The BOJ is continuing their QE, but will also now be targeting a zero yield on 10-year bonds (they were negative before). They want to steepen the curve.The latest FED and BOJ meeting were no surprise. Yellen and Kuroda did exactly what everyone thought they would.

The Fed held rates steady, but claim they plan to hike before the end of the year (ie, December), emphasizing they really mean it this time.

US markets rocketed higher with small-caps leading the advance while the dollar sold off. The next few months should be pretty lucrative for agile macro traders.

Here’s some quick takeaways:

The BOJ wants a steeper yield curve to help banks. The larger the spread between the 10 and 2yr of Japanese bonds, the more profits for the financial sector who was struggling with negative rates.

This move is basically a tacit acknowledgement that NIRP is deflationary. This is why we’re seeing negative yielding currencies strengthen because steepening the yield curve is a form of stealth tightening. We should expect the ECB and SNB to follow suite in the months ahead. This is why I expect the dollar to weaken in the near-term as markets wake up to this fact.

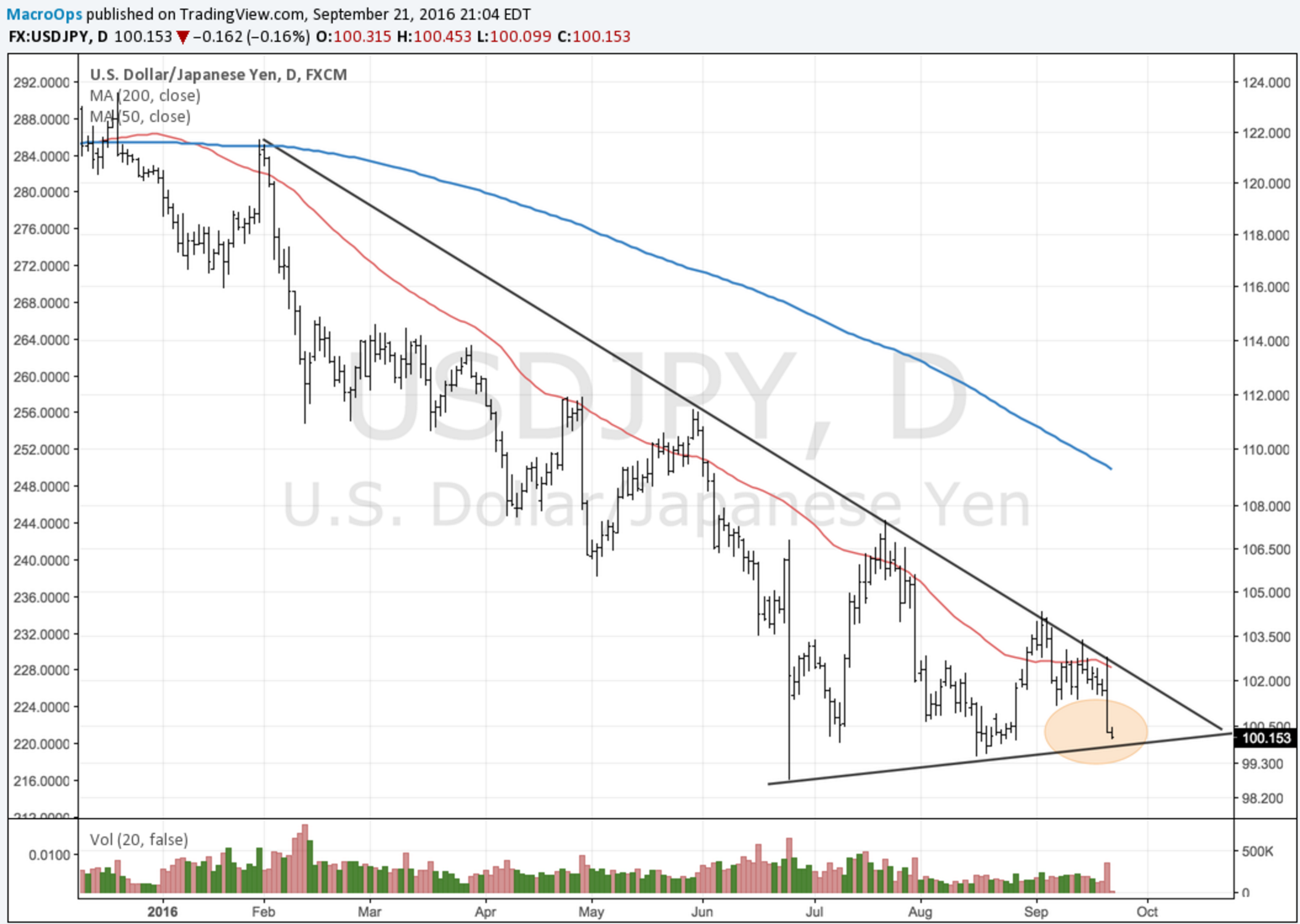

The USDJPY cross is nearing a critical juncture. USDJPY falls when the dollar weakens and the yen strengthens. It experienced a strong reversal after the BOJ’s announcement and is now dangerously close to breaking its lower support… this is exactly what BOJ chairman Kuroda doesn’t want to see

