|

Spring has arrived. Flowers are blooming. And so is inflation. We’ve been using the “I word” for quite a while here at the newsletter. As we look around, we see more and more signs indicating that people are waking up to the fact that inflation is here. The new awareness has accelerated the upward move in gold, oil, silver, base metals, food-related investments, better managed foreign currencies, and stocks in faster-growing countries. Fed Chairman Ben Bernanke, however, recently described the inflation in asset prices as “transitory,” suggesting that policymakers are either not convinced, don’t want to be convinced, or are avoiding admitting they’re convinced, about the current inflationary direction. Clearly, it is not in their best interest to excite the populace and create an inflationary psychology. This is why policymakers always downplay any potentially psychologically damaging news. It seems strange to us that the response of billions of people around the globe is being so blithely ignored. Real assets are in demand, driven by growing wealth in emerging countries, depreciation of the world’s reserve currency, and fears of supply disruptions and shortages as revolutionary fervor spreads throughout the Middle East and beyond. The above-mentioned investment categories will continue to rise. As we have recently said, gold will surpass $1,500 and then eclipse $1,600 in the not-too-distant future. Oil is on its way to $150 per barrel. Now is the time to keep the faith. Take profits on price spikes. Buy the dips. Hold on to your core positions. Oil and gold are currently involved in a normal correction. They have much further to run. We have no doubt about that. The Federal Reserve has announced it has no plans to follow the European Central Bank in raising interest rates any time soon. That decision supports our long-term bullish outlook for gold and oil. We see no signs that the Fed will do anything to reverse its easy money policies. If the economy slows, QE 3 will be the government’s solution. Inflation will be exacerbated by the depreciating U.S. dollar and the understanding that the U.S. plans to foist a weak dollar upon its citizenry…and its creditors. Over our career we have noticed—and research has corroborated—that precious metals and commodity-related stocks move up most rapidly when interest rates are below the inflation rate. For example, if it costs an investor 3 percent interest to buy commodities on margin, and inflation is 4.5 percent, gold and/or other commodities typically rise in price as more investors use these negative real interest rates to protect themselves from oncoming inflation. We highlight an article by John Melloy on CNBC’s web site on April 12, 2011. In his article, Inflation Actually Near 10% Using Older Measure, he states: “After former Federal Reserve Chairman Paul Volcker was appointed in 1979, the consumer price index surged into the double digits, causing the now revered Fed Chief to double the benchmark interest rate in order to break the back of inflation. Using the methodology in place at that time puts the CPI back near those levels. Inflation, using the reporting methodologies in place before 1980, hit an annual rate of 9.6 percent in February, according to the Shadow Government Statistics newsletter. Since 1980, the Bureau of Labor Statistics has changed the way it calculates the CPI in order to account for the substitution of products, improvements in quality (i.e. iPad 2 costing the same as original iPad) and other things. Backing out more methods implemented in 1990 by the BLS still puts inflation at a 5.5 percent rate and getting worse, according to the calculations by the newsletter’s web site, Shadowstats.com…. Our continued kudos and gratitude go out to Jim Sinclair, atwww.jsmineset.com. Jim’s daily commentaries and reports on the unraveling world finance and monetary system have been right on the mark. The public is lucky to have access to someone of his astuteness who patiently explains how and why investors need to protect themselves.

