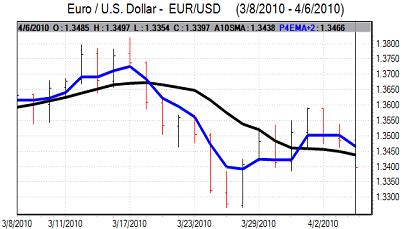

EUR/USD

The Euro came under renewed selling pressure in Asian trading on Tuesday with lows near 1.34 as there were renewed fears over the Greek borrowing situation.

The Euro-zone Sentix investor index strengthened to 2.5 for April from -7.5 the previous month. This was the first positive reading since the second quarter of 2008 which was much stronger than expected and should provide some degree of relief over near-term economic prospects.

The Euro was still unable to gain any significant support as underlying debt fears remained an important negative factor. There were press reports that Greece was uncomfortable with the prospect of IMF support and would look to re-negotiate the recent support package. These reports were denied, but spreads on Greek bonds over German bunds widened to over 400 basis points which undermined the Euro and it dipped to 7-week lows near 1.3355.

There were no further US economic data releases during Tuesday and there are only limited releases due over the remainder of this week. There is still likely to be a mood of cautious optimism surrounding the economy and the dollar should be in a position to gain support on yield grounds.

Within the FOMC minutes released on Tuesday, there were comments indicating that there was no fixed time for the extended period language and the members were broadly confident that the Fed could react and tighten policy quickly if required. There were concerns over the contraction seen in bank lending seen during the first two months of the year. Overall, the minutes did not provide additional dollar support with the Euro recovering back to the 1.34 area.

Source: VantagePoint Intermarket Analysis Software

Call now and you will be provided with FREE recent forecasts

that are up to 86% accurate * 800-732-5407

If you would rather have the recent forecasts sent to you, please go here

Yen

The yen has been resilient over the past 24 hours as exporter selling remained a key feature. The dollar again tested support levels below the 94 level in Asian trading with Euro/yen selling also significant in supporting the yen against the dollar.

The yen continued to edge stronger against the dollar later on Tuesday and the Euro dipped to test support near 125.30 before finding some buying interest.

Underlying risk appetite was still broadly resilient which limited the scope for further yen gains, but the dollar was unable to regain the 94 level.

Sterling

There was a Sterling decline back to lows just below 1.52 on Tuesday as the US currency gained ground. Confirmation that a General Election would be called on Tuesday for May 6th was not a surprise, but the UK currency was pushed lower by one opinion poll which suggested an increased risk of an indecisive outcome.

The opinion polls will remain under close scrutiny in the short term and Sterling will tend to gain some support if the polls suggest a clear outcome. There will still be important underlying fears over the budget situation.

The construction PMI index rose to 53.1 for March from 48.5 the previous month and this was the first figure above the 50.0 benchmark for over two years. The data should maintain some degree of optimism towards near-term economic trends and the PMI services-sector index will be watched closely on Wednesday.

Sterling found support below 1.5150 against the dollar and pushed higher back to the 1.5280 region later in US trading with the currency gaining support from solid risk appetite.

Swiss franc

The dollar pushed to a high near 1.0720 against the franc on Tuesday before hitting tough resistance and edging back towards 1.0680 later in the New York session. The Euro maintained its position above 1.43 against the Swiss currency.

Renewed fears surrounding the Greek situation will maintain a negative Euro factor and should limit the potential for a sustained Euro advance against the franc.

Swiss consumer prices rose 0.1% in March to give a 1.4% annual increase. This was in line with market expectations and should not have a substantial impact on monetary policy expectations.

Source: VantagePoint Intermarket Analysis Software

Call now and you will be provided with FREE recent forecasts

that are up to 86% accurate * 800-732-5407

If you would rather have the recent forecasts sent to you, please go here

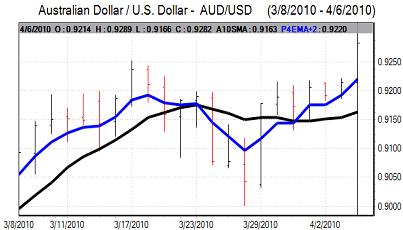

Australian dollar

The Reserve Bank of Australia increased interest rates to 4.25% from 4.00% at the latest policy meeting. Given that there had been some doubts over the potential for a rate increase, the decision provided some Australian dollar support, especially with a relatively hawkish statement.

The currency pushed to a high near 0.9250 against the US currency and there was a further advance to 0.9285 in New York as the US currency edged weaker. The Australian dollar also gained support from firm commodity prices.