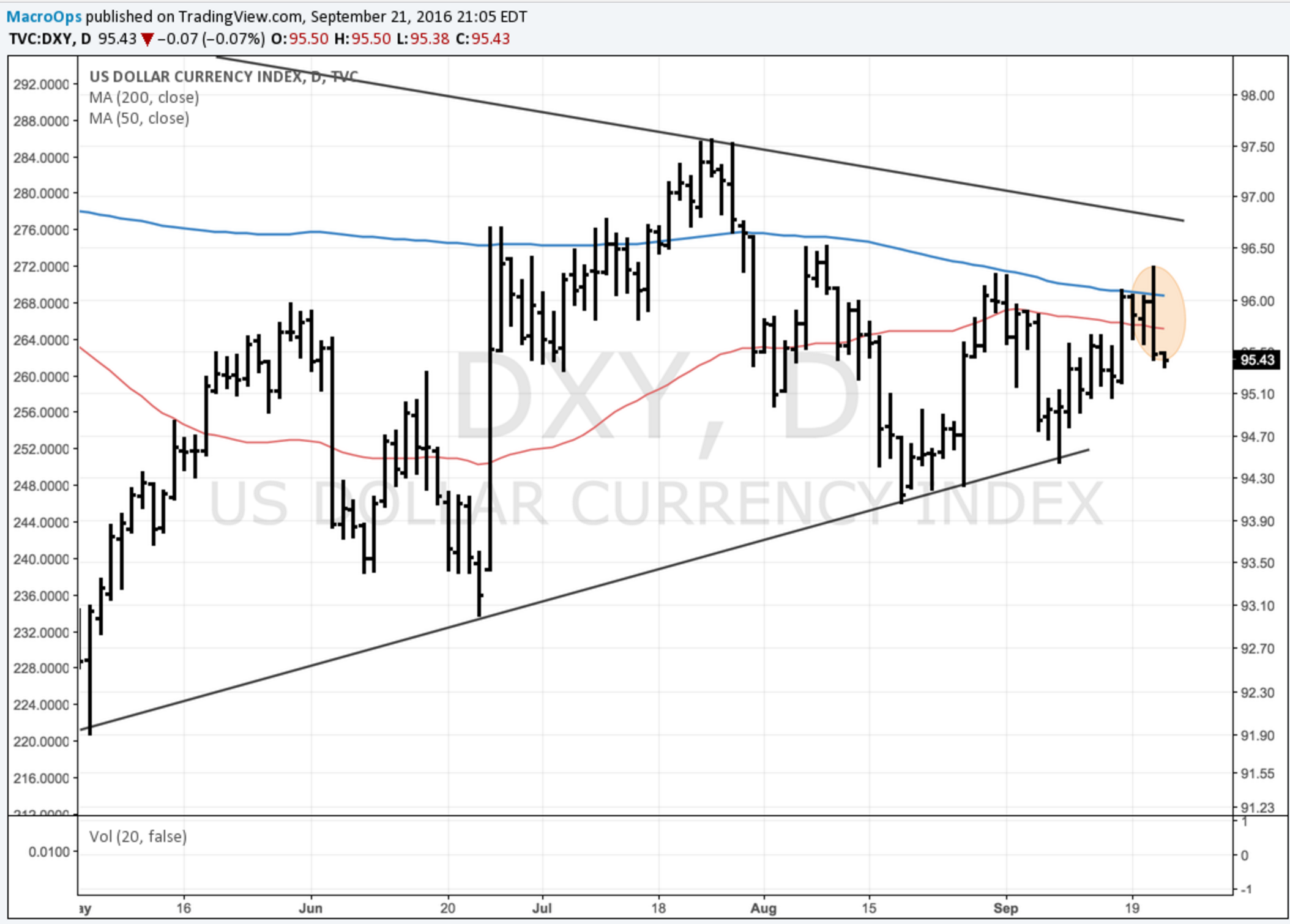

The dollar index reversed yesterday after the Fed’s announcement. If it breaks its lower trendline then I would expect a fast and sizable move lower as a weaker dollar would catch many traders, especially fund managers, off guard. If there’s a break, we’ll take a swing at a long AUDUSD trade

Gold and miners rallied off the dollar weakness. If the dollar pukes I’d expect gold to rally further. A long gold trade could be profitable if price breaks above its upper trendline.

The dollar index reversed yesterday after the Fed’s announcement. If it breaks its lower trendline then I would expect a fast and sizable move lower as a weaker dollar would catch many traders, especially fund managers, off guard. If there’s a break, we’ll take a swing at a long AUDUSD trade.

Same story in crude and energy stocks; both rallied off a weaker dollar. If the dollar stays soft we’ll see crude breakout to the upside of its current wedge and run higher.

At the meeting, the Fed lowered its growth forecasts for the economy while at the same time promising a rate hike before the end of the year. Makes sense right?

Central banks are reaching the point where the markets are caring less for their words and will only respond to actions… they’re losing their credibility.

The threat of raising rates is just part of their strategy to keep markets in check. Fed President Bullard laid this out in an interview with the WSJ’s Hilsenrath last month:

Hilsenrath: What kind of compromise would it take to get the FOMC to move in September? I mean, so the tradition is there’s some kind of — like you say, some kind of agreement. What would it take to get them there?

Bullard: Well, I have no idea, so — and it’s really — it’s really the chair’s job to fashion that. But I will say that — I’ll talk historically about the FOMC, the kinds of things that the FOMC would do. You would trade off. You would say, OK, we could hike today, but then we’ll not plan to do anything in the future. That would be one way to — one way to go about a consensus. So that often happens on the FOMC. Or vice versa. If you read the Greenspan-era transcripts, he’ll do things like, OK, we won’t go today, but we’ll kind of hint that we’re pretty sure we’re going to go next time.

