Gold rose to a new two-week high in early U.S. trading Wednesday amid rising expectations of additional central bank stimulus. The yellow metal got a further boost from a bigger than expected rise in U.S. import prices, which jumped 1.1% in February.

The rise in import prices was the largest in six months, driven by rising petroleum prices. Prices were unchanged in February ex-petroleum. Nonetheless, with the Fed pumping $85 billion in new money into the system each and every month, there are many investors out there looking for any signs of inflation. Gold of course is the classic hedge against price risks.

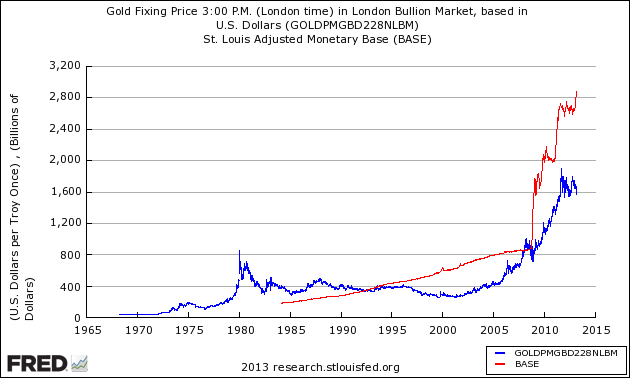

In USAGOLD’s latest newsletter, Michael J. Kosares notes how gold correlates to the monetary base, pointing out the sharp 8% rise in base money since the beginning of the year, courtesy of the Fed’s QE4 program.

Kosares: “Gold, as the chart illustrates, closely tracks but lags the monetary base. If nothing else, the extensive and on-going creation of money (whether or not it translates to double-digit price inflation) suggests that the Federal Reserve remains in crisis mode and that there might be volcanic risks in the banking and credit system rumbling just below the surface.”

KEY POINT

Pay particular attention to that “lag,” as gold has yet to react to the latest surge in the monetary base. With the low end of the year-plus range holding, the yellow metal may be staging for its next run at the upside.

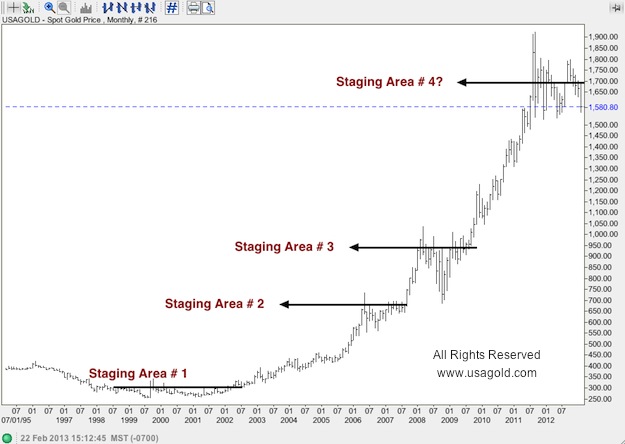

[Editor’s note: Check out this special report on Gold chart staging areas.]

INTERESTING CENTRAL BANK SHIFTS

Beyond easy monetary policy, central bank demand for gold is another key underpinning for the market. The World Gold Council released a report today that highlights some pretty interesting shifts in central banks reserves.

BIG JUMP IN GOLD RESERVES

WGC: “The official reserves of global central banks have grown from $2 trillion in 2000 to more than $12 trillion in 2012. During this same twelve-year period the data shows significant shifts away from the US dollar while the share of “other” currencies in reserve composition has tripled in absolute terms since 2008.”

Of particular interest for our readers is the ongoing move out of dollars and the increased appetite for gold. In February, the WGC reported that central banks added 534.6 tonnes of gold to reserves in 2012, the most since 1964.

In the latest report, Ashish Bhatia, Manager for Government Affairs at the World Gold Council makes a couple key observations about gold:

“Building gold reserves in tandem with new alternatives is an optimal strategy as central banks remain under-allocated to gold and many attractive alternatives are either too small or, as is the case with the renminbi, not yet open to broader international participation.

“Gold has a deep and liquid market with no credit risk, making it one of the most attractive assets for central banks to consider as they diversify away from the US dollar and euro. Gold’s tail-risk hedging properties add to its appeal as a particularly valuable component of a diversified reserve portfolio.”

BOTTOM LINE

The individual investor too is arguably under allocated to gold and could greatly benefit from diversification into the yellow metal. The same motivators behind the central banks’ moves to diversify out of dollars and into gold are equally applicable to those individual investors.