The cash-and-carry model is probably one of the most important concepts futures traders should understand in order to correctly value futures contracts and decide which strategies to pursue. It can tell you if you will be accumulating, or paying out, carry to hold a position. This concept is applicable to most financial markets as well as gold, but is particularly suitable for the currency markets. I will outline some current trading strategies to consider.

One of the biggest mistakes new traders make is that they believe futures contracts are predictors of future expected price. That’s not always true. Futures prices have a clear mathematical relationship to the corresponding spot (cash market) price, determined by interest rates, and the cost of storage (carry) for that particular commodity.

Arbitrage

Arbitrage is the first concept to understand when talking about the cash-and-carry model. The arbitrage trader is essentially in the middle of a transaction between buyer and seller. Any time the arbitrage trader is able to find a commodity for sale at a better price than is available to another trader, he or she steps in the middle and takes a risk-free profit. For example, trader A is selling commodity X for $10 per unit, while trader B is willing to buy commodity X for $12 per unit. These traders don’t know each other, but the arbitrage trader is aware of both and the price differential, steps in and collects the $2 difference as profit.

Arbitrage can take the form of a variety of different strategies. Cash-and-carry arbitrage involves buying a commodity in cash form, holding it, and delivering it into a futures contract with the goal of taking a profit through that cycle.

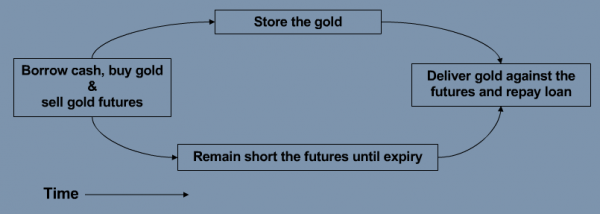

Cash and Carry Arbitrage – Example

Price of gold in the physical market for immediate delivery $1,050/oz

Price of gold in futures market for delivery in one year $1,060/oz

Differential $10

In this example, the futures contract one year from now is trading $10 above the spot price. That differential may be too much. If that’s the case, traders will engage in cash- and-carry arbitrage. These traders go into the physical market, borrow cash to purchase gold, put it in a vault and store it, then at the same time, sell gold futures. If the cost of doing that is less than $10, the trader will have captured a risk-free profit through arbitrage, and has a neutral exposure to the market.

If it’s possible to collect a profit from this enterprise, that creates buying in the physical market, and selling in the futures market. That creates a high barrier for futures prices. If traders expect a year from now gold will be much higher (say $1,300) we don’t see that reflected in the futures prices, because the cash-and-carry model holds very well for this market.

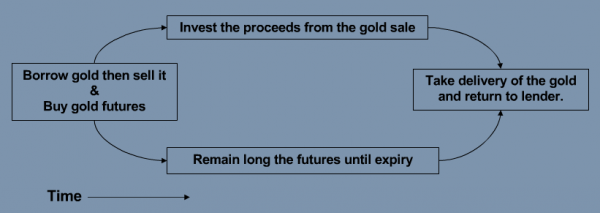

Reverse Cash and Carry Arbitrage – Example

Price of gold in the physical market for immediate delivery $1,050/oz

Price of gold in futures market for delivery in one year $1,040/oz

Differential ($10)

Reverse cash-and-carry arbitrage is the exact opposite, but it only works for commodities that can be borrowed. You might not realize that investors can borrow gold by leasing it from central banks or metals dealers, for a rather inexpensive rate.

In the reverse cash-and-carry, the trader would borrow gold, sell it into the market and generate cash, then buy gold futures contracts. Again, there is no market exposure, but the physical gold the trader sold is owed back to where it’s been leased from. The trader has secured a future purchase of gold with the futures market long position. Then he or she invests the proceeds of the cash in risk-free interest rate products, and remains long the futures until expiry. The trader then takes delivery of the gold futures, and returns the gold back to the lender. This creates a low barrier for futures prices. The selling in the physical market pushes the spot price down, and the buying of futures pushes those prices upward.

These two barriers, the high and low barrier, can combine, and create a band, known as the cost of carry. It is essentially the cost of leverage. If you are looking to buy gold and hold it for a year, there may be a cost, that $10 in our prior example. That’s the cost of borrowing the cash had you been able to purchase the entire amount of physical gold and hold it. Any time a futures market moves outside the band, arbitrage occurs and pushes prices inside the band.

There are a few conditions needed for the cash-and-carry model to work.

- The commodity must be able to be borrowed. Some commodities, such as grains, can’t be easily borrowed.

- The commodity must be storable. Not all commodities are easily stored. Natural gas is very expensive to store as it has to be compressed, and livestock are difficult to store.

- Must not decay with time.

