Florida’s Deep Freeze drew plenty of media attention. But real opportunities often come after the spotlight has faded.

Frozen Orange Juice futures may sound like the poster child for exotic, “Vegas style” investing to the uninitiated mainstream investor. However, to the old school commodities traders, FCOJ is held as a tasty little secret. For unlike trading stocks, gold, or even crude oil, Orange Juice prices are nearly always a pure fundamental play. And there are very few fundamentals to follow for Orange Juice. Supply comes from a few key areas. Demand is somewhat easy to measure. Fund participation is limited. This can make price forecasting for Juice a fundamentalist’s utopia.

The exception to this is when an outside event such as weather brings new speculators into the market, driving prices away from their supply/demand fair price. This is where opportunities can be created.

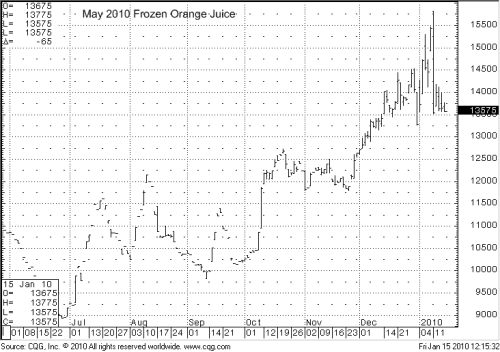

When we advised waiting for increased volatility last month to sell FCOJ (Frozen Concentrate Orange Juice) options, we never expected the magnitude of volatility that came in early January. Last week’s record cold temperatures in central Florida Orange growing regions cast a shadow of doubt over next year’s Orange harvest. This brought a torrent of media coverage which in turn attracted waves ofspeculators into the market, spiking prices.

As with many spec led rallies, the market priced in a worst case scenario before the frost had even evaporated. Thus, when a worst case scenario did not materialize, speculators (read general public) exited en masse.

While this type of price movement can be exciting for high speed traders, I get paid to make the dull money. And now that the general public has lost their money, it may be time to seek the legitimate opportunity.

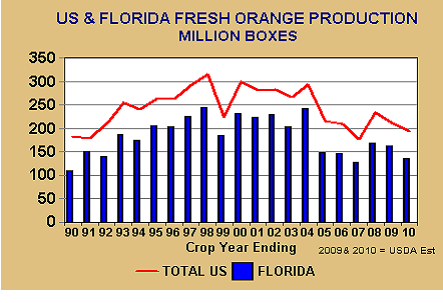

Florida oranges make up close to half of all oranges used to satisfy the FCOJ (Orange Juice) contracts at the ICE. This makes prices on the ICE extremely sensitive to developments in the Florida crop.

Florida Orange production was already the second lowest in 20 years before the freezing weather.

At an estimated 135 million boxes, Florida’s 2009/2010 Orange crop is already pegged to be the second lowest in twenty years and 17% smaller than last year. This smaller incoming crop makes prices even more sensitive to further reductions. While the Florida harvest is already underway, the bulk of the crop has yet to be picked.

Oranges are damaged when temperatures fall below 28 degrees for four hours or more. The longer the exposure at these temperatures, the greater the damage.

Growers, however, have their own defenses against freezing temperatures. One is “accelerated” harvest. This simply means the growers bring in as many workers as possible to pick as many harvest ready oranges as possible ahead of, and/or during the freeze. The other is irrigation. Sprinkler systems are turned on to cover the trees and fruit in a layer of ice. The ice actually protects the fruit from the colder temperatures outside.

Watering was so heavy last week in certain parts of Florida that certain areas were ordered to stop or risk draining wells.

It is clear that temperatures in several growing areas dipped below these temperatures for varying amounts of time. The extent of Florida farmers’ success against Mother Nature has yet to be determined. Unclear is how much real damage was done to the Florida orange crop or how much or little the final yield figures will be effected. Despite the media coverage of the event, and grower assurances that the bulk of the damage was averted, it could be weeks or even months before some real numbers begin to emerge.

Thus, price movements through the media event were purely based on speculation. The market’s job over the next 4-8 weeks will be pricing the revised supply numbers. Even though a worst case scenario did not materialize, there is no doubt that Florida lost some oranges to the cold weather and that the USDA will end up with an estimate of less than 135 million boxes of oranges for 2010. When the second smallest crop in 20 years gets even smaller, that is typically not bearish for prices.

This means that further speculative liquidation over the next few weeks should be an opportunity to enter a fundamentally supported bull market at a fair price. In our case, that would be selling deep out of the money puts well beneath the market. Selling puts gives you the highest odds for success as you can profit even if the market does not rally or continues to fall in the short term. The fundamental set up should keep an invisible floor under prices – at least until Brazilian oranges begin coming to market later this year.

It’s the kind of fundamental set up you seek as an option seller. We’ll be watching closely over the next 2-4 weeks for positioning opportunities.

(See Liberty Trading Group’s James Cordier LIVE on CNBC from January 4th, 2010 discussing FCOJ prices in the wake of freezing temperatures at http://www.libertytradinggroup.com/news.html )

To learn more about selling options in the commodities markets, feel free to visit us on the web at www.OptionSellers.com. A complimentary option selling information pack is available for qualified investors.