![]() (UTHR) was founded in 1996 and is headquartered in Maryland. Focused on the development of pharmaceutical products for the treatment of cardiovascular disease, the company has expanded its therapeutic targets into the viral and cancer arena as well.

(UTHR) was founded in 1996 and is headquartered in Maryland. Focused on the development of pharmaceutical products for the treatment of cardiovascular disease, the company has expanded its therapeutic targets into the viral and cancer arena as well.

UTHR has been profitable since ’04 and the stock has had a nice run since the market crash ’08 rising from $24/share to its current price of $66, but there is still potential for the stock to go much higher (Figure 1). As can been seen in the stock price, the company has a market cap of $3.8B, a forward looking P/E value of 19, and a operating margin of 28%. Revenue growth as been a whopping 52% yoy, so the company has products that are making some in-roads into their flagship product, Remodulin for pulmonary arterial hypertension (PAH). First, the most recent earnings information. In its February earnings call, UTHR’s total revenues for the three months ended December 31, 2010, were $166.5 million, up from $108.9 million for the quarter ended December 31, 2009. Net income for the three months ended December 31, 2010, was $9.5 million or $0.17 per basic share, compared to a net loss of $3.3 million or $0.06 per basic share for the quarter ended December 31, 2009. For the year ended December 31, 2010 (Table 1 below), we had net income of $105.9 million, or $1.89 per basic share and $1.78 per diluted share, compared to $19.5 million, or $0.37 per basic share and $0.35 per diluted share, for the year ended December 31, 2009. The revenues and income are growing rapidly!

Table 1. 2009 vs. 2010 Revenues by Product

| 2009 | 2010 | |

| in $M | ||

| Remodulin | 332 | 404 |

| Tyvaso | 20 | 152 |

| Adcirca | 6 | 36 |

|

Telemedicine products and services |

11 | 11 |

| Licensing | 1.2 | 1.2 |

| Total Revenues | 370 | 604 |

Figure 1. 2 yr stock price of UTHR

What is PAH and how is it treated? PAH is an increase in blood pressure in the pulmonary artery, pulmonary vein, or pulmonary capillaries, together known as the lung vasculature, leading to shortness of breath, dizziness, fainting, and other symptoms, all of which are exacerbated by exertion. Pulmonary hypertension can be a severe disease with a markedly decreased exercise tolerance and heart failure. It was first identified by Dr. Ernst von Romberg in 1891.[1] According to the most recent classification, it can be one of five different types: arterial, venous, hypoxic, thromboembolic or miscellaneous. Treatment is determined by whether the PH is arterial, venous, hypoxic, thromboembolic, or miscellaneous. Since pulmonary venous hypertension is synonymous with congestive heart failure, the treatment is to optimize left ventricular function by the use of diuretics, beta blockers, ACE inhibitors, etc., or to repair/replace the mitral valve or aortic valve. UTHR has a Prostacyclin (prostaglandin I2) analogue, Remodulin, which is considered the most effective treatment for PAH.

Figure 2. PAH

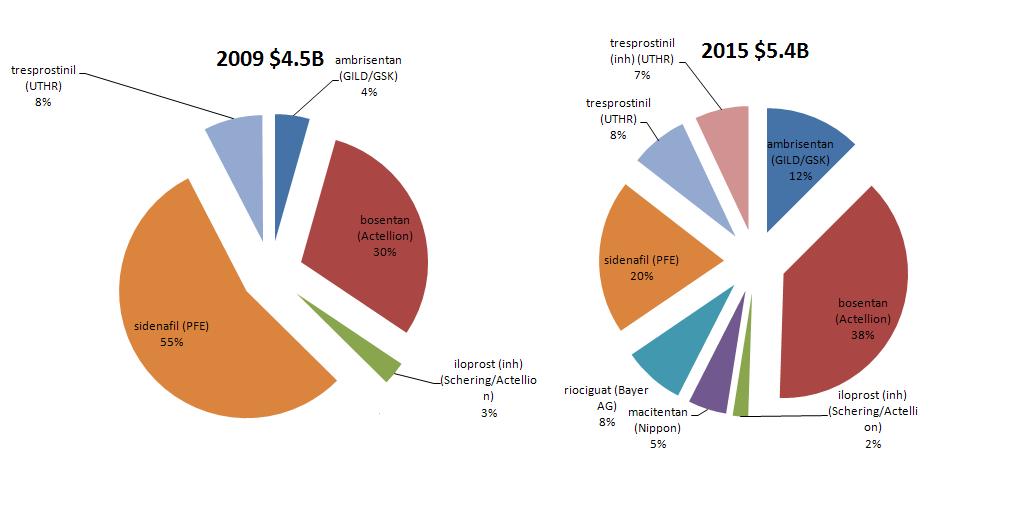

Remodulin & Tyvaso (tresprostinil) – was originally developed by GSK and Pharmacia, tresprostinil is a stable structural analog of prostacyclin in liquid formulation for injection. Tresprostinil is used either as a continuous subcutaneous or IV infusion for the treatment of pulmonary arterial hypertension (PAH) in patients with NYHA Class II-IV symptoms to diminish symptoms associated with exercise. Below is the total market for PAH and UTHR is poised to take a bigger share of that market IF their drugs remain compelling enough for doctors to prescribe and/or there are no adverse events. PFE is the clear market leader (thus far), with GILD moving into a nice second, but the market itself is ripe for consolidation. (Tyvaso is the inhaled version of Remodulin).

Figure 3. PAH market.

Adcirca (tadalafil) – think Celais….the PDE-5 inhibitor for erectile dysfunction (same as Viagra (sidenafil) in Figure 3). UTHR launched it in the EU, Japan and the US in 2009, but sales are slow to pick up due to PFE’s sidenafil (Viagra) dominating the market.

