EUR/USD

The Euro was blocked in the 1.3350 area against the dollar on Monday and weakened steadily during the day as underlying doubts surrounding the Euro-zone outlook increased following the EU Summit.

There was a warning from Moody’s that the Euro-zone remained in danger of downgrades and the comments from Standard & Poor’s still suggested that there was a high risk of rating action given that Euro structural issues had not been addressed sufficiently. There were important fears that there could be a downgrade within the next few days which sapped Euro support, especially given fears that France could be subjected to a double downgrade.

The lack of confidence was illustrated by a renewed widening in the peripheral yield spreads as Italian and Spanish bond yields rose sharply. The latest ECB data indicated that peripheral bond purchases had fallen sharply to below EUR1.0bn in the latest week from over EUR8.0bn previously. This could be an indication of underlying investor demand, but confidence will remain extremely fragile.

There will be further speculation that the Euro-zone economy is heading for a deep recession, especially given the commitment to fresh austerity measures and there will be pressure for further ECB interest rate cuts. The Euro was, therefore, also undermined by a further deterioration in yields relative to the US dollar and it retreated to lows near 1.3160 before a weak recovery. The dollar index maintained a firm tone as it broke above important resistance levels.

There were no significant US developments during the day as the focus remained firmly on Europe. In this context, Tuesday’s Federal Reserve FOMC meeting may receive relatively little attention unless there is a surprise decision. The most likely outcome is that Bernanke will examine contingency planning in the event of further stresses within the European and global banking sector.

Source: VantagePoint Intermarket Analysis Software

Call now and you will be provided with FREE recent forecasts

that are up to 86% accurate* 800-732-5407

If you would rather have the recent forecasts sent to you, please go here

Yen

The dollar found support in the 77.60 area against the yen on Monday and pushed to highs near 78, although it was unable to break any important resistance levels.

Both currencies continued to derive safe-haven support from a lack of confidence in the Euro-zone economy. There were also important reservations surrounding the Asian outlook as equity markets remained under pressure and there was underlying demand for the Japanese currency.

The Bank of Japan stance will be watched very closely, especially as any move by the Swiss National Bank to weaken the franc further would increase potential support for the yen as a safe-haven and increase pressure on the central bank to resist yen gains.

Sterling

Sterling dipped to lows around 1.5550 against the dollar on Monday before finding support and rallying to a high near 1.5650. There were sharp moves on the crosses as the Euro weakened sharply against Sterling. The UK currency pushed to highs near 0.8450 which was an important break from recent ranges and a nine-month high for Sterling.

There was Sterling buying in relation to corporate dividend payments, although there was also evidence of UK demand as a refuge from the Euro-zone. In this context, the controversial UK decision to veto a EU Treaty did not have a negative short-term currency impact.

The latest RICS house-price data improved slightly to a reading of -17 for November from -24 previously, although there was little sign of an underlying improvement in confidence. The latest inflation data will be watched closely on Tuesday, although the monetary policy impact is likely to be very limited as the Bank of England focuses on the recession threat.

Swiss franc

The dollar maintained a firm tone on Monday and was finally able to break above resistance in the 0.93 area which helped trigger a high around 0.9380. The franc was unable to make any impression on the Euro ahead of Thursday’s National Bank policy meeting as there was solid Euro support on any move to the 1.23 area.

There was further speculation that the central bank would move to announce a further weakening of the franc. There was also the possibility that the bank would move to introduce negative official interest rates to curb any demand for the Swiss currency in the event of any further deterioration in Euro confidence.

Source: VantagePoint Intermarket Analysis Software

Call now and you will be provided with FREE recent forecasts

that are up to 86% accurate* 800-732-5407

If you would rather have the recent forecasts sent to you, please go here

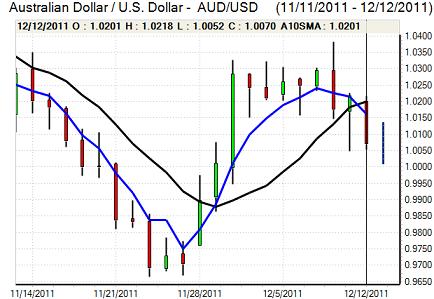

Australian dollar

The Australian dollar was unable to make any impression on the US currency on Monday and dipped to lows around 1.0030 before a tentative recovery. There was a general tone of risk aversion which undermined the currency and a slide in the Chinese equity market to 3-year lows did little to improve sentiment.

The domestic data did not have a major impact as business confidence held steady according to the latest NAB survey while there was a sharp third-quarter decline in housing starts. Risk-appetite trends are likely to remain the dominant short-term market influence.