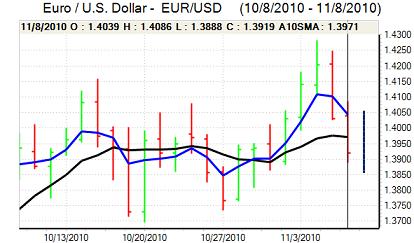

EUR/USD

The Euro has remained under pressure during the past 24 hours with further losses against the US dollar. There was a dip below 1.39 during the Europeans session on Monday and, despite a brief recovery, there were fresh 2-week lows near 1.3850 in Asia on Tuesday.

With no major US economic data due for release, markets were focussed more on the Euro-zone debt problems. There was a further widening of yield spreads during the day as Irish and Portuguese spreads hit record highs and there was a deterioration in Euro sentiment.

The ECB confirmed that it had bought around EUR700mn in Euro-zone bonds the previous week as investor confidence continued to deteriorate. From a medium-term perspective, there were increased fears that new debt-crisis mechanisms would make it more difficult for the ECB to intervene and there were also increased fears that plans for private-sector involvement in bailout plans would further discourage bond inflows.

Regional Fed President Bullard stated that the amount of quantitative easing could be adjusted higher or lower over the next few months and underlying dollar sentiment is still likely to be extremely fragile. Although the dollar has recovered significantly against the Euro over the past few days, there has been very little headway against other major currencies as underlying confidence is still negative.

Source: VantagePoint Intermarket Analysis Software

Call now and you will be provided with FREE recent forecasts

that are up to 86% accurate * 800-732-5407

If you would rather have the recent forecasts sent to you, please go here

Yen

The dollar was again capped below 81.50 against the yen during Monday and drifted weaker to test support below the 81 level with relatively narrow ranges.

The Japanese economic data was broadly in line with expectations as bank lending continued to decline while the current account remained in strong surplus and the overall impact was limited with some yen support from weaker risk appetite.

Finance Minister Noda repeated recent comments that the authorities would take decisive action when required, but the comments had little impact. Market focus on potential intervention has waned, but this could lead to surprise intervention by the central bank. There will also be market caution ahead of G20 meetings later this week and some reduction in long speculative yen positions remains a possibility.

Sterling

Sterling dipped to lows below 1.61 against the dollar during Monday, again primarily as a function of Euro weakness rather than Sterling losses and the UK currency strengthened to a five-week high against the Euro.

The latest housing-sector data was weaker than expected with the RICS survey recording that 49% of agents reported lower prices in October from 36% previously and there will certainly be concerns over a further slowdown which will tend to undermine Sterling confidence.

The latest Bank of England inflation report on Wednesday will be very important for market sentiment. A more optimistic central bank tone on growth and an increase in inflation forecasts would heighten market speculation over a near-term increase in interest rates. Over the past few quarters, the report impact has been consistently negative for the UK currency which may trigger some selling pressure in the run-up to the report and there will be the risk of high volatility.

Sterling was able to find support below 1.61 against the dollar on Tuesday despite the weak housing data with the Euro testing support below 0.86.

Swiss franc

The franc maintained a firm tone on the crosses during Monday with the Euro retreating to test support below 1.34 and the US dollar was again blocked below 0.97 despite a slightly firmer net tone.

The Swiss currency continued to gain support from increased fears over Euro-zone bonds and the risk of further turmoil in the financial sector which would be likely to trigger renewed demand for the franc on defensive grounds.

If the Swiss currency gains further against a basket of currencies, deflation fears within the National Bank could return and official comments will be watched very closely.

Source: VantagePoint Intermarket Analysis Software

Call now and you will be provided with FREE recent forecasts

that are up to 86% accurate * 800-732-5407

If you would rather have the recent forecasts sent to you, please go here

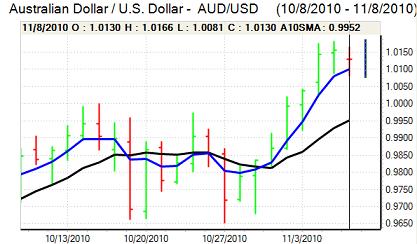

Australian dollar

The Australian currency was blocked close to 1.0150 against the US dollar during Monday and dipped to test support below 1.01 as the US unit recovered, but selling pressure was still measured.

In an international context, the Australian currency drew support from a further rise in gold prices with increased demand for metals as an inflation hedge. The impact was offset by a slightly more cautious attitude towards global risk. Domestically, a small decline in business confidence did not have a major impact with the Australian dollar holding just above 1.01 on Tuesday.