By: Lee Vecchione

We are forecasting that unprecedented government intervention will support markets throughout 2010 as policy makers continue to push the limits of the current liquidity cycle; however, in 2011 and beyond this shock to the system will fade and the stark reality of the challenges facing the United States will be in the clear and present.

From a technical perspective, this is a cyclical bull market within a secular bear and should run its course by early 2011. That is in confluence with the charts as the SPX and DJIA both have ominous patterns that are pointing to significant price declines in the 2011-2013 timeframe. In addition, we believe that Treasury bond yields reached a secular low in 2009, which is confirmed by the head and shoulders pattern that has formed on both the TLT (20+ Year) and the IEF (10+ Year).

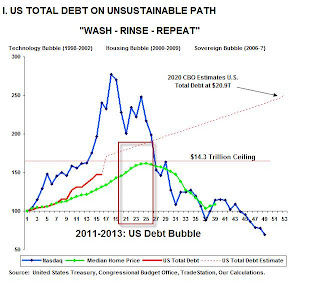

From an economic perspective, the U.S. government is on an unsustainable course with the country’s total debt forecasted to be $20.9 Trillion in 2020. We are of the belief that there has been an awakening of the populous and deficit reduction will be the topic de jour going into the 2012 presidential election. There are only two ways to reduce the deficit in the short term and that is to either cut spending or raise taxes – both which lead to a lower standard of living and place a drag on economic growth. In the near term, we expect GDP to roll back to an anemic rate with the potential to turn negative as the inventory cycle plays through.

On an individual level, consumers are currently in a balance sheet recession and deleveraging as they purge the past 20 years of a credit binge. We see the personal savings rate rising to 6% and stabilizing in the next 1-3 years, casting headwinds and reshaping the world’s dependence upon the voracious appetite of the U.S. consumer. In addition, we see jobs as hard to come by and the social safety net cast about as wide as it can, causing individuals to roll off into the abyss, and posing major implications for society as a whole.

The core issue of the crisis has not completely abated with data pointing to a continuation in weak housing fundamentals – mortgage rates to increase, shadow inventory to overhang weak demand, tax credit incentive to expire, and foreclosures still to peak. This combination leads us to believe that housing prices, while close, have yet to find a bottom.

There is also an impending wave of commercial mortgage resets on the horizon, with the peak in 2013. According to the Congressional Oversight Panel, over 2900 regional banks could be at risk as 50% of the loans made on these properties are underwater. We feel that the markets and main stream media are neglecting the potential severity of this window and will not pick up on it until the process is already underway and worthy of a headline.

Lastly, on a matter of transparency, ethics and the overall confidence in financial reporting, we highlight how industry and government, in opposition of investors and regulators, relaxed the rules on FAS 157, mark-to-market accounting. All we can say is that the passage of time will always unearth true valuations.