The month of May was an active one for the IPO market. In total, there were 27 deals, surpassing the combined output of March and April, which had 25 deals.

Certainly, the strength in the broader markets has under-pinned the healthy IPO market, but whether that tailwind persists into June remains to be seen. Volatility picked up as the calendar flipped and talk of the Fed tapering its quantitative easing program has rattled the markets.

For now, however, a little uncertainty hasn’t been enough to derail the IPO market as deals continue to flow out of the pipeline.

LIGHTINTHEBOX (LITB) WILL TEST THE WATERS

It seems a bit strange now looking back, but, back in 2010 and early 2011, Chinese IPOs were the hottest commodities around. In fact, in 2010, there were a whopping 40 Chinese IPOs, accounting for more than a quarter of the total number of IPOs that year.

It has dried up dramatically since then, but following YY Inc’s (YY) successful IPO, and the recent strength in Chinese stocks, LightIntheBox (LITB) will look to take advantage of the improved environment for China-based IPOs.

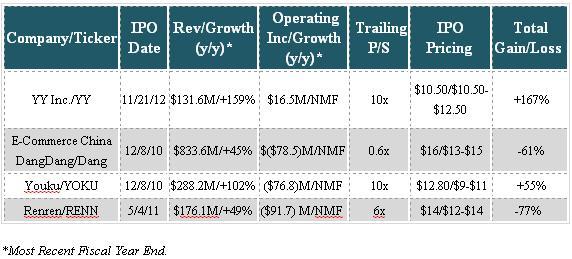

Below is a closer look at how YY, and a few other recent China-based IPOs have been performing:

THE DEAL AND THE BUSINESS

On June 5, LITB will offer 8.3 million ADSs, with each ADS representing two ordinary shares. Following the IPO, there will be 97.9 million ordinary shares outstanding, which would give it a market cap of $465.1 million, assuming the deal prices at the mid-point. The underwriters are Credit Suisse and Stifel Nicolaus Weisel.

LITB is a China-based e-commerce company that sells a wide selection of lifestyle products at low prices through its various websites. These products range from electronics, to apparel, to home and garden items, to jewelry, and many others.

Its largest markets are Europe and North America and it uses marketing platforms such as Google and Facebook to reach its consumers. It acquires new customers exclusively through the internet, and has established a specialized social media marketing team that uses interactive activities to engage online users.

FINANCIALS

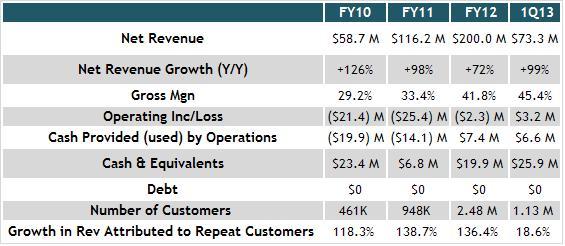

LITB’s financials are impressive. In FY12 and 1Q13, revenue soared by 72% and 99%, to $200 million and $73.3 million, respectively. Furthermore, gross margin has been expanding nicely over the past few years, going from 29.2% in FY10 to 41.8% in FY12. The bump here is attributable to its cost of goods sold, as a percentage of revenue, dropping sharply to 58% last year from 66.6% in FY11, and 70.8% in FY10. LITB has been focusing on the sale of higher margin products.

There are some blemishes and perhaps a red flag, though. The company has a track record of losses, as it has yet to report operating profit on a full year basis. In FY12 it had a net loss of ($4.2) million, a big improvement from the ($24.5) million loss from a year earlier, but still in the red nonetheless.

The potential red flag is its growth in revenue attributed to repeat customers. In 1Q13, this was at 18.6%, down from 20.3% in the year ago period. We wouldn’t characterize it as a major concern at this point, but given that one of our concerns is that there is plenty of negative customer feedback (a simple Google search illustrates that), we felt it was worth highlighting and worth watching going forward.

CONCLUSION

It will be interesting to see how LITB prices and performs out of the gate. A solid pricing, especially in the footsteps of YY’s successful IPO, could be a green light for more Chinese IPOs down the road. Its strong financials and growth rates support a strong showing, but unfortunately, there are a couple hiccups.

For instance, LITB disclosed a material weakness in its internal control over financial reporting. This material weakness relates to the lack of sufficient accounting personnel for financial information processing and reporting with appropriate U.S. GAAP knowledge. This is not uncommon for foreign IPOs, but given that there already is a high degree of unease and skepticism, it would be highly preferable if this issue was taken care of prior to the IPO.

Additionally, if a Google search is done on LITB, one of the more prevalent items to pop up is customer complaints about receiving bad products, or products that didn’t match the website. Again, not very encouraging considering the past unease surrounding these IPOs.

With all of this in mind, we would sum it up this way: LITB is a very high risk proposition, and it’s questionable whether the risks are worth the potential rewards. For investors with a very high tolerance for risk, a case could be made to take a position, assuming it prices and opens for trading at reasonable levels. But, passing on this deal and waiting for a higher quality, U.S. based IPO to come through the pipeline sounds like a reasonable approach for many investors.