week of the month. Which could keep Friday from seeing a big range or any rotation outside the weeks range.

Economic data for the week (underlined means more likely to be a mkt mover) Friday 8:30 Core Durable Goods Orders, 8:30 Durable Goods Orders, 10:00 New Home Sales. Saturday IMF meetings (Greece concerns likely to be a focus). Monday nothing due out, Tuesday 9:00 S&P/CS Composite 20 HPI, 10:00 Consumer Confidence, 10:00 Richmond Manufacturing Index. Wednesday 10:30 Crude Oil Inventories, 2:15 FOMC Statement, 2:15 Federal Funds Rate. Thursday 8:30 Unemployment Claims, 10:30 Natural Gas Storage. Friday 8:30 GDP, 8:30 Advanced GDP Price Index, 8:30 Employment Cost Index, 9:45 Chicago PMI, 9:55 Revised UoM Consumer Sentiment, 9:55 Revised UoM Inflation Expectations.

Some earnings for the week (keep in mind companies can change last minute: Friday pre market CMS, HON, IR, SLB, TRV, XRX and nothing after the bell. Monday pre market BLK, CAT, HUM, SOHU, TZOO, and after the bell ALB, AMP, BSX, ELX, RSH, TXN, VECO, WMS. Tuesday pre market MMM, BP, CIT, CMI, DD, F, LXK, MHP, NEM, ODP, OXPS, TLAB, TYC, X, UAUA, UA, UPS, LCC, VLO, and after the bell BRCM, DWA, NSC, PNRA, ULTI.

NQ (Nas 100 e-mini) Friday’s pivot 2027.50, weekly pivot 2010.50. Support: 2022.25, 2015.25, 2008.25, 2003, 1998.50. Resistance: 2037.75, 2043.25, 2046.25, 2052, 2057.75