EUR/USD

The dollar gained initial support on Tuesday from a deterioration in risk appetite as fears over the Libyan situation and the Middle East continued. The Euro was subjected to further selling pressure during European trading, dipping to lows close to 1.3525, but there was then a sharp recovery.

Comments from ECB officials were again watched very closely with Mersch commenting that there would need to be a rebalancing of monetary stance at some point. There were suggestions that there could be a consensus for a tougher language at the early-March monetary council meeting. The comments inevitably fuelled speculation that the central bank would move to tighten policy earlier than expected.

The comments boosted the Euro strongly during the US session with a high near 1.37. There will still be concerns that any tightening will have a negative impact on the peripheral economies which would reinforce the structural weaknesses. Tensions will remain high ahead of the planned March 24-25 EU Summit, especially if peripheral credit-default spreads continue to widen.

The US consumer confidence data recorded an increase to a three-year high of 70.4 for February from a revised 64.8 the previous month which will maintain optimism over near-term consumer spending trends. In contrast, the Case-Shiller house-price index recorded a 2.4% decline in the year to December which will maintain doubts over the housing sector.

Regional Fed President Evans maintained a dovish tone in comments on Tuesday and there will still be expectations that the Fed will be very slow to adjust policy with the dollar near 1.37 in Asia on Wednesday.

Source: VantagePoint Intermarket Analysis Software

Call now and you will be provided with FREE recent forecasts

that are up to 86% accurate * 800-732-5407

If you would rather have the recent forecasts sent to you, please go here

Yen

The dollar was unable to regain the 83.50 level in Europe on Tuesday and after initially finding support close to 82.80, there were renewed losses to lows near 82.55 during Asian trading on Wednesday.

Risk conditions remained important and the Japanese currency continued to gain support from downward pressure on equity markets and a reluctance to fund carry trades.

The domestic data recorded a 1.1% decline in services-sector prices in the year to January compared with 1.3% decline previously and there will be some speculation that rising energy prices will lessen deflationary pressures. There will still be speculation that the Finance Ministry will look to cap any significant yen gains.

Sterling

Sterling was blocked above 1.6180 against the dollar in Europe on Tuesday and dipped to lows near 1.61 before recovering losses on a wider US retreat. The UK currency was unsettled in part by a general deterioration in international risk appetite.

The latest government borrowing data was stronger than expected with a surplus of GBP3.7bn for January compared with a revised GBP14.5bn deficit the previous month. January is a strong month seasonally for tax receipts, but there will be some relief that there was an annual improvement.

The MPC minutes will be watched very closely on Wednesday amid expectations of greater divisions within the committee and the possibility that more than 2 members voted for a rate increase. In comments on Tuesday, Tucker commented that the Bank of England faced very difficult choices over the next few months while Posen maintained his opposition to any tightening. Substantial divisions will remain and Sterling volatility is likely to remain a key feature as markets debate the outlook for interest rates and the economy.

Swiss franc

The franc maintained a strong tone during Tuesday as it tested Euro support below 1.28 and also advanced to February highs near 0.9360 against the US dollar. Safe-haven demand remained an important factor with the currency gaining fresh support from a deterioration in risk appetite. Global risk conditions will remain a key determinant of the franc’s value.

The latest trade data recorded a monthly surplus of close to GBP2.0bn and there was real-terms annual increase in exports. There is evidence of pressure in some sectors, but the data overall lessened immediate fears over the competitive position.

Source: VantagePoint Intermarket Analysis Software

Call now and you will be provided with FREE recent forecasts

that are up to 86% accurate * 800-732-5407

If you would rather have the recent forecasts sent to you, please go here

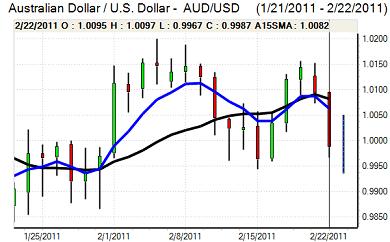

Australian dollar

The Australian dollar remained under pressure during European trading on Tuesday, weakening to a low near 0.9960 against the US dollar before rallying and regaining parity on a wider US retreat. The Australian currency was still tending to under-perform on the crosses as risk conditions remain less favourable.

There will be further selling pressure on the currency if there is any further escalation in Middle East tensions, especially as high oil prices will also increase unease over regional and global growth prospects. The domestic economic trends will also be watched closely amid expectations of a significant slowdown in consumer spending which will sap currency support.