“Patent expirations” are the two words most commonly used to dissuade investors from investing in pharmaceutical stocks. With respect to Pfizer specifically, 20% of its revenues are expected to be significantly affected by the loss of patent on flagship cholesterol drug Lipitor. But the market’s pessimism combined with some changes at the company may result in extraordinary gains for long-term shareholders at the current price.

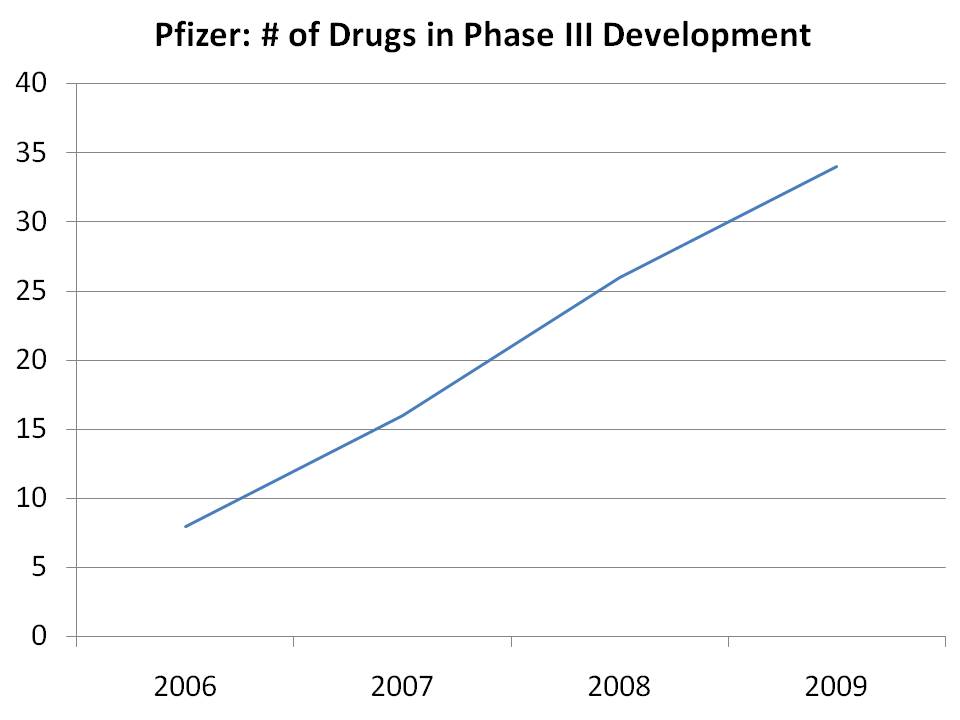

While patent expiries on existing drugs will continue to spook investors as long as Pfizer has drugs worth selling, it would be naive to expect that Pfizer will not be able to replace some or all of these drugs with new ones. The company has been working hard for many years to improve its pipeline, having spent around $8 billion per year on R&D efforts. The results may be starting to show, as the number of drugs Pfizer is able and willing to take to Phase III trials has been growing steadily as follows:

Of course, such a chart does not give a complete picture of the future, as many drugs will fail their trials, and the potential market size of each drug is not illustrated, but these results are certainly encouraging on their own. CEO Jeff Kindler, who has been with Pfizer for 9 years, noted in the company’s last conference call that “[W]e are more enthusiastic about our late stage pipeline than we have been in years.”

Of course, such comments from CEOs must be taken with a grain of salt, as managements have incentives to boost confidence in their own company’s stock. But an analysis of Kindler’s previous statements over the years suggests this comment may be genuine. Pfizer’s average return on equity over the last five years of 13% also confirms that management is not reckless with its investments, and is prudent with capital allocation decisions.

In previous years, Pfizer has managed to generate these strong returns even while holding a relatively large net cash position. With the acquisition of Wyeth a couple of quarters ago, however, the company is now employing all of its shareholder capital – and then some. The company now has a net debt position of $20 billion, compared to a net cash position of $8 billion at this time last year. As a result of this swing, the company now has almost $30 billion of additional earning assets. The acquisition of Wyeth also adds steadier products such as Advil, Robitussin and ChapStick to Pfizer’s portfolio, which mitigates the risk that accompanies larger debt balances.

From a valuation point of view, the pessimism surrounding this company has made it look cheap. Management estimates earnings per share of approximately $2.30 in 2012, versus a current stock price of $16. Investors should note, however, that management’s numbers are significantly higher than the GAAP numbers, as management likes to report a number that excludes various items; shareholders should ensure they understand these differences, as

non-recurring charges in this industry tend to be the norm rather than the exception.

When we met with value investor Francis Chou almost two years ago, he was bullish on the pharmaceutical sector as a long-term value investment. Since that time, valuations for many of the large pharma companies (Pfizer included) are down, while changes in companies like Pfizer are likely to have a positive effect on future earnings. As the market continues to be pessimistic on this sector due to upcoming patent expirations, much of the downside risk is already priced in. At this price level, companies like Pfizer could offer superior long-term returns.

Disclosure: None