Hilsenrath: Right.

Bullard: And so you get this inter-tempo kind of trade-off, and that often — that often is enough to get people to sign up.

Hilsenrath: So, hike today and then delay.

Bullard: Yeah. (Laughs.)

Hilsenrath: Or, no hike today and then no more delay.

Bullard: Yeah, yeah.

Hilsenrath: Something like that.

Bullard: Yeah, those kinds of trade-offs are, historically speaking — I’m not saying I know what Janet’s doing, because I don’t. But, historically speaking, those are the kinds of things that the FOMC has done.

Hilsenrath: I came up with my catchphrase for the — for the month. (Laughter.)

Bullard: Those are great. That’s worthy of a T-shirt. (Laughs, laughter.) You could have one on the front and one on the back.

Torry: Or a headline.

Hilsenrath: Well, that’s the St. Louis framework now, right?

Bullard: Yeah.

Hilsenrath: Hike today and then delay.

Bullard: Yeah. That’s what it would be, yeah.

“No hike today and then no more delay”, that’s the spin we’re seeing from the Fed. We should give markets the rest of this week to digest this news. Price action is extremely unreliable during Fed weeks, so it’s best to sit on the sideline and watch.

If there’s some decisive moves at the end of the week then we’ll start adding more risk to our books. I think we’ll see a period of risk-on for US equities into the end of the year, with small-caps and biotechs leading the way. I expect European and Japanese stocks to underperform the US. I also think the dollar will weaken in the short-term, which will drive gold and energy stocks higher while keeping emerging markets buoyant.

The last quarter of this year is going to be a good one for macro traders who stay on their toes.

For more information about how we’ll be taking advantage of this environment, please click here.