EUR/USD

The Euro hit resistance above 1.33 in Europe on Thursday and then weakened steadily during the day with a test of support below 1.32 in New York trading.

The Euro-zone debt-market developments remained a key focus as markets continued to fret over medium-term vulnerabilities. Ratings agency Fitch downgraded Ireland’s bond rating by a further three notches as debt costs continue to spiral higher. Confidence surrounding Ireland remains extremely weak and a key problem for the Euro is that uncertainty will persist with the Irish parliament still debating the budget and a vote on whether to approve the aid package is due to be held next week.

There will be continued speculation over additional measures to support weaker Euro-zone members with further debate surrounding possible Euro-bond issuance, although these plans appears to have been rejected by Germany. Discussions will continue ahead of the EU summit due to be held at the end of next week and the Euro will be vulnerable to further selling pressure if there are public disagreements over plans.

The latest US jobless claims data was better than expected with a decline to 421,000 in the latest week from a revised 438,000 and overall confidence in the economy is likely to remain slightly higher which will provide some dollar support. This backing will be tempered by speculation that the Federal Reserve will look to push Treasury yields lower.

The Euro retreated to lows just above 1.3150 before regaining the 1.32 level and pushing higher in Asian trading on Friday.

Source: VantagePoint Intermarket Analysis Software

Call now and you will be provided with FREE recent forecasts

that are up to 86% accurate * 800-732-5407

If you would rather have the recent forecasts sent to you, please go here

Yen

The dollar hit resistance closer to 84.20 against the yen on Thursday and edged weaker with a test of support near 83.50 where solid US currency support emerged following the US jobless claims data.

There will be further speculation over a possible Chinese move to increase interest rates over the weekend, especially with key economic data release dates brought forward to Saturday and this is likely to provide some near-term yen support. If there is no Chinese move to raise rates then the yen would be vulnerable to selling pressure when Asian markets open on Monday.

Domestically, there was a deterioration in fourth-quarter business confidence according to the latest Bank of Japan survey while consumer confidence weakened. There will be persistent unease over Japanese growth trends which will maintain pressure for yen gains to be resisted with the dollar holding above 83.50 on Friday.

Sterling

Sterling hit resistance above 1.5820 against the US dollar on Thursday and retreated sharply during the US session with lows close to 1.57 before a recovery.

As expected, the Bank of England left interest rates unchanged at 0.50% following the latest MPC meeting and the quantitative easing total was also held steady at GBP200bn. There was no statement and details of the discussion including the vote split will not be known for 2 weeks. Public comments from MPC members will continue to be watched very closely in the near term.

The latest trade data was again disappointing with the goods-related deficit rising to GBP8.5bn for October from a revised GBP8.4bn previously and this will dampen hopes for a sustained export-led recovery.

Sterling will continue to gain some net protection from fears over the Euro-zone outlook and the Euro was drifting just below 0.84 in early Europe on Friday.

Swiss franc

The franc maintained a firm tone against the Euro on Thursday and tested support below 1.30 before finding some respite. The tone of franc strength on the crosses capped dollar gains to near the 0.99 level before a retreat to 0.9825 during Asian trading on Friday.

The Swiss currency will continue to gain defensive support from a lack of confidence in the Euro-zone with the potential for capital flight away from Euro-related assets.

There will be caution ahead of the National Bank’s quarterly monetary policy meeting next week as the bank could signal its opposition to further franc gains. Volatility will remain an important risk surrounding the meeting.

Source: VantagePoint Intermarket Analysis Software

Call now and you will be provided with FREE recent forecasts

that are up to 86% accurate * 800-732-5407

If you would rather have the recent forecasts sent to you, please go here

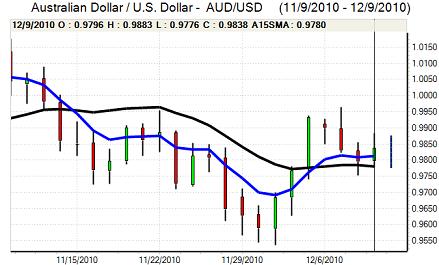

Australian dollar

The Australian dollar pushed to highs near 0.9870 against the US dollar during Thursday and proved resilient over the remainder of the day with support near 0.98 holding even when there were sharp Euro losses. There was further support from the stronger than expected employment data and comments from Reserve Bank officials will be watched closely next week to assess policy intentions.

The Australian currency drew some support from a higher than expected Chinese trade surplus and metals prices rose during the Asian session, but there was still caution given the possibility of a Chinese interest rate increase.