For the month of October, I see the U.S. dollar as the dominating driver for the markets, particularly commodities. Many commodities have been divorced from supply and demand fundamentals and are being seen as inflation hedges, or safe-haven investments. Weakness in the U.S. dollar has helped drive gold to a new record high, and I think gold’s rally has legs. Demand for gold is likely remain strong as the dollar remains weak, which should be the case until the Federal Reserve starts tightening interest rates and the job market starts to improve.

Gold and the Dollar

Gold has been a mover and a shaker, hitting a record high above $1,049 per ounce this week. I remain bullish, but rather than chase the trend, I’d recommend waiting for a pullback to consider buying at lower levels. Wait, and be patient. The market will see some corrective moves. The rally in gold is in part driven by inflation fears, but also by the weak dollar. The ICE U.S. Dollar Index futures, which track the U.S. dollar against a basket of six global currencies, are down 15 percent from this year’s highs. The dollar isn’t moving as much on a percentage basis as some of the commodity markets (such as gold) it is fueling; it’s more of a psychological factor.

I recommend buying December gold on a pullback to the breakout level at $1,025, and risk $20. Gold is a little overbought right now; just a few days ago this market was under $990. Don’t get me wrong–I’m very bullish gold for the long-term. By Christmas 2010 I think gold will be at $1,200. The swings, however, could be big in both directions. I see a bull market from way back to 2001 on the charts, and I expect it to continue.

Crude Oil

The Energy Department’s latest weekly crude oil inventory report, released on Wednesday, October 7, showed crude oil supplies dropped 978,000 barrels to 337.4 million. Despite that bullish report, NYMEX November crude oil closed $1.31 a barrel lower at $69.57. However, prices are still up more than 50 percent this year.

Analysts were expecting inventory levels to show a surplus, but we got a drawdown .The market should have rallied on this news but didn’t. While I’m also long-term I’m bullish crude oil, this isn’t a positive sign for the near-term, and the market looks to be consolidating and trending lower on a technical basis.

For now, I’d recommend playing the recent range. I recommend selling around $72 – $74 and buy on breaks under $68. I think we have a trading affair in crude oil. Until this market breaks out on a weekly basis, buy on the low end of the range, and sell near the top. Don’t forget to always use stops.

Stock Indexes and Treasuries

Our economy seems to be doing pretty well overall, but we do have concerns. The data has been mixed. Housing is trying to bottom, and manufacturing is coming along. GDP seems to be improving. Consumer spending is not really kicking in yet, although consumer confidence has improved. What’s the holdback? Employment. We keep losing jobs. September’s employment report was a disappointment, showing a non-farm payroll drop of 263,000 and the unemployment rate ticking up to 9.8 percent.

We are now in the midst of the third-quarter earnings reporting period, which will be a major event for the stock market that should provide some further interpretation of the state of the economy. Alcoa, the largest aluminum producer, was the first company in the DJIA to report, and posted an unexpected profit. Nonetheless, according to a Bloomberg survey, S&P 500 companies are expected to show a ninth straight quarter of declining profits.

October is usually a down move for stocks, but so far, we haven’t seen it. For the December S&P futures, I think a break to $1,010 and also to $975 seem like logical places to get long if you believe in the recovery story. If the market pops to $1,065 this month, I’d look to sell. That’s my range for October. A few good earnings reports in the next week could drive the market as high as $1,100, but that should mark resistance in the near-term.

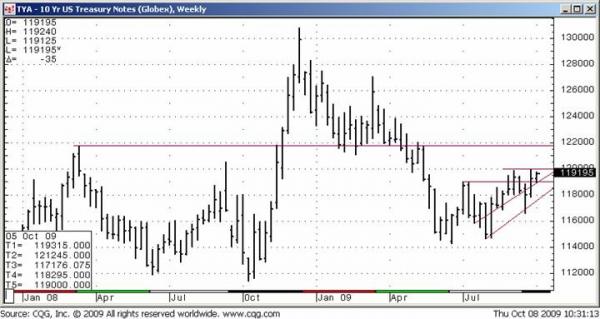

To me, it seems rather bizarre to me that interest rates are so low. Stocks and bonds seem to be interpreting the economic environment a bit differently. On Wednesday, October 7, the 10-Year Treasury note futures rallied after a $20 billion auction met strong demand. The bid-to-cover ratio, which gauges demand by comparing total bids with the amount of securities offered, was 3.0, higher than the 2.55 average over the past 10 auctions. We had $60 billion in assets chasing $20 billion in securities, and the 10-year yield was only about 3.20 percent, 3.25 percent. That’s pretty low historically. That seems to imply people are avoiding risky assets and clearly, are interested in Treasuries. But when you look at the surges in riskier assets, including gold, crude oil or stocks, you’d sure think otherwise. You’d think people aren’t afraid of risk.

Who is right? I think the Treasury market is looking at the state of the economy right now, and gold and stock indexes seem to be looking several months down the road. Treasuries are concentrating on the job situation, and expect the Federal Reserve to keep interest rates low for the foreseeable future.

This week, we saw Australia’s Central Bank step out and start raising interest rates, boosting its cash rate target to 3.25 percent. This week, Kansas City Federal Reserve Bank President Thomas Hoenig said that in the U.S. “we will need to remove our very accommodative policy sooner rather than later,” and last month, Fed Governor Kevin Walsh said rates may need to be raised “before it is obvious that it is necessary,” and “possibly with greater force than is customary.”

Not so long ago, it was unanimous among the Fed policymakers that expansion was needed, pumping money into the system was needed, and rates would stay indefinitely near zero. Now we are seeing some division in terms of what and when this policy will need to change.

This spring and summer, we can see how the 10-year Treasury note futures were trending upward. I think for the near-tem, selling seems like a better strategy. Take a stab on the short side around 119 – 125, and use a tight one-point stop.

These are just a few of my thoughts and ideas for the month of October. Please feel free to call me to discuss these or other markets, and to incorporate specific trading strategies for your account size and risk tolerance. Good luck and good trading!

Jeff Friedman is a Senior Market Strategist with Lind Plus. He can be reached at 866-231-7811 or via email at jfriedman@lind-waldock.com. You can follow Jeff on Twitter at www.twitter.com/LWJFriedman. Join Jeff for his monthly webinar, Friedman’s Futures Forecast, by visiting Lind-Waldock’s events page. You can view an archived webinar of this forecast at www.lind-waldock.com/events, where Jeff covers even more detail and more markets.

Past performance is not necessarily indicative of future trading results. Trading advice is based on information taken from trade and statistical services and other sources which Lind-Waldock believes are reliable. We do not guarantee that such information is accurate or complete and it should not be relied upon as such. Trading advice reflects our good faith judgment at a specific time and is subject to change without notice. There is no guarantee that the advice we give will result in profitable trades. All trading decisions will be made by the account holder.

Futures trading involves substantial risk of loss and is not suitable for all investors. © 2009 MF Global Ltd. All Rights Reserved. Futures Brokers, Commodity Brokers and Online Futures Trading. 141 West Jackson Boulevard, Suite 1400-A, Chicago, IL 60604.