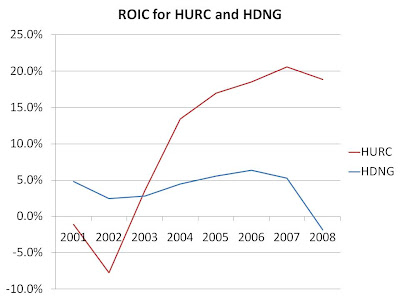

Hardinge (HDNG) and Hurco (HURC) both design and manufacture computerized machine tools. During downturns, one of the most common decisions undertaken by companies looking to preserve capital is cutting capital expenditures. As such, both of these companies operate in very cyclical industries and therefore do not carry much debt. While these companies have some important differences between them, their approximate returns on invested capital are compared below to illustrate a point:

In the last several years, HURC has managed to generate solid returns while HDNG has struggled even during periods of relatively strong macroeconomic growth. Over the period displayed above, HDNG returned an average of 3.7% on its invested capital while HURC returned an average of 10.4%, meaning HURC was able to generate more income out of its assets.

While HURC appears to be the better run company, which one is the better investment? “Buy best of breed companies” is the oft-repeated investing mantra that many investors blindly follow. But what this advice fails to take into consideration is the asking price: while HURC trades for its book value, HDNG trades at about a 60% discount to its book value. Therefore, if the businesses perform the same as they have in the past, buyers of HDNG will see similar returns on their investments as will buyers of HURC, thanks to the discount being offered on HDNG’s book value.

But what if returns are not the same? HDNG has recently taken on new management following its poor performance and is in the process of attempting to improve its cost structure. Should the company increase efficiencies such that returns on capital return to respectable levels, shareholders should see enormous price appreciation as the current discount is erased. But what if returns should fall? Fortunately, at this price, investors are protected by the company’s cash, inventory and accounts receivable, which sum to a level higher than the current stock price, even after subtracting all liabilities.

Neither company will likely see its sales levels grow for some time, as their customers continue to cut expenditures to boost their bottom lines. But from a business value standpoint, one company does appear to offer an enticing price to long-term investors, even though it has been a poor performer. But investors needn’t bet on a turnaround, as the discount to book already offers investors the prospects of decent returns, while a margin of safety exists such that capital appears to be relatively safe. We have previously seen another example of this phenomenon as Office Depot traded at a massive discount while best-of-breed Staples maintained a fair price level.

Disclosure: Author has a long position in shares of HDNG