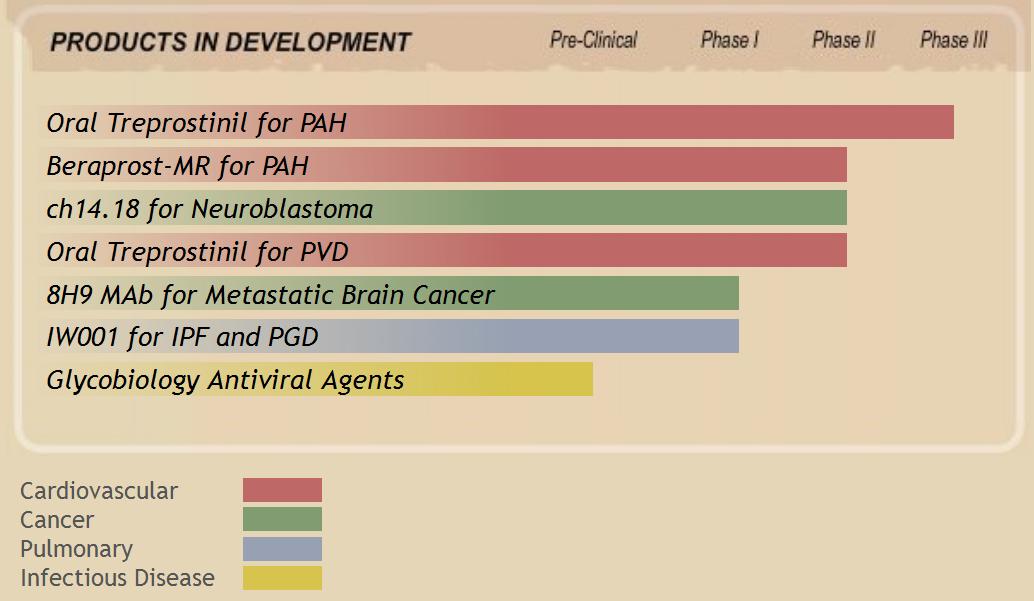

Pipeline

As the Figure above notes, Treprostinil remains a mainstay to the companies pipeline. The oral version is in Phase 3 trials for for the potential treatment of peripheral vascular disease (PVD), scleroderma and pulmonary arterial hypertension (PAH). Unless disaster hits, I would expect that the drug works for PVD and PAH, but the scleroderma trial is an interesting one. Actellion tried bosentan in scleroderma and it worked in subjects with digital ulcers, but it remains unclear (from what I can find) that bosentan was ever approved for scleroderma. The rationale for treprostinil working in scleroderma are strong, and data are due out in the next few months.

Beraprost-MR (under license from is another oral analogue of prostacyclin PGI2 for PAH. It is still in Phase 2. Based upon the structure and mechanism of action, it should work, but how well compared to what is already on the market?

IW001 (ImmuneWorks and LungRx (wholly owned subsidiary of UTHR)) were in clinical trials (Phase 1 – so very early) with IW001 for idiopathic pulmonary fibrosis (IPF) and transplant rejection. IW001 is an oral solution of Type V Collagen and to under stand how this is supposed to work is very interesting. First, IPF) may begin as the result of an injury to the lung, possibly due to an infection, smoking, or other unknown event. This injury induces an inflammatory response, attracting antigen-presenting cells to the lung and exposes Type V Collagen to these antigen-presenting cells, which phagocytose this protein. These antigen-presenting cells then migrate to a lymph node, where they present this auto-antigen to T cells. T cells activated against Type V Collagen, along with B cells, migrate back to the lung and the initial site of inflammation. These activated immune cells exacerbate the lung injury through a self-destructive autoimmune response against Type V Collagen. This leads to further fibrosis in the lung, and eventually lung failure and death. Knowing this, ImmuneWorks along with UTHR are trying to develop potential immune tolerance therapies for people with IPF and those awaiting a lung transplant. in other words, they are trying to trick the immune system to ‘calm down’ with the reactions to ‘self’ proteins, thus slowing down the immune response. It is novel, but there are many types of collagen, so not sure one type is the answer.

In the cancer area, UTHR is developing ch14.18 and 8H9 mAb. Ch14.18 is an anti-GD2 monoclonal antibody 3F8, for the potential diagnosis (as 131I-3F8) and treatment of cancers, including neuroblastomas. One has already been developed by a Lexigen Pharmaceuticals (no data have been reported since 1998!), but recently, a paper in the New England Journal of Medicine showed that another ch14.18 treatment along with two other treatments showed remarkable results in that the new treatment cuts down a high-risk cancer’s recurrence rate over a 2-year period by 20 percent – and that is a major leap forward – even if the cancer is not among the most common types. I think this will be rocketed through the FDA, so watch closely, although the total number of patients is small (less than 650/yr diagnosed). It remains to be seen how well it performs in broader range trials.

8H9 is a mouse monoclonal antibody licensed from Memorial Sloan-Kettering Cancer Center for solid brain tumors. It reacts with several epitopes in brain tumors, and It is way too early to even jump on this one and dissect it.

UTHR is reliant on its PAH pipeline for the near future, and as the population ages, and PAH becomes more prevalent, revenue could benefit. I see the company as a take over target with a $3.8B market cap, and mid-tier pharma on the prowl for more market share. I like a very conservative spread, as the stock is volatile. The January 2012 $60/65 BCS for $2.50 or better coupled with the sale of the $45 Ps for $3 or better. That is a 50c credit for the $5 spread, and I would be happy to own them at $44.50 for a long term hold.