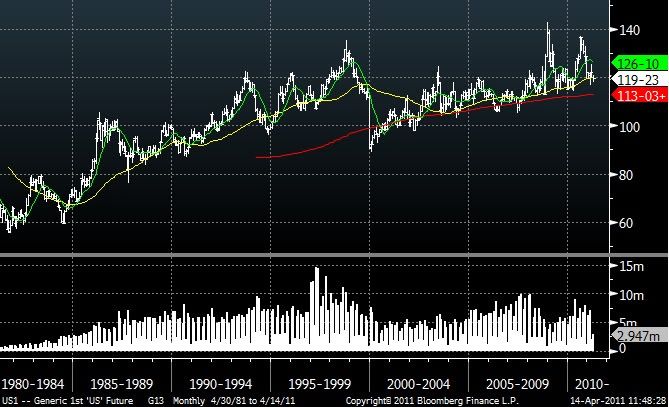

How to Invest for Inflation to Maximize Profits and Protect Assets Inflation is a standard of living destroyer. In the past, citizens could use real estate as a means to fend it off, but this time around the challenge is greater. In the U.S., homes are stuck in the mud, and a lot of mortgages under water. Prices are not going up in the near future for a lot of reasons. Here are some of them: ? the glut of unsold and unpaid-for homes, ? the glut caused by foreclosures of homes bought by people who never really had the capital to begin with, ? a large number of the baby boomers starting to retire and downsizing their living accommodations, ? a new generation of home buyers that is much smaller, and less able to follow in the boomer footsteps and finance those bigger, more expensive homes. It’s worth repeating that the best investments to help combat inflation are, and remain, the same we have been discussing for years: commodities (especially precious metals, oil and food commodities), stocks in inflation-benefitting industries, strong foreign currencies, and strong foreign stock markets. Please see the summary of recommendations below for our currency and country choices. We predict as inflation rises, along with gold, oil, and other stores of value, and the U.S. dollar falls, you’ll also hear the media turning up the volume of negativity. You’ll hear that oil, gold, silver, and other stores of wealth are overpriced, hyped up, that they are a scam, and that when they fall in price the speculators will be punished, etc. You will hear that the rising cost of oil will destroy economic activity. What you’ll be hearing is disinformation similar to the tripe dumped on the public in the 1970s beginning when gold sold for $150 an ounce, on its way from $35 to over $850 an ounce. Investor psychology can create price changes. The battle is now on to control that psychology. The current rising psychology in the global markets is “how do I protect myself from spiraling costs?” When investors in the U.S. and abroad start to widely distrust the U.S. dollar and seek alternatives, the drumbeat from the media and the political spin masters will grow louder about how investing in oil and gold, etc, is bad and even “unpatriotic.” The message was wrong then and will be wrong again. Part of the strategy will be to scare investors away from protecting themselves from the coming inflation. Don’t let them shake you out. Know the negative message is coming. Don’t pay much attention. Stay the course. Expect a Banking Crisis Repeat The big banks have been strengthened by the Dodd-Frank bill, and the too-big-to-fail doctrine is still firmly established. Thankfully, the media has taken notice. After reading a spot-on Bloomberg BusinessWeek article (please click here) you will understand even more clearly what we have been saying about the continued shenanigans by big banks. Unregulated derivatives use has not slowed down, and, in fact, they are becoming even more dangerous than they were before 2008. This is further reason to own gold, oil, foreign currencies and food-related commodities. Oil Check: Hoarding and Gorging on a Grand Scale In 2010, China imported 54 percent of its oil. With the country’s economic output and energy demands clearly rising, the government has announced it will continue to expand its Strategic Petroleum Reserve. We believe China will keep filling its tanks indefinitely, perhaps for another decade. The Chinese will become even bigger oil importers than they are at the present. Continue Avoiding U.S. Bonds — Especially Long Maturities We have been bearish on all types of U.S. bonds for a while, and especially since August 2010. We believe the decline in value since August (even while the Fed has been buying about $4 to $6 billion in treasury bonds per day) is just the beginning. Avoid bonds, especially long-term bonds. Rising inflation will ravage them. The other investment categories we have discussed will trounce bonds as investments going forward. U.S. 30-Year Treasury Bonds

With respect to the undesirability of U.S. bonds, there is going to be a lot of noise coming out of Washington D.C. about the need for federal budget cuts and becoming more fiscally responsible. While U.S. politicians bicker about how to do this, however, they will also be deciding on how much to raise the federal debt ceiling. The rest of the world is not amused and sees this for what it is. On the front page of yesterday’s Financial Times, the International Monetary Fund, who is often called upon to help countries in dire fiscal and economic straits, delivered a slap saying the “U.S. lacks credibility on debt”. Summary of Current Recommendations

|

Uncategorized