If any of these three conditions fail to hold, then you see a situation where futures prices may in fact represent future cash market price expectations. For example, if the price of corn futures is higher for a corn contract a year from now, that likely reflects expectations the spot price will increase in a year. That’s not necessarily the case for gold or most financial futures, which can be borrowed and are storable. In assets that follow the outlined conditions, the cost-of-carry model holds very well.

Currency Carry Trades

Currency futures offer excellent carry trading opportunities. Anyone who has been following the financial markets has probably heard of the Japanese yen carry trade. That occurred when traders were borrowing yen at Japanese interest rates, then converting into U.S. dollars to invest in higher-yielding U.S. assets. That occurred when U.S .interest rates where much higher than yen interest rates (which is no longer the case). That caused the yen to fall, and traders and hedge funds made tremendous amounts of money capturing the interest rate differential between the countries.

Futures contracts make this process easy to do. Whenever you have an interest rate differential between two currencies, there is an opportunity for a carry trade, although of course it’s not necessary always profitable. Because the cost of carry holds, the futures prices represent the interest rate differential between the two currencies.

A good example of a carry trade opportunity right now is the Australian dollar. The Reserve bank of Australia has been leading the way in raising interest rates. Last month it raised their key short-term lending rate 25 basis points to 3.25, and raised them again the first week in November to 3.50 percent. Policymakers have made it clear they are going to be aggressive and hawkish in making sure their economy doesn’t accelerate too quickly out of recession, resulting in an inflationary trap.

The U.S. Federal Reserve has left interest rates at 0.25 percent, and Fed policymakers have implied that they will likely remain at that level until into 2010. This creates a 3.25 percent differential between the two currencies. Comparing prices of Australian dollar futures, we can see the 2009 contract and 2010 contract are roughly 4.25 percent different. The futures markets are pretty smart; that differential is already worked into the price. Traders recognize that if the Reserve Bank of Australia continues to raise rates, it won’t take long before the interest rate differential hits 4.25 percent, so you can see that rate built into the futures price.

Australian Dollar Futures

Settlement Diff from Dec Diff fro Dec %

Dec 09 89.790

Mar 10 88.910 -0.880 -0.98%

Jun 10 87.940 -1.850 -2.06%

Sep 10 86.960 -2.830 -3.15%

Dec 10 85.970 -3.820 -4.25%

If you believe the Australian dollar will head higher for whatever reason–because it’s a commodity-based currency, their economy has weathered the recession better than the U.S., and/or the U.S. dollar should remain weak–you might want to purchase Australian dollar futures. These futures make available a 4.25 percent additional return on the total value of the contract, so the carry is already priced in.

If you buy a December 2010 futures contract at 85.97 and the spot price of Australian dollars doesn’t move, eventually that 85.97 will climb to 89.79. Those prices will merge and you gain the 4.25 percent differential. A lot of traders are already engaging in carry trades in the Australian dollar, pushing up the value of the currency.

Brazilian Real Futures

Settlement Diff From Dec Diff from Dec %

Dec 09 56.44

Mar 10 55.155 -1.290 -2.29%

Jun 10 54.110 -2.335 -4.14%

Sep 10 53.010 -3.435 -6.90%

The Brazilian Selec interest rate target is 8.75 percent. You could capture that differential from the U.S. rate by buying Brazilian real futures, and collecting the carry. When trading futures, keep in mind that you have to get the direction of the market right, as well as the interest rate differential.

I think both Australian dollar and Brazilian real futures have good bullish fundamental arguments going for them, so these strategies should represent good opportunities for traders. Commodity based currencies did poorly when commodity prices dropped, but as economies heat up again, commodities have rebounded, and that’s reflected in the price of both of these currencies.

If you would like more details on specific trading strategy, or have any other questions about the futures markets in general, please feel free to contact me.

Aaron Fennell is a Senior Market Strategist and Chartered Financial Analyst based in Toronto with Lind-Waldock, a division of MF Global Canada Co. He is accepting clients from Canada and can be reached at either 877-840-5333 or 416-369-7933, or via email at afennell@lind-waldock.com.

The data and comments provided above are for information purposes only and must not be construed as an indication or guarantee of any kind of what the future performance of the concerned markets will be. While the information in this publication cannot be guaranteed, it was obtained from sources believed to be reliable. Futures and Forex trading involves a substantial risk of loss and is not suitable for all investors. Past performance is not indicative of future results. Please carefully consider your financial condition prior to making any investments. Not to be construed as solicitation.

©2009 MF Global Ltd. Lind-Waldock, a division of MF Global Canada Co. Toll-free 877-501-5463. MF Global Canada Co. is a member of the Canadian Investor Protection Fund.

Futures Brokers, Commodity Brokers and Online Futures Trading.

123 Front St. West, Suite 1601, Toronto, Ontario M5